Crowdcube • Lireka

Financement participatif (equity crowdfunding)

Lireka

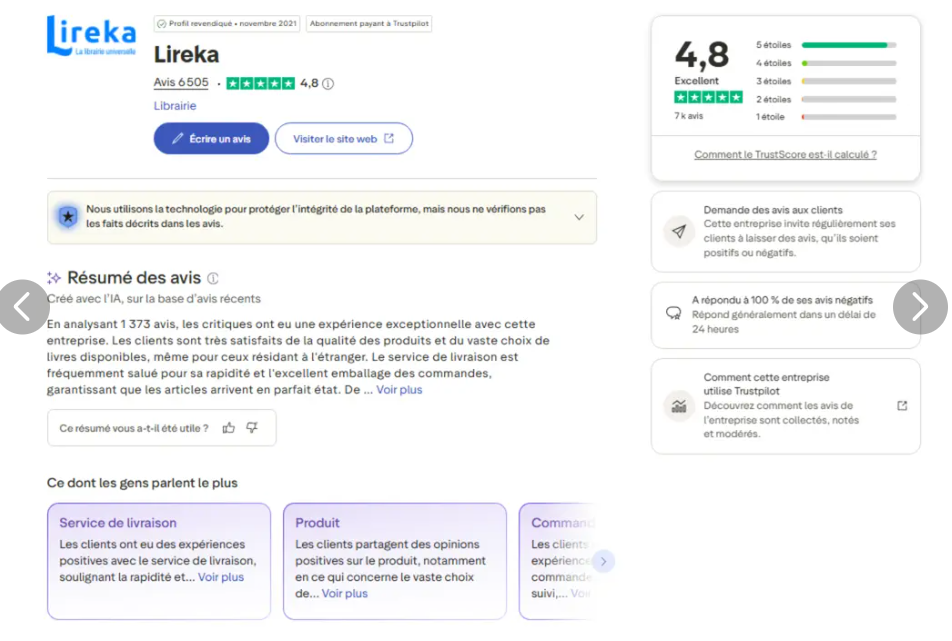

Première librairie en ligne à proposer la livraison internationale GRATUITE, Lireka rend la culture accessible en expédiant des livres dans le monde entier. Fondée par deux anciens employés d'Amazon, elle propose un vaste catalogue de près de 2 millions de titres à des prix attractifs.

Key project data

Target amount

3,0 MEUR

Valuations

9,0 MEUR

Date de fin

2026-07-11

Would AI invest?

64/100

1

100

Aperçu généré par l'IA

AI project overview

Condensed summary based on project data

<h1><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><em>La première librairie internationale proposant la livraison gratuite dans le monde entier — nous exportons des livres en français et en anglais à destination des expatriés et des francophones du monde entier.</em></span></span></h1> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Secteur</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Librairie en ligne internationale (e-commerce / exportation de livres), associée à la librairie physique Librairie Arthaud</span></span></p> </td> </tr> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Stade</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Qualifiée par l’entreprise de « série A »</span></span></p> </td> </tr> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Siège</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Grenoble, France (Lireka SAS ; détient 100 % de Librairie Arthaud SAS)</span></span></p> </td> </tr> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Levée de fonds</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Levée de fonds en capital de 3 millions d’euros au total (2,4 millions d’euros de capitaux nouveaux) pour une valorisation pré-levée de 9 millions d’euros ; 2,55 € par action ; participation via un mandataire Crowdcube</span></span></p> </td> </tr> </tbody> </table> <h2><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Score IA</span></span></h2> <table cellspacing="0" class="Table" style="background:white; border-collapse:collapse; margin-left:-1px; width:6.5in"> <tbody> <tr> <td style="background-color:#faece7; vertical-align:top; width:229px"> <p style="text-align:center"> </p> </td> <td style="background-color:#faece7; vertical-align:top; width:395px"> <p><span style="font-size:11px"><span style="font-family:Aptos,sans-serif"><strong><span style="color:black">Pourquoi ce score</span></strong></span></span></p> </td> </tr> <tr> <td style="background-color:#faece7; vertical-align:top; width:229px"> <p style="text-align:center"> </p> </td> <td style="background-color:#faece7; vertical-align:top; width:395px"> <ul> <li><span style="font-size:11px"><span style="font-family:Aptos,sans-serif"><span style="color:black">Une traction réelle et corroborée par plusieurs sources : environ 14,4 millions d’euros de chiffre d’affaires du groupe en 2025, chiffre d’affaires du site web de Lireka en hausse d’environ +41 % à 5,5 millions d’euros, 104 643 clients cumulés, note Trustpilot de 4,8/5 (6 283 avis), et coût d’acquisition client (CAC) déclaré de 8 € avec un retour sur investissement publicitaire (ROAS) > 5.</span></span></span></li> </ul> </td> </tr> <tr> <td style="background-color:#faece7; vertical-align:top; width:229px"> <p style="text-align:center"><span style="font-size:12pt"><span style="font-family:Aptos,sans-serif"><strong><span style="font-size:28.0pt"><span style="color:black">53 / 100</span></span></strong></span></span></p> </td> <td style="background-color:#faece7; vertical-align:top; width:395px"> <ul> <li><span style="font-size:11px"><span style="font-family:Aptos,sans-serif"><span style="color:black">Des fondateurs expérimentés — Marc Bordier (11 ans chez Amazon en tant que responsable de la catégorie Livres) et Emma Henry (Hachette, Amazon, Samsung) — dans un domaine qu’ils connaissent bien.</span></span></span></li> </ul> </td> </tr> <tr> <td style="background-color:#faece7; vertical-align:top; width:229px"> <p style="text-align:center"><span style="font-size:12pt"><span style="font-family:Aptos,sans-serif"><strong><span style="color:black">Verdict : prudence</span></strong></span></span></p> </td> <td style="background-color:#faece7; vertical-align:top; width:395px"> <ul> <li><span style="font-size:11px"><span style="font-family:Aptos,sans-serif"><span style="color:black">Mais la société d’exploitation est toujours déficitaire au niveau comptable (résultat net de Lireka SAS : −0,40 million d’euros en 2025), elle est endettée de plusieurs millions d’euros, et le dossier d’investissement repose presque entièrement sur les prévisions de la direction, que la plateforme elle-même qualifie de non garanties.</span></span></span></li> </ul> </td> </tr> <tr> <td style="background-color:#faece7; vertical-align:top; width:229px"> <p style="text-align:center"> </p> </td> <td style="background-color:#faece7; vertical-align:top; width:395px"> <ul> <li><span style="font-size:11px"><span style="font-family:Aptos,sans-serif"><span style="color:black">Plusieurs lacunes d’information non résolues : un troisième cofondateur, dont le nom a été rendu public, est absent des documents, les chiffres relatifs à l’actionnariat ne concordent pas parfaitement, l’éligibilité aux allègements fiscaux est mentionnée de manière incohérente, et une procédure devant les Prud’hommes est en cours depuis janvier 2025.</span></span></span></li> </ul> </td> </tr> </tbody> </table> <p> </p> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#e6f1fb; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:672px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">ℹ️ Ceci ne constitue pas un conseil en investissement.</span></strong><span style="color:black"> </span><span style="color:#000000">L’objectif de cette synthèse est d’aider les investisseurs potentiels à présélectionner rapidement des projets de financement participatif sans pour autant prendre une décision d’investissement définitive. Avant d’investir, le projet finalement retenu doit être examiné en détail sur la base des informations fournies par l’entreprise sur la plateforme de financement participatif concernée. L’IA peut commettre des erreurs ; vous devez donc vérifier les données.</span></span></span></p> </td> </tr> </tbody> </table> <h2><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Description de l’entreprise</span></span></h2> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Lireka est une librairie en ligne spécialisée dans l’exportation de livres. Elle propose la livraison gratuite dans le monde entier, des prix affichés en monnaie locale et la prise en charge des frais de douane et des droits d’importation pour le client, se positionnant ainsi face aux prix d’exportation plus élevés d’Amazon et à ses droits d’importation facturés séparément. L’entreprise dispose d’un catalogue de près de 2 millions de titres, principalement en français, avec un catalogue en anglais lancé au deuxième trimestre 2026 et des versions en allemand, espagnol et italien prévues d’ici 2027.</span></span></p> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">L’entreprise est associée à la Librairie Arthaud, une librairie grenobloise fondée en 1801 et rachetée par le groupe en octobre 2020, qui apporte un stock physique (environ 80 000 références), des relations avec les éditeurs et une image de marque de librairie indépendante. Lireka gère également une branche B2B (Lireka Pro) qui vend aux Alliances françaises, aux Instituts français, aux écoles françaises et aux bibliothèques ; l’entreprise indique que le B2B représente aujourd’hui environ 10 % de son chiffre d’affaires, la direction visant une part de 20 à 30 %.</span></span></p> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Les fondateurs sont Marc Bordier (président-directeur général, qui a passé environ 11 ans chez Amazon en tant que responsable de la catégorie Livres) et Emma Henry (directrice générale, forte d’une expérience chez Hachette, Amazon et Samsung). Des sources publiques mentionnent également un troisième cofondateur, Robin Mallein (directeur technique, basé à Prague), qui n’apparaît pas dans la présentation actuelle ni dans le résumé des informations clés.</span></span></p> <h2><span style="font-family:Times New Roman,serif"><span style="font-size:13.3333px">Rendements potentiels</span></span></h2> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Objectif de l’entreprise</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Consolider une position déjà éprouvée en tant que spécialiste de l’exportation de livres ; vision à long terme : atteindre un chiffre d’affaires supérieur à 100 millions d’euros sur 8 à 10 ans et devenir le leader européen de l’exportation de livres (selon les déclarations de l’entreprise, d’après le dossier de présentation).</span></span></p> </td> </tr> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Base de valorisation</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong>Fournis par l’entreprise</strong> — Lireka a défini ses propres objectifs de rendement, son horizon de sortie (5 à 7 ans) et ses multiples de sortie (EV/Chiffre d’affaires 0,85x, EV/EBITDA 10x) ; la note informative de la plateforme mentionnant un risque d’environ 10x ne s’applique donc pas ici.</span></span></p> </td> </tr> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Sortie envisagée</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Cession à un acquéreur stratégique (distributeurs de livres, e-commerce spécialisé, médias européens) ou opération de croissance par capital-investissement ; valeur d’entreprise cible à la sortie d’environ 30 millions d’euros sur un chiffre d’affaires prévisionnel pour 2030 d’environ 35 millions d’euros et un EBITDA d’environ 3 millions d’euros.</span></span></p> </td> </tr> </tbody> </table> <h2><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Parcours vers l’objectif (méthodologie de l’entreprise)</span></span></h2> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">La société propose son propre cadre de sortie plutôt que de s’appuyer sur une approche heuristique sectorielle. Elle évalue une sortie future à environ 30 millions d’euros de valeur d’entreprise en appliquant un multiple EV/chiffre d’affaires de 0,85x au chiffre d’affaires prévisionnel de 2030 d’environ 35 millions d’euros, ce chiffre étant recoupé avec un multiple EV/EBITDA de 10x sur l’EBITDA prévisionnel de 2030 d’environ 3 millions d’euros. Atteindre ce chiffre d’affaires suppose que l’entreprise maintienne une croissance annuelle de son site web d’environ +41 % de 2026 à 2030, tout en déployant des catalogues en anglais, allemand, espagnol et italien en plus du modèle français qui a fait ses preuves. Par rapport à une valeur d’entrée pré-financement de 9 millions d’euros, une valeur d’entreprise de sortie d’environ 30 millions d’euros implique un multiple d’environ 3,3x au niveau de l’entreprise avant prise en compte de toute dilution, des frais ou de la cascade de liquidation — ce qui correspond globalement au seuil de « 3x » indiqué dans la présentation elle-même.</span></span></p> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Exemple de sortie comparable cité</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Le dossier illustre cette thèse en s’appuyant sur l’acquisition par Livingbridge, en 2021, de la plateforme de recommerce World of Books (une entreprise de commerce électronique spécialisée dans le livre, soutenue par un fonds de capital-investissement).</span></span></p> </td> </tr> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Étapes clés menant à la sortie</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Développement du catalogue anglais (objectif : 10 millions de titres), lancement en Allemagne, mise en place d’une logistique d’approvisionnement direct vers de nouvelles destinations, doublement de la superficie de l’entrepôt pour atteindre environ 2 000 m², et EBITDA atteignant environ 3 millions d’euros d’ici 2030 (toutes ces prévisions sont celles de l’entreprise).</span></span></p> </td> </tr> </tbody> </table> <h2><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Valorisation</span></span></h2> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Demande</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">3 millions d’euros de fonds propres totaux, dont 2,4 millions d’euros de capitaux nouveaux ; la présentation précise qu’environ 300 000 euros sont réservés à la tranche grand public de Crowdcube.</span></span></p> </td> </tr> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Valeur pré-financement</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">9 000 000 € (présentation) / 8 998 514 € (cotation). Cours de l’action : 2,55 € (≈ 2,20 £).</span></span></p> </td> </tr> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Valeur post-financement implicite</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Environ 11,4 millions d’euros sur la base des 2,4 millions d’euros de capitaux nouveaux (environ 12 millions d’euros si la totalité des 3 millions d’euros est considérée comme des capitaux propres valorisés). Le chiffre exact dépend du montant final levé, qui n’a pas encore été divulgué.</span></span></p> </td> </tr> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Méthodologie</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Non divulguée. La société présente un cadre de multiples de sortie pour la future cession, mais n’explique pas comment le prix d’entrée de 9 millions d’euros a lui-même été calculé.</span></span></p> </td> </tr> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Référence</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">La valorisation pré-financement de 9 millions d’euros est inférieure à 1 fois le chiffre d’affaires consolidé de 2025 (environ 14,4 millions d’euros) et correspond à environ 1 fois le chiffre d’affaires autonome de Lireka SAS pour 2025 (environ 9,0 millions d’euros). L’hypothèse de sortie de la société repose sur un faible multiple EV/chiffre d’affaires de 0,85x, ce qui reflète le fait que le secteur de la vente au détail de livres se négocie généralement à des multiples de chiffre d’affaires modestes.</span></span></p> </td> </tr> </tbody> </table> <h2><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Instrument et conditions pour les investisseurs</span></span></h2> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Ce que vous détenez</span></span></h3> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Vous recevrez des actions ordinaires — la seule catégorie d’actions de cette société (il n’existe pas d’actions « privilégiées » distinctes). Vous ne les détiendrez pas directement : la propriété légale revient à Crowdcube Nominees Limited, qui détient les actions en fiducie pour votre compte (c’est ce qu’on appelle une structure de prête-nom). Vous êtes le « bénéficiaire effectif », ce qui signifie que vous percevez la valeur économique, mais que le mandataire détient le titre légal et exerce généralement les droits de vote des actions mises en commun par les investisseurs en un seul bloc. Chaque action ordinaire donne droit à une voix, mais comme les actions des investisseurs sont regroupées par l’intermédiaire du mandataire et que les fondateurs contrôlent une large majorité — Marc Bordier détient à lui seul environ 58 % (les fondateurs totalisent environ 69 % selon des sources publiques) —, les investisseurs individuels ont très peu d’influence concrète sur les décisions de la société, y compris sur toute décision de vendre la société.</span></span></p> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Dilution et futurs tours de financement</span></span></h3> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">La « dilution » signifie que votre pourcentage de participation diminue lorsque la société émet de nouvelles actions lors d’une levée de fonds ultérieure. La société a déclaré qu’elle prévoyait de lever davantage de capitaux (ses facteurs de risque indiquent qu’elle en aura besoin, sans garantie de succès), et elle a déjà obtenu 0,6 million d’euros de billets convertibles auprès d’actionnaires existants en 2025. Les investisseurs du financement participatif se voient ici accorder des droits de préemption (le droit d’acheter suffisamment d’actions lors d’un tour de table futur pour conserver votre pourcentage), mais la plupart des petits investisseurs ne participent pas aux tours suivants ; une certaine dilution au fil du temps est donc le scénario réaliste par défaut. Il n’existe aucune protection anti-dilution liée au prix : si le prix d’un tour de table futur est inférieur à celui-ci, votre participation n’est pas protégée.</span></span></p> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Exemple concret (mécanisme standard du tableau de capitalisation, sans constituer un conseil) : si vous investissez aujourd’hui 1 000 € à une valorisation post-financement d’environ 11,4 millions d’euros, vous détenez environ 0,0088 % de la société (environ 1 000 € ÷ 11,4 millions d’euros). Si la société lève ensuite 4 millions d’euros à une valorisation pré-financement de 20 millions d’euros (une série A réussie, à un prix plus élevé), les nouveaux fonds représentent environ 17 % de la société après augmentation de capital, votre participation est donc diluée à environ 0,0073 %. Si, en revanche, le tour suivant est un « down-round » à 6 millions d’euros de valorisation pré-financement levant 4 millions d’euros, les nouveaux capitaux représentent environ 40 % de la société après dilution, votre participation est diluée à environ 0,0053 %, et la valeur implicite de vos 1 000 € baisse d’environ 30 à 40 % en raison de la baisse du cours de l’action.</span></span></p> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Concernant les options de souscription d’actions réservées aux salariés : la société dispose d’un pool d’options BSPCE (l’équivalent français des options de souscription d’actions réservées aux salariés), et la partie non attribuée est déjà prise en compte dans le nombre d’actions en situation de dilution totale de 3 528 829 utilisé pour fixer le prix de ce tour de table ; cette dilution spécifique est donc déjà prise en compte. Par ailleurs, les obligations convertibles à échéance 2025 devraient se convertir en actions avec une décote de 20 %, car ce tour de table semble dépasser le seuil de 6,6 millions d’euros « pré-money » qui déclenche la conversion — ce qui entraînera l’émission d’actions à peu près au moment de votre investissement. Votre droit de préemption est le principal outil dont vous disposez pour préserver votre pourcentage lors des tours de financement futurs, si vous choisissez d’investir davantage.</span></span></p> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Mécanismes de sortie et de liquidation</span></span></h3> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">La « préférence de liquidation » définit l’ordre dans lequel les parties sont remboursées en cas de vente ou de liquidation de la société. Même s’il n’existe ici qu’une seule catégorie d’actions, le pacte d’actionnaires établit un ordre de priorité de remboursement : tout d’abord, chaque actionnaire récupère le montant qu’il a initialement payé pour ses actions ; ensuite, tout argent restant revient en priorité aux « nouveaux investisseurs » (ce qui inclut les personnes qui investissent lors de ce tour) jusqu’à ce qu’ils récupèrent la prime d’émission qu’ils ont versée ; et s’il n’y a pas assez pour couvrir cela, le montant restant est réparti proportionnellement entre les nouveaux investisseurs. Tout ce qui reste après cela est réparti entre tous les actionnaires en fonction de leur pourcentage de participation. En termes simples, cela confère aux investisseurs de ce tour de table une préférence de remboursement du capital d’environ 1x — une certaine protection contre la baisse, mais pas de multiple.</span></span></p> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">La clause de « drag-along » permet à la majorité de contraindre tous les autres actionnaires à vendre aux mêmes conditions. Dans ce cas, les détenteurs d’au moins 50 % de l’ensemble des actions et d’au moins 50 % des actions détenues par les investisseurs peuvent contraindre tous les autres actionnaires à vendre à un acquéreur prenant 100 % des parts — mais uniquement si le prix atteint un seuil minimum égal au prix d’entrée des nouveaux investisseurs majoré d’un taux composé de 10 % par an. Le « tag-along » est le droit symétrique qui vous protège : si un actionnaire majoritaire vend suffisamment d’actions pour conférer à un acquéreur un contrôle supérieur à 50 %, vous pouvez vous joindre à la vente aux mêmes conditions ; un « tag-along » proportionnel s’applique également aux ventes de moindre importance. Vous pouvez donc être entraîné dans une vente que vous n’avez pas choisie, mais pas en dessous d’un seuil de prix minimal en hausse, et vous pouvez exercer votre droit de « tag-along » lorsque d’autres vendent.</span></span></p> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Liquidité : aucun dividende n’est prévu, il n’existe pas de marché secondaire dédié (vous ne pouvez céder votre droit de jouissance qu’à un autre membre de Crowdcube, le titre de propriété restant entre les mains du prête-nom), et des restrictions de cession s’appliquent. Vous devez considérer cet investissement comme illiquide à long terme — de manière réaliste, 5 à 7 ans jusqu’à une sortie au niveau de l’entreprise, selon le dossier de présentation — et une perte en capital est possible.</span></span></p> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Risques clés spécifiques à cet instrument</span></span></h3> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Les actions sont détenues par l’intermédiaire d’un mandataire et les fondateurs détiennent une large majorité ; les investisseurs participatifs n’ont donc pratiquement aucune influence sur le plan du vote — y compris sur la décision de vendre l’entreprise et le moment de cette vente.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Aucune protection anti-dilution basée sur le prix : en cas de tour de table à la baisse, le pourcentage détenu par les investisseurs participatifs et la valeur implicite de l’investissement chutent sans aucune protection.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">La cascade de liquidation rembourse d’abord la souscription initiale de chaque actionnaire, puis la prime des nouveaux investisseurs — en cas de vente à faible valeur, après le remboursement des créanciers (le groupe est endetté de plusieurs millions d’euros), il pourrait ne rester que peu de fonds à distribuer au prorata.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Le droit de « drag-along » (droit de vente forcée) au seuil de 50 %/50 % signifie que les fondateurs et les investisseurs alignés peuvent imposer une vente sans le consentement des investisseurs participatifs (mais uniquement au-dessus d’un seuil correspondant au prix d’entrée majoré de 10 % par an).</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Les obligations convertibles à échéance 2025 détenues par les actionnaires existants seront probablement converties avec une décote de 20 % autour de ce tour de table, et la société prévoit de lever à nouveau des fonds — ces deux opérations entraînant l’émission d’actions avant ou parallèlement à la levée de fonds auprès du grand public.</span></span></li> </ul> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Éléments non divulgués</span></span></h3> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Les éléments suivants n’ont pas été divulgués dans les documents examinés. Lorsqu’une condition n’est pas divulguée, vous ne pouvez pas l’évaluer avant d’investir :</span></span></p> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Le tableau de capitalisation complet avant le tour de table — seule la participation de Marc Bordier (> 25 %) est détaillée ; les investisseurs providentiels antérieurs, le pourcentage exact du pool d’options et le flottant ne sont pas ventilés.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Une date de fin fixe pour le blocage des titres des investisseurs / une période de détention fixe (des restrictions de cession existent, mais aucune date de fin explicite n’est indiquée).</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">La méthodologie utilisée pour établir la valorisation initiale de 9 millions d’euros.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Le montant final levé, et donc la valorisation post-money exacte et la dilution finale (la levée de fonds est en cours).</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">L’intégralité des statuts (mentionnés comme étant joints à l’e-mail de réflexion, mais non fournis), ainsi que le montant chiffré du litige en cours en matière d’emploi.</span></span></li> </ul> <h2><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Répartition des notes</span></span></h2> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:213px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Catégorie</span></strong></span></span></p> </td> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Note</span></strong></span></span></p> </td> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Pondération</span></strong></span></span></p> </td> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:312px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Verdict</span></strong></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:213px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Historique de l'équipe et du fondateur</span></span></p> </td> <td style="background-color:#faeeda; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><span style="color:black">78</span></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">15 %</span></span></p> </td> <td style="background-color:#faeeda; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:312px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Modéré à solide</span></strong><span style="color:black"> — Expérience approfondie d’Amazon et de l’édition dans ce domaine précis ; contrebalancée par un troisième cofondateur dont l’identité n’est pas divulguée et par le manque d’informations publiques sur le reste de l’équipe.</span></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:213px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Traction et rentabilité unitaire</span></span></p> </td> <td style="background-color:#faeeda; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><span style="color:black">72</span></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">30</span></span></p> </td> <td style="background-color:#faeeda; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:312px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Modérée</span></strong><span style="color:black"> — Chiffre d’affaires réel, croissance du site web d’environ +41 %, plus de 100 000 clients et un ROAS > 5 ; mais la rentabilité se limite à un EBITDA faible et le dossier repose sur des prévisions.</span></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:213px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Taille et croissance du marché</span></span></p> </td> <td style="background-color:#faeeda; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><span style="color:black">60</span></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">15</span></span></p> </td> <td style="background-color:#faeeda; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:312px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Modérée</span></strong><span style="color:black"> — Vaste marché d’exportation déclaré par langue, mais les chiffres sont fournis par l’entreprise et n’ont pas été vérifiés de manière indépendante dans le dossier.</span></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:213px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Concurrence et avantage concurrentiel</span></span></p> </td> <td style="background-color:#faece7; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><span style="color:black">55</span></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">10</span></span></p> </td> <td style="background-color:#faece7; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:312px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Prudence</span></strong><span style="color:black"> — La logistique négociée, la tarification géolocalisée et le référencement naturel (SEO) constituent des avantages plausibles, mais Amazon est le concurrent direct et la plateforme principale a été développée par une agence externe.</span></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:213px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Modèle économique et évolutivité</span></span></p> </td> <td style="background-color:#faeeda; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><span style="color:black">65</span></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">10</span></span></p> </td> <td style="background-color:#faeeda; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:312px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Modéré</span></strong><span style="color:black"> — Une stratégie multilingue véritablement reproductible reposant sur une base commune ; non éprouvée au-delà du français, l’anglais n’étant lancé qu’en 2026.</span></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:213px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Santé financière et bilan</span></span></p> </td> <td style="background-color:#faece7; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><span style="color:black">48</span></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">20</span></span></p> </td> <td style="background-color:#faece7; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:312px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Prudence</span></strong><span style="color:black"> — Lireka SAS a enregistré des pertes nettes chaque année jusqu’en 2025 (−0,40 million d’euros), est endettée à hauteur de plusieurs millions d’euros et doit impérativement lever des capitaux supplémentaires.</span></span></span></p> </td> </tr> </tbody> </table> <h2><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Analyse détaillée</span></span></h2> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Équipe et parcours du fondateur (78 / 100)</span></span></h3> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Points forts</span></strong></span></span></p> </td> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Faiblesses</span></strong></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Marc Bordier a passé environ 11 ans chez Amazon en tant que responsable de la catégorie Livres à Paris et à Londres — une expérience directement pertinente en matière de catégorie et d’opérations.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Emma Henry apporte son expérience acquise chez Hachette (édition), Amazon et Samsung, ainsi que dans une start-up américaine (Matelab).</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">L’équipe a mené l’entreprise à un chiffre d’affaires d’environ 14 millions d’euros et à un EBITDA consolidé positif, ce qui témoigne de sa capacité d’exécution.</span></span></li> </ul> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Un troisième cofondateur cité dans des sources publiques (Robin Mallein, directeur technique) est absent de la présentation et du SKI, sans aucune explication — ce qui soulève une question quant à la composition de l’équipe.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Les chiffres relatifs à la répartition du capital ne concordent pas selon les sources (SKI : 57,93 % pour Bordier ; présentation : 61 % + 8 % ; site web : 69 % au total).</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Validation indépendante limitée de la profondeur de l’équipe élargie de 14 personnes, au-delà des deux fondateurs cités.</span></span></li> </ul> </td> </tr> </tbody> </table> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Traction et rentabilité unitaire (72 / 100)</span></span></h3> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Points forts</span></strong></span></span></p> </td> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Faiblesses</span></strong></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Le chiffre d’affaires consolidé a atteint environ 14,4 millions d’euros en 2025 ; celui du site web de Lireka a progressé d’environ 41 % pour s’établir à 5,5 millions d’euros.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">104 643 clients cumulés (taux de croissance annuel composé de +124 % entre 2021 et 2025 selon les chiffres de l’entreprise) ; note Trustpilot de 4,8/5 sur 6 283 avis.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Les indicateurs d’acquisition communiqués par l’entreprise (8 € de CAC avec un ROAS > 5) suggèrent un marketing payant efficace, si ces chiffres sont exacts.</span></span></li> </ul> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">La rentabilité se limite à un EBITDA modeste (+11 000 € pour Lireka seule selon la présentation ; environ 44 000 € pour le groupe selon le communiqué de presse), et non à un bénéfice net.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Les indicateurs relatifs à la clientèle et au NPS (NPS de 82) sont fournis par l’entreprise et n’ont pas fait l’objet d’un audit indépendant dans le dossier.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Le scénario optimiste repose sur le maintien d’une croissance de +41 %, tandis que l’EBITDA devrait redevenir négatif en 2027.</span></span></li> </ul> </td> </tr> </tbody> </table> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Taille et croissance du marché (60 / 100)</span></span></h3> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Points forts</span></strong></span></span></p> </td> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Faiblesses</span></strong></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">L’entreprise cite des marchés d’exportation importants par langue (anglais : 5,4 milliards d’euros ; français et allemand : 0,7 milliard d’euros chacun), ce qui vient étayer son hypothèse d’expansion multilingue.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Une définition claire et large de la population cible : environ 300 millions de francophones et environ 2 à 2,5 millions d’expatriés.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Plusieurs sources de données externes sont citées comme base de l’estimation de la taille du marché.</span></span></li> </ul> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Les chiffres relatifs à la taille du marché sont fournis par l’entreprise et n’ont pas fait l’objet d’une vérification indépendante dans le dossier.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Le segment des exportations vers la France, dont l’entreprise a effectivement démontré l’existence, est le plus petit des marchés cités (environ 0,7 milliard d’euros).</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Validation indépendante limitée des taux de croissance dans les niches d’exportation ciblées.</span></span></li> </ul> </td> </tr> </tbody> </table> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Concurrence et avantage concurrentiel (55 / 100)</span></span></h3> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Points forts</span></strong></span></span></p> </td> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Faiblesses</span></strong></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Positionnement différencié en tant que spécialiste de l’export (livraison gratuite, droits de douane inclus, tarification adaptée au marché local) par rapport aux prix à l’export plus élevés d’Amazon et à ses droits de douane facturés séparément.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Avantages mis en avant : tarifs de transport négociés, tarification géolocalisée, référencement naturel (SEO), ainsi que les relations d’Arthaud avec les éditeurs et son stock physique.</span></span></li> </ul> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Amazon est le concurrent direct, disposant d’une envergure et de ressources bien supérieures.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">La plateforme principale a été développée par une agence externe (COex) sur environ deux ans, ce qui tempère le discours sur la « technologie propriétaire / propriété intellectuelle complète ».</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Les agrégateurs répertorient environ 18 concurrents ; la pérennité de l’avantage en matière de logistique et de tarification n’est pas validée de manière indépendante.</span></span></li> </ul> </td> </tr> </tbody> </table> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Modèle économique et évolutivité (65 / 100)</span></span></h3> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Points forts</span></strong></span></span></p> </td> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Faiblesses</span></strong></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Un modèle véritablement reproductible : une base commune de logistique, de technologie, de catalogue et d’acquisition appliquée langue par langue.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Un canal B2B supplémentaire (Lireka Pro) avec une base de clientèle institutionnelle crédible (Alliances françaises, écoles, bibliothèques).</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Un modèle à faible intensité capitalistique par rapport au commerce de détail, qui repose sur des stocks importants, la librairie physique fournissant à la fois les stocks et l’image de marque.</span></span></li> </ul> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">La thèse du multilinguisme n’est pas encore validée : l’anglais n’a été lancé qu’au deuxième trimestre 2026 et l’allemand, l’espagnol et l’italien sont encore à l’étude.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">La livraison gratuite dans le monde entier dépend du maintien de conditions économiques favorables chez les transporteurs et d’un panier d’achat élevé.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">La croissance nécessite de doubler la capacité de l’entrepôt et d’apporter des capitaux supplémentaires, ce qui accroît les risques liés à la mise en œuvre et au financement.</span></span></li> </ul> </td> </tr> </tbody> </table> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Santé financière et bilan (48 / 100)</span></span></h3> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Points forts</span></strong></span></span></p> </td> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Faiblesses</span></strong></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">L’EBITDA du groupe est redevenu légèrement positif en 2025, et la Librairie Arthaud est proche du seuil de rentabilité avec une croissance modérée.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Les pertes de la société d’exploitation se sont réduites chaque année (passant de −1,17 M€ en 2022 à −0,40 M€ en 2025).</span></span></li> </ul> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Lireka SAS a toutefois continué d’enregistrer une perte nette chaque année jusqu’en 2025 (−0,40 million d’euros), ce qui signifie que la société n’est pas encore rentable.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Le groupe est endetté de plusieurs millions d’euros auprès de banques (BPI, Banque Populaire, BNP, CIC) avec des échéances allant jusqu’en 2032.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Le SKI indique que l’entreprise devra lever des capitaux supplémentaires sans garantie de succès — le risque de financement est explicite.</span></span></li> </ul> </td> </tr> </tbody> </table> <h2><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Signaux d’alerte et vérifications d’intégrité</span></span></h2> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:200px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Vérifier</span></strong></span></span></p> </td> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:472px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Constat</span></strong></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:200px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Litige en cours</span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:472px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong>Présents</strong> — Une procédure devant le tribunal des prud’hommes est en cours depuis janvier 2025. Le montant en jeu n’est pas précisé dans les documents.</span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:200px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Cohérence de l’équipe / des fondateurs</span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:472px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong>Incohérence</strong> — Un troisième cofondateur cité dans diverses sources publiques (Robin Mallein, directeur technique) n’apparaît ni dans le dossier de présentation ni dans le SKI, et aucune explication n’est fournie.</span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:200px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Rapprochement des participations</span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:472px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong>Incohérence</strong> — La répartition de la participation des fondateurs varie selon les sources (SKI : 57,93 % pour Bordier ; présentation : 61 % + 8 % ; site web : 69 % au total). Il s’agit probablement de bases de calcul différentes, mais celles-ci ne sont pas harmonisées dans les documents.</span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:200px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Méthodologie d’évaluation</span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:472px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong>Données essentielles manquantes</strong> — La base indépendante utilisée pour l’évaluation initiale de 9 millions d’euros n’est pas fournie ; seul le cadre du multiple de sortie futur est présenté.</span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:200px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Cadre de rentabilité</span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:472px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong>Mise en garde</strong> — Le titre « une économie rentable » repose sur un EBITDA modeste ; la société d’exploitation (Lireka SAS) a tout de même enregistré une perte nette de −0,40 million d’euros en 2025.</span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:200px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Cohérence des avantages fiscaux</span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:472px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong>Incohérence</strong> — Le résumé des informations clés au Royaume-Uni indique « EIS : Non », tandis que la fiche d’information française mentionne « IR-PME 18 % ». L’éligibilité varie selon les investisseurs et n’est pas harmonisée.</span></span></p> </td> </tr> </tbody> </table> <h2><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Remarques sur la qualité des données</span></span></h2> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Les données financières et les indicateurs de progression sont recoupés entre le dossier de présentation, le résumé des informations clés de Crowdcube et la presse publique, et sont cohérents en eux-mêmes — le niveau de confiance dans les faits présentés est donc relativement élevé. Les conditions proposées aux investisseurs sont bien documentées dans le résumé des informations clés. Les principales lacunes concernent le tableau complet de la structure du capital, le statut du troisième cofondateur, la méthodologie d’évaluation initiale, le montant chiffré du litige en cours et le montant final levé (la levée de fonds est en cours). La taille du marché et certains chiffres relatifs à la clientèle/au NPS proviennent des déclarations de l’entreprise et n’ont pas fait l’objet d’une vérification indépendante ; les catégories « Marché » et « Concurrence » ont donc été notées avec plus de prudence.</span></span></p> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#e6f1fb; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:672px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><span style="color:black">Note générée par l’IA à partir d’informations publiques et de documents de l’entreprise publiés sur la plateforme. Les investisseurs doivent effectuer leur propre diligence raisonnable. Les performances passées en matière de levée de fonds ou d’exploitation ne garantissent pas les résultats futurs. Les investissements par financement participatif sont illiquides, à haut risque, et une perte en capital est possible.</span></span></span></p> </td> </tr> </tbody> </table> <p> </p>

See full overview

Ask question

Ask AI about this project

Beta

Démarrer une conversation

Envoyez un message pour commencer à discuter avec l'assistant IA

Like this project?

Platform offering this project

Crowdcube GB

Risk Level

Élevé

Return Level

Élevé

Risk Return Level

Good

Investissement minimum

GBP 10

Financé

GBP 1357,04M