Startup investment has a reputation problem. Many European investors assume it belongs exclusively to the world of Silicon Valley-style tech unicorns, reserved for venture capitalists with enormous funds and connections few possess. That assumption is wrong, and it is costing ordinary investors real opportunity. Across Europe, exciting capital flows are reshaping sectors from renewable energy to real estate, opening doors to investors who understand the mechanics. This guide clarifies what startup investment actually means, compares the main investor types, explores how sector dynamics shift deal structures, and maps the regulatory landscape that makes cross-border investing increasingly accessible. 🚀

Key Takeaways

| Point | Details |

|---|---|

| Startup investment basics | It means providing capital to early-stage companies for high growth potential and returns. |

| Angel vs VC differences | Angels invest earlier and offer personal involvement, while VCs are later-stage and more structured. |

| Sector-specific approaches | Investment mechanics adapt for technology, real estate, and renewable energy with tailored risk checks. |

| European frameworks | EU regulations like EuVECA open cross-border investing and ensure fund eligibility. |

| Crowdinform as a tool | Crowdinform connects European investors to diverse startup, real estate and energy opportunities. |

What defines a startup investment?

At its core, startup investment is capital provided to an early-stage company, often at pre-seed, seed, or Series A stage, in exchange for an ownership stake or a convertible instrument, with the investor expecting a high-growth return rather than fixed repayment. That distinction matters enormously. You are not lending money to be paid back on schedule; you are buying a share of a company’s future.

Convertible instruments, such as convertible notes or SAFEs (Simple Agreements for Future Equity), allow investors to provide capital that converts into equity at a future funding round, usually at a discount. This structure protects early investors while giving founders flexibility before a valuation is agreed. Understanding these mechanics puts you in a far stronger position when evaluating deals.

The startup investing advantages are most visible when investors focus on growth rather than yield. Key characteristics of startup investment include:

-

Capital at risk: Unlike bonds or savings accounts, your principal is not guaranteed

-

Equity or convertible instruments: Ownership upside rather than interest payments

-

Long time horizons: Most exits take five to ten years via acquisition or IPO

-

High variance returns: A small number of winners can compensate for many losses

-

Active or passive roles: Some investors take board seats; others remain silent shareholders

“Startup investment is not about steady income. It is about backing teams and ideas with the potential to generate outsised returns over a longer horizon, where patience and diligence are the investor’s greatest assets.”

This mindset shift, from income to growth, is the first step toward thinking like a successful startup investor in Europe.

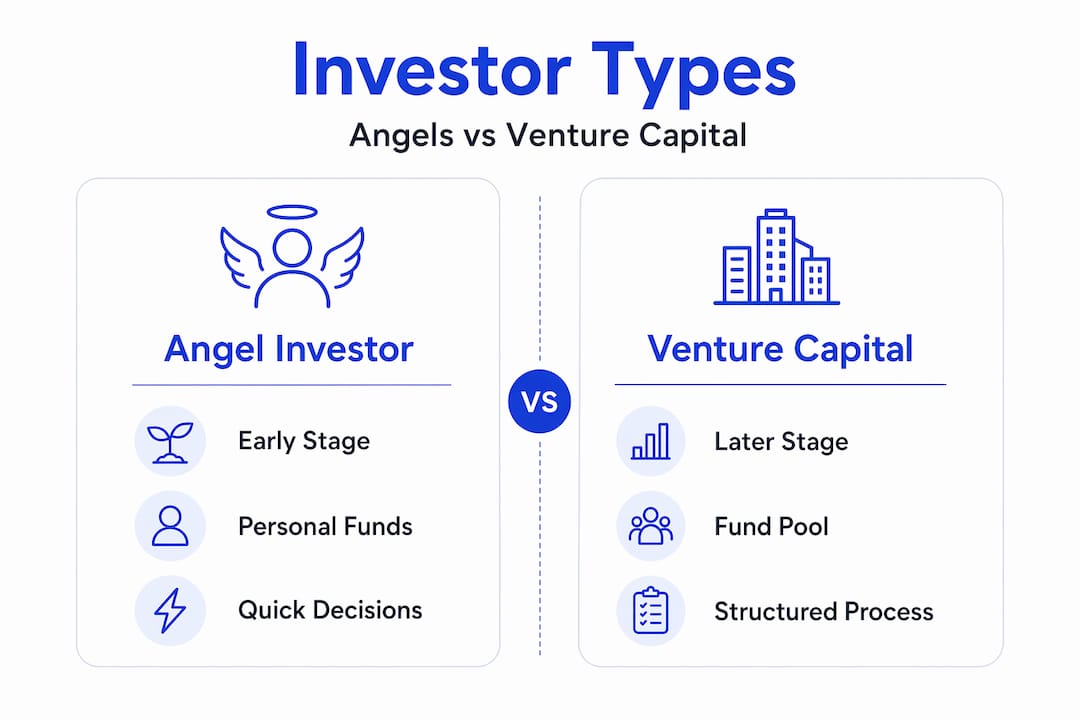

Types of startup investors: angels vs venture capital

Understanding who invests, and how, helps you position yourself effectively in the European market. Angel investors typically invest early, at seed or even concept stage, in exchange for equity or convertible debt, while venture capital (VC) firms typically invest later, at Series A and beyond, in exchange for equity. Both target high growth rather than fixed-income repayment.

The differences run deeper than timing alone. According to angel vs VC nuance, the distinction also includes how quickly capital is deployed, who leads the round, and the depth of operational or strategic support provided. Angels often fill critical earlier gaps and de-risk rounds before larger institutional investors step in.

Here is a side-by-side comparison of the two main investor types:

| Feature | Angel investor | Venture capital firm |

|---|---|---|

| Stage | Pre-seed / seed | Series A and beyond |

| Capital source | Personal funds | Institutional / LP funds |

| Decision speed | Fast (weeks) | Slower (months) |

| Ticket size | €10k to €500k | €1m to €50m+ |

| Operational support | Hands-on mentorship | Strategic board presence |

| Portfolio focus | Concentrated bets | Diversified fund mandate |

| European example | Business angel networks | EIF-backed VC funds |

For European investors who are newer to startup allocation, crowdinvesting in Europe offers an accessible third path that sits between informal angel investing and institutional VC. Crowdinvesting platforms allow smaller ticket sizes, often from €500 upwards, reducing the barrier to entry significantly.

Pro Tip: Before choosing between angel-style investing and fund-based VC exposure, assess your time availability. Angels who offer genuine mentorship and sector expertise create more value and often negotiate better deal terms. If you cannot commit that time, a fund structure or crowdinvesting platform offers a more realistic option.

Here is a practical step-by-step approach for first-time European startup investors:

-

Define your risk tolerance and decide what percentage of your portfolio you can genuinely afford to lose entirely

-

Choose your sector focus based on your professional expertise, whether technology, real estate, or energy

-

Select your investment vehicle, whether direct angel investing, syndicate participation, or a crowdinvesting platform

-

Conduct basic due diligence covering team, market size, financials, and competitive position

-

Diversify across at least eight to twelve investments to create a meaningful probability of capturing a high-return outcome

Understanding investment diversification is particularly critical in startup portfolios, where the failure rate can be high even with excellent diligence.

Investment mechanics: how sectors reshape startup deals

One of the most underappreciated insights in startup investment is that the mechanics remain consistent across sectors, but the diligence focus and deal structure shift significantly. Startup investment mechanics are sector-agnostic, but deal structures and diligence focus can shift across technology, real estate infrastructure, and renewable-energy-adjacent opportunities. The core equity exchange and growth thesis apply universally.

Here is how diligence priorities differ across three key sectors:

| Sector | Primary diligence focus | Common deal structure | Key risk factor |

|---|---|---|---|

| Technology | Product scalability, IP, team | Equity / SAFE | Market competition |

| Real estate | Asset resilience, planning consent | Convertible note / revenue share | Regulatory and valuation risk |

| Renewable energy | Grid reliability, offtake agreements | Project equity / bond hybrid | Technology performance |

For renewable energy investing, the diligence process includes assessing the reliability of energy generation assets, the security of power purchase agreements (PPAs), and government subsidy frameworks. These factors are less relevant in a pure software startup but absolutely central to a solar or wind venture. 🌱

Real estate startups, particularly those building proptech platforms or developing sustainable residential assets, sit at an interesting crossroads. Real estate investing steps in Europe increasingly involve climate resilience assessments, especially as ESG (environmental, social, and governance) requirements tighten across the EU.

Additional sector-specific considerations include:

-

Technology: Revenue growth rate and customer acquisition cost (CAC) relative to lifetime value (LTV) dominate early evaluation

-

Real estate: Location fundamentals, planning timelines, and macroeconomic interest rate sensitivity matter enormously

-

Renewable energy: Feed-in tariffs, subsidy longevity, and grid connection timelines are non-negotiable due diligence items

-

Cross-sector ventures: Increasingly, energy meets property in developments combining solar generation with residential or commercial assets

Pro Tip: When analysing real estate crowdfunding deals specifically, request the independent asset valuation report and check the loan-to-value (LTV) ratio. A ratio above 75% signals elevated risk, especially in a rising interest rate environment. This single data point can save significant capital.

The convergence between property and energy is creating genuinely exciting new deal categories across European markets, from energy-positive residential developments in Germany to community solar projects in Spain and Portugal.

Navigating European frameworks: EuVECA, cross-border, and regulation

Europe’s regulatory landscape is one of its most powerful features for startup investors, yet it remains poorly understood by many. The right framework knowledge transforms what feels like a maze into a structured opportunity.

The most important instrument to know is EuVECA, which creates an EU-wide marketing passport for qualifying venture capital fund managers, subject to conditions. In practical terms, this means a qualifying fund registered in, say, Luxembourg or the Netherlands can legally market to investors across all EU member states without needing a separate authorisation in each country.

Key EuVECA eligibility requirements include:

-

Fund size: The fund must be below the €500 million threshold for the standard AIFMD (Alternative Investment Fund Managers Directive) regime

-

Investment mandate: At least 70% of committed capital must be invested in qualifying portfolio undertakings, typically unlisted SMEs (small and medium-sized enterprises)

-

Manager registration: Fund managers must be registered with their national competent authority

-

Investor eligibility: The framework primarily targets professional investors, though provisions exist for some well-informed retail investors above defined thresholds

-

Geographic flexibility: The passport allows cross-border fundraising without duplicating regulatory burdens

Beyond EuVECA, crowdlending in Europe is increasingly governed by the European Crowdfunding Service Providers (ECSP) regulation, which came into full effect in 2023 and provides a harmonised licence for platforms operating across EU borders. This gives retail investors access to business loans and equity crowdfunding on regulated platforms with standardised disclosure requirements.

Key statistic: Europe’s venture environment is shaped by selectivity and valuation sensitivity, with deal activity and capital deployed sometimes diverging, reflecting stricter investor underwriting standards. This means quality of deal matters more than quantity, and investors who understand how to evaluate fundamentals have a genuine edge.

Additional regulatory trends shaping European startup investment:

-

SFDR (Sustainable Finance Disclosure Regulation): Funds must classify and disclose how sustainability risks are integrated, making ESG transparency a baseline expectation

-

DORA (Digital Operational Resilience Act): Relevant for fintech and digital startups, raising technology risk standards

-

State Aid rules: Influence how governments can co-invest alongside private capital, particularly in renewable energy

-

National co-investment schemes: Countries like France (Bpifrance), Germany (KfW), and the Netherlands (RVO) actively co-invest in startups, reducing risk for private investors

Regulation, handled well, is not a burden. It is a signal of market maturity, and in Europe, that maturity is accelerating.

A fresh perspective: what most guides miss about startup investing in Europe

Most startup investment guides focus almost entirely on technology. They talk about SaaS metrics, software valuations, and consumer apps. What they consistently miss is the extraordinary opportunity expanding across European renewable energy and real estate, sectors where early-stage capital is genuinely scarce and impact is measurable.

This matters practically, not just philosophically. When you invest in a seed-stage solar energy company or a sustainable housing proptech platform, you are often entering at lower valuations, with clearer physical assets underpinning the business, and with stronger alignment to long-term EU policy tailwinds. The risk profile is different from pure software, but so is the potential for uncorrelated returns.

Another thing most guides underplay is the role of operational support from early investors. Angel vs VC nuance is not just about stage or deal size. It is also about who fills critical gaps before institutional money arrives. In European markets, where venture ecosystems outside London, Berlin, and Paris are still maturing, an experienced angel investor who provides regulatory guidance, customer introductions, or technical credibility can be the difference between a startup surviving its first two years or not.

We would also argue that sector expertise, not just financial capital, is a meaningful competitive advantage for European startup investors. If you have spent years in energy infrastructure, real estate development, or sustainability consulting, you bring diligence capabilities and network access that no generalist fund can replicate. That knowledge is an asset. Use it.

Finally, many investors underestimate how powerful diversification across sectors, not just companies, can be. A portfolio combining renewable energy perspective investments with real estate ventures and technology plays behaves very differently from a single-sector concentration. The correlation between these categories remains relatively low, which means sector diversification genuinely reduces portfolio volatility while maintaining upside. That is the kind of structural advantage that compounds over time. 🎂

How Crowdinform empowers European startup investors

Navigating hundreds of crowdfunding platforms, comparing deal terms, and tracking investment projects across sectors takes significant time and expertise. That is precisely why Crowdinform exists.

Crowdinform is Europe’s leading aggregator and review platform for crowdfunding services, covering over 500 platforms with independently sourced data. Think of it as the TripAdvisor for crowdfunding: transparent, comprehensive, and AI-powered. Using the built-in AI copilot, you can receive personalised project reviews, explore investments across technology, real estate, and renewable energy sectors, and build a diversified portfolio with confidence. Whether you are an experienced impact investor or just beginning your startup investment journey, Crowdinform gives you the tools to invest smarter, not harder. Ready to explore? 🚀

Frequently asked questions

What is the main risk of startup investments in Europe?

The main risk is significant or total capital loss if the startup fails, particularly given that deal scrutiny is rising and European valuations are under pressure. Diversifying across multiple investments substantially reduces this concentration risk.

How does the EuVECA regulation help investors?

EuVECA enables qualifying fund managers to market their venture capital funds across all EU member states under a single passport, simplifying cross-border access for European investors and reducing administrative duplication.

Are startup investments only for technology companies?

No. Deal structures and diligence differ by sector, but the equity-based mechanics of startup investment apply equally to real estate and renewable energy ventures, both of which are expanding rapidly across Europe.

What distinguishes angels from venture capital firms?

Angels invest early using personal capital and often provide hands-on mentorship with faster decision-making; venture capitalists invest at later stages with larger institutional funds, more structured due diligence, and strategic board-level involvement.