Microinvesting is defined as the practice of investing small, recurring amounts of money, often as little as £1 to £5, into diversified financial markets to build wealth over time. Unlike traditional investing, which typically demands hundreds or thousands of pounds upfront, microinvesting uses automation, fractional shares, and round-up features to make the markets accessible to almost anyone. Platforms like Acorns, Stash, and Moneybox have turned spare change into a genuine entry point for new investors. If you have ever wondered whether investing is only for the wealthy, microinvesting explained simply is this: it is not.

What is microinvesting and how does it actually work?

Microinvesting works through two core mechanisms: round-up features and fractional share purchases. When you pay for a coffee with your debit card, a round-up app automatically rounds that transaction to the nearest pound and sets aside the difference. Once your spare change reaches a threshold (commonly around £5), the platform executes a trade on your behalf, typically buying into a diversified ETF or index fund.

Fractional shares are the second pillar. A single share of a company like Amazon or Apple can cost hundreds of pounds. Fractional shares allow you to own a proportional slice of that share for as little as £1, meaning you gain exposure to high-priced assets without needing the full purchase price. This is what makes microinvesting genuinely democratic rather than just a marketing claim.

Automation is the feature that separates microinvesting from simply saving. Most platforms allow you to set recurring weekly or monthly contributions alongside your round-ups. This creates a form of dollar-cost averaging, where you buy more units when prices are low and fewer when prices are high, smoothing out market volatility over time. The result is a consistent investing habit that requires almost no active decision-making.

Here is how a typical microinvesting journey unfolds in practice:

- Download a microinvesting app (Acorns, Stash, or Moneybox, depending on your region) and link your bank account or debit card.

- Select a portfolio from the pre-built options, usually ranging from conservative bond-heavy funds to aggressive equity-focused portfolios.

- Enable round-ups so every card transaction automatically contributes spare change to your account.

- Set a recurring contribution, even £5 or £10 per week, to accelerate growth beyond round-ups alone.

- Review your portfolio quarterly to confirm the risk level still matches your financial goals.

Pro Tip: Check whether your platform executes trades in real time or waits for a threshold. Execution delays are common and mean your money may sit uninvested for several days after a round-up.

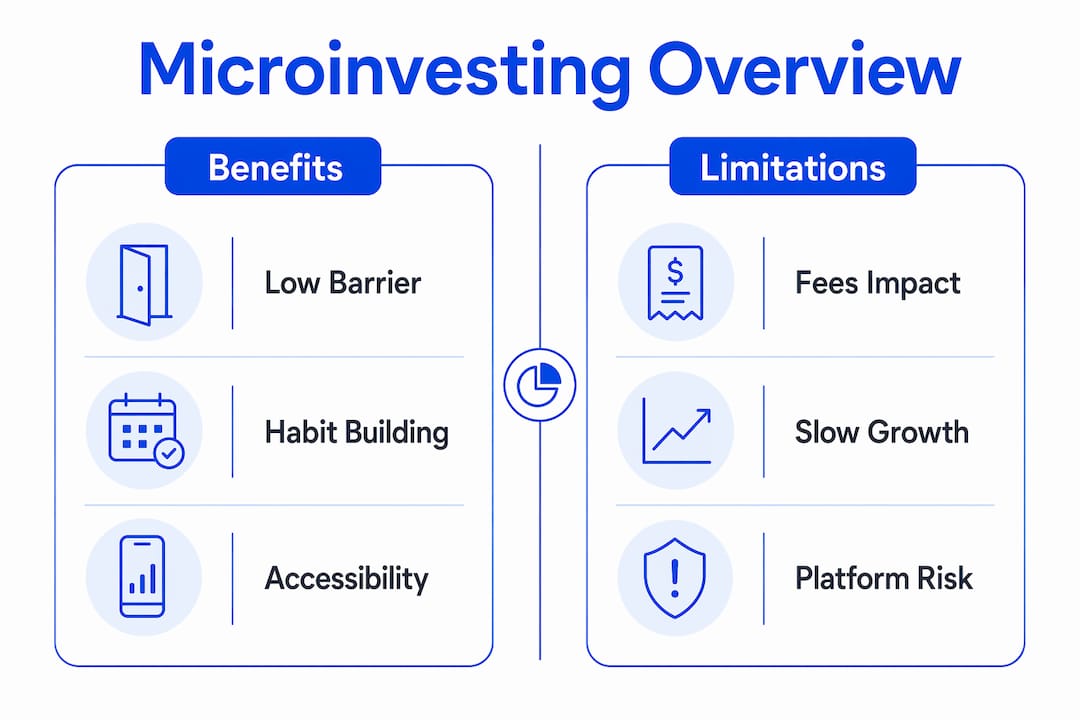

What are the benefits of microinvesting?

The most compelling benefit of microinvesting is accessibility. Platforms often have £0 minimums to start, which removes the single biggest barrier that stops new investors from ever beginning. You do not need a financial adviser, a brokerage account, or a lump sum. You need a smartphone and a linked bank card.

Beyond access, the benefits of microinvesting include:

- Habit formation. Consistent, automated contributions build the discipline of investing before you even notice the money leaving your account. This psychological shift, from spending first to investing first, is genuinely valuable.

- Financial literacy. Watching a real portfolio respond to market movements teaches you more about investing than any textbook. Even £1 a week contributes to compounding growth over long periods, and seeing that growth firsthand builds confidence.

- Compounding over time. Small amounts invested consistently compound meaningfully over decades. A 20-year-old investing £10 per week at a 7% average annual return will accumulate significantly more than someone who waits until they have a "proper" amount to invest.

- Diversification from day one. Most microinvesting apps place your money into ETFs and index funds, giving you instant exposure to hundreds of companies rather than a single stock.

- Low emotional friction. Because the amounts are small, new investors are less likely to panic-sell during market dips, which is one of the most damaging behaviours in long-term investing.

Microinvesting suits beginners, students, freelancers with irregular income, and anyone who wants to start building an investing habit without committing large sums. It is less suited to experienced investors seeking active portfolio control or those with specific tax-efficient strategies already in place.

What are the limitations and pitfalls of microinvesting?

Microinvesting is not without its drawbacks, and understanding them upfront will save you frustration later. The most significant issue is fees. Flat-fee monthly subscriptions can outweigh returns on tiny investments, effectively making microinvesting a net loss for users with very small balances. A £1 monthly fee on a £20 balance represents a 5% annual cost, far exceeding what most ETFs return.

Pro Tip: Always calculate your platform fee as a percentage of your actual balance, not just as an absolute number. A £3 monthly fee sounds trivial but is devastating on a £100 portfolio.

The second major pitfall is portfolio unawareness. Many users rely entirely on default app settings without understanding what they actually own. Microinvesting portfolios typically hold ETFs or index funds, but the specific allocation between equities, bonds, and commodities varies significantly between platforms and portfolio tiers. Failing to review this periodically means your risk exposure may drift away from what you actually need.

Other common limitations include:

- Execution delays. Platforms often wait until accumulated round-ups reach a threshold before investing, meaning your money sits idle and uninvested for days or weeks.

- Insufficient for major financial goals. Microinvesting alone will not fund a comfortable retirement. It is a starting point, not a complete strategy.

- Limited investment choice. Most apps restrict you to pre-built portfolios, removing the flexibility that experienced investors expect.

| Limitation | Impact on the investor |

|---|---|

| Flat monthly fees | Can exceed returns on small balances, creating a net loss |

| Execution delays | Spare change sits uninvested until threshold is reached |

| Portfolio unawareness | Risk level may not match evolving financial goals |

| Insufficient scale | Cannot replace a full retirement savings strategy |

How to start microinvesting: practical steps and app comparison

Starting microinvesting takes less than 30 minutes if you approach it methodically. The first step is defining your goal. Are you building an emergency fund, practising investing before committing larger sums, or genuinely trying to grow long-term wealth? Your answer shapes which platform and portfolio type you should choose. Crowdinform's guide on analysing investment platforms is a useful reference for evaluating features systematically.

Follow these steps to get started:

- Define your goal and monthly budget. Decide how much you are comfortable contributing beyond round-ups. Even £20 per month makes a material difference over years.

- Compare platform fees carefully. A percentage-based fee (e.g., 0.25% annually) is almost always better than a flat monthly fee for small balances.

- Check minimum investment requirements. Most leading apps have no minimum, but some require a small initial deposit to activate your account.

- Select a portfolio that matches your risk tolerance. Conservative portfolios hold more bonds; aggressive ones hold more equities. Choose based on your timeline, not your mood.

- Enable automation. Set up both round-ups and a recurring contribution to maximise consistency.

- Review quarterly. Check your portfolio allocation every three months and adjust if your goals or risk tolerance have changed.

When comparing microinvesting apps, the differences between platforms matter more than most beginners realise:

| Platform | Fee structure | Key feature | Best suited for |

|---|---|---|---|

| Acorns | From $3/month | Round-ups + recurring contributions | US-based beginners |

| Stash | From $3/month | Fractional shares + financial education | US beginners wanting stock picks |

| Moneybox | 0.45% annually + £1/month | Round-ups + Stocks and Shares ISA | UK investors wanting tax efficiency |

| Trading 212 | Free (0% commission) | Fractional shares + pie investing | UK/EU investors wanting flexibility |

The microinvesting apps comparison above highlights one critical insight: regional availability matters. Acorns and Stash are US-focused, while Moneybox and Trading 212 serve UK and European investors more effectively. Always verify that a platform is regulated in your country before depositing funds. For a broader platform comparison guide covering European options, Crowdinform aggregates reviews across 500 platforms to help you make an informed choice.

Key takeaways

Microinvesting works because it removes the capital and behavioural barriers that stop most people from ever starting, but it requires fee awareness and periodic portfolio review to deliver genuine long-term value.

| Point | Details |

|---|---|

| Low barrier to entry | Most platforms require £0 minimum, making investing accessible to anyone with a smartphone. |

| Automation drives consistency | Round-ups and recurring contributions create investing habits without active effort. |

| Fees can erode small balances | Always calculate platform fees as a percentage of your actual balance before committing. |

| Portfolio review is non-negotiable | Default app settings may not match your evolving risk tolerance; check quarterly. |

| A starting point, not a full strategy | Microinvesting builds confidence and habits; transition to broader strategies as your capital grows. |

Why I think microinvesting deserves more credit than it gets

Most financial commentary either dismisses microinvesting as "not serious investing" or oversells it as a path to financial freedom. Both positions miss the point entirely.

What I have observed, tracking the European fintech and crowdfunding space through Crowdinform, is that the investors who engage most confidently with complex opportunities, such as P2P lending, real estate crowdfunding, and startup equity, are often those who started with microinvesting apps. The habit of watching a portfolio, understanding ETF composition, and tolerating short-term volatility is not trivial. It is the foundation that makes everything else possible.

The genuine risk I see is not that people invest too little through microinvesting. It is that they invest and then forget. Automation is powerful, but it is not a substitute for understanding. Experts caution that users should monitor portfolio allocations periodically rather than relying fully on default settings, and I agree completely. The investors I respect most treat their microinvesting app as a training ground, not a destination.

My honest advice: use microinvesting to build the habit and the confidence. Then, once you understand how markets move and how your own risk tolerance behaves under pressure, graduate to platforms that offer real diversification across asset classes. The discipline you build in the early stages is worth far more than the returns on your first £500.

— Jevgenijs

Ready to grow beyond microinvesting?

Once you have built your investing habit through microinvesting, the natural next step is expanding into assets that offer greater return potential and genuine diversification. Crowdinform aggregates and reviews over 500 European crowdfunding platforms, covering loans (P2P), real estate, and startup equity, so you can compare opportunities with the same confidence you bring to choosing a microinvesting app. Our AI copilot analyses individual projects and provides structured reviews, helping you move from spare-change investing to purposeful portfolio building. Explore investment opportunities on Crowdinform and discover where your next pound could work hardest.

FAQ

What is microinvesting in simple terms?

Microinvesting is the practice of investing very small amounts of money, often just a few pounds at a time, into diversified funds or fractional shares through an automated app. It is designed to make investing accessible to people with limited capital or no prior experience.

Is microinvesting worth it for beginners?

Microinvesting is worth it as a starting point because it builds consistent investing habits and introduces you to real market dynamics with minimal financial risk. The main caveat is that platform fees must be low relative to your balance, otherwise returns are eroded before they compound.

How do round-up features work in microinvesting apps?

A round-up feature automatically rounds each card transaction to the nearest pound and transfers the difference to your investment account. Most platforms wait until round-ups accumulate to a set threshold before executing a trade, so your money may not be invested instantly.

What is the difference between microinvesting and traditional investing?

Traditional investing typically requires a meaningful lump sum, active account management, and direct selection of individual stocks or funds. Microinvesting automates contributions, uses fractional shares, and requires no minimum deposit, making it far more accessible but also more limited in scope and return potential.

Can microinvesting replace a pension or retirement plan?

Microinvesting alone is insufficient for retirement because the amounts invested are typically too small to generate the capital needed over a working lifetime. It works best alongside a pension, ISA, or broader investment strategy rather than as a replacement for one.