Key Takeaways

|

Point |

Details |

|---|---|

|

Lower entry barriers |

Fractional ownership allows anyone to invest in high-value assets with smaller amounts. |

|

Diverse applications |

You can gain access to real estate, startups, and private markets through fractional models. |

|

Regulatory complexity |

Check the rules: legal treatment varies across asset types and jurisdictions in Europe. |

|

Liquidity potential |

Selling your share is easier on some platforms, but not always guaranteed in practice. |

|

Do your due diligence |

Always review governance, resale mechanisms, and investor protections before committing. |

What is fractional ownership?

Fractional ownership is exactly what it sounds like: instead of purchasing an entire asset outright, you buy a proportional share of it. That share entitles you to a corresponding proportion of the income it generates, the capital appreciation it achieves, and, in most structures, a defined mechanism to eventually sell or transfer your stake.

This concept is not entirely new. Syndicates and joint ventures have existed in property and private equity for decades. What has changed is scale, accessibility, and technology. Digital platforms now allow hundreds or even thousands of investors to co-own a single asset, with legal structures and automated income distribution making the experience far more manageable than traditional syndication.

The most common legal structures used in fractional ownership include:

-

Co-ownership agreements: Investors hold a direct, undivided interest in the asset itself. This is straightforward but can complicate decision-making when many parties are involved.

-

Special purpose vehicle (SPV): A dedicated legal entity (typically a limited company or LLC equivalent) is created to hold the asset. Investors own shares in the SPV rather than the asset directly. This is the most widely used structure in European real estate crowdfunding.

-

Digital tokens: Blockchain-based tokens represent fractional stakes. Depending on their classification, these may fall under crypto-asset regulation or traditional securities law.

When it comes to investing in real estate through fractional structures, the mechanics are well established. As noted in recent analysis of the sector, fractional ownership is implemented via legal structures such as co-ownership or holding via an SPV, with investors receiving returns relative to their share, often with a defined transfer or resale mechanism.

“Fractional ownership is not simply about making expensive things cheaper. It is about restructuring access to opportunity, governance, and long-term wealth creation.”

The appeal extends well beyond real estate. Private equity, venture capital, infrastructure, fine art, and even intellectual property rights are increasingly being fractionalised. For European investors seeking genuine portfolio diversification without committing hundreds of thousands of euros to a single asset, this is a genuinely exciting development. 🌱

How fractional ownership works: Models and examples

Understanding the concept is one thing. Seeing how it plays out in practice across different asset classes is where the real insight lies. Let us walk through the three dominant models you will encounter as a European investor.

Real estate via SPV

This is the most mature model. A platform identifies a property, creates an SPV to hold it, and then offers shares in that SPV to investors. You select the property, decide how much to invest, and the platform handles property management, rent collection, and income distribution. Returns flow to you proportionally, typically as quarterly or monthly distributions.

Private equity slices

Private market equity is increasingly being fractionalised into smaller, tradable units. The goal is to maintain proportional economic exposure to an underlying private allocation while lowering access thresholds for individual investors. This means you can gain exposure to a late-stage startup or a private fund that would otherwise require a minimum commitment of €100,000 or more, for as little as €500 to €5,000.

Tokenisation

Tokenisation converts the value of a real-world asset into digital tokens on a blockchain. Each token represents a fractional stake. Tokenisation enables fractional ownership by converting property value into digital tokens with EU-wide regulatory coverage that depends on whether the tokens are treated as crypto-assets under MiCA or as financial instruments under securities law. This distinction matters enormously for investor protections and platform obligations.

Here is a quick comparison of the three models:

| Feature | SPV (real estate) | Private equity slices | Tokenised assets |

|---|---|---|---|

| Minimum investment | €500 to €5,000 | €500 to €10,000 | €50 to €1,000 |

| Liquidity | Low to medium | Low | Medium (secondary market) |

| Regulatory framework | Securities law | Securities law | MiCA or securities law |

| Income type | Rental yield + capital gain | Capital gain | Varies by asset |

| Governance rights | Via SPV shares | Limited | Token-specific |

Step-by-step: how a typical fractional investment works

-

Select an offer: Browse available opportunities on a platform, reviewing projected yields, asset details, and legal structure.

-

Commit your investment: Transfer funds and receive your proportional share (SPV shares or tokens).

-

Receive income: Rental income or dividends are distributed to your account on a regular schedule.

-

Monitor performance: Track your investment’s performance via the platform dashboard.

-

Exit your position: Sell your stake via the platform’s secondary market, a structured buyback, or at the end of the investment term.

Pro Tip: Always check whether a platform offers a secondary market before investing. Without one, your exit options may be limited to the end of a fixed term, which could be three to seven years away.

Investing in startups through fractional private equity models is particularly exciting right now, given the volume of high-quality European companies seeking growth capital outside traditional venture channels. The opportunity set is expanding rapidly.

Benefits and potential drawbacks of fractional ownership

After understanding the structural models, it is important to weigh the real-world pros and cons with clear eyes. Fractional ownership offers genuinely compelling advantages, but it is not without meaningful risks.

Key benefits

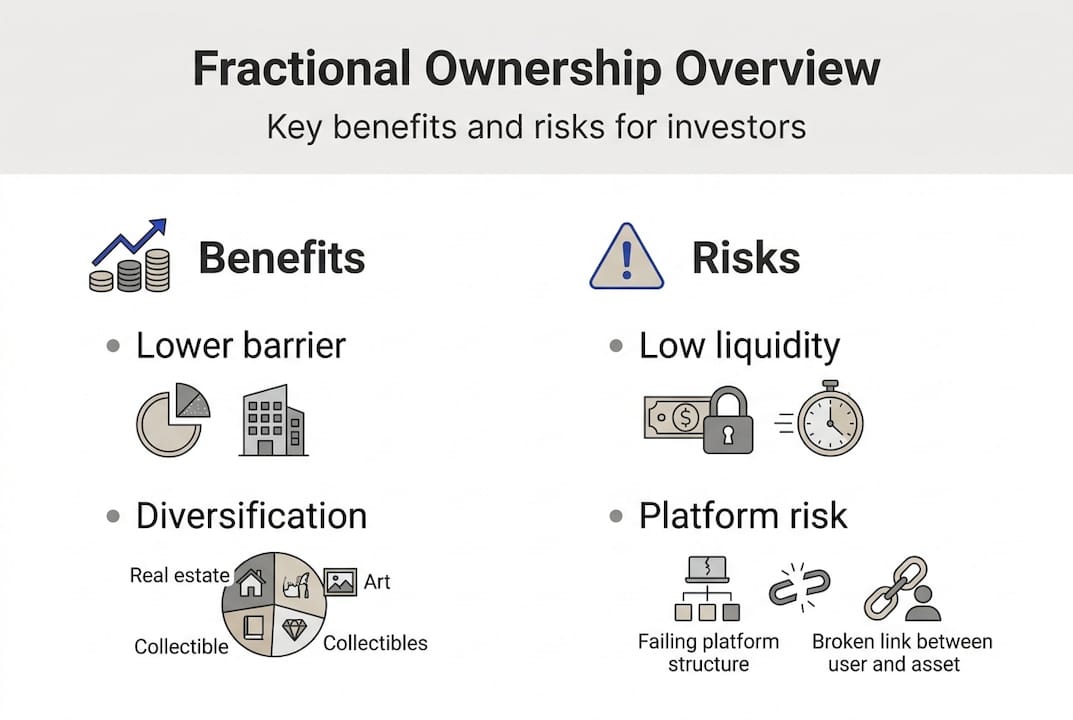

-

Lower entry barriers: You can invest in premium assets with €500 to €5,000 rather than €500,000. This opens doors that were previously closed to most retail investors.

-

Portfolio diversification: Instead of concentrating capital in one property or one company, you can spread it across multiple assets, geographies, and sectors.

-

Passive income potential: Rental income, dividend distributions, and interest payments can provide steady cash flow without active management responsibilities.

-

Transparency: Reputable platforms provide detailed documentation, regular reporting, and clear governance structures.

-

Access to institutional-grade assets: Commercial real estate, logistics hubs, and private equity deals that institutions favour are now accessible to individual investors.

Potential drawbacks

-

Liquidity risk: This is the most significant concern. Empirical research suggests tokenisation and fractionalisation can increase liquidity and access opportunities, but observed liquidity benefits can depend on specific institutional design features, such as limited buyback of tokens over short horizons. In plain terms: just because an asset is fractionalised does not mean you can sell your stake quickly.

-

Regulatory uncertainty: The legal landscape for tokenised assets is still evolving across Europe. Classification under MiCA versus securities law affects your protections significantly.

-

Shared governance: When hundreds of investors co-own an asset, individual decision-making power is minimal. You are trusting the platform and its management team to act in your interests.

-

Platform risk: If the platform operating your investment faces financial difficulties, your investment may be at risk regardless of the underlying asset’s performance.

-

Fee structures: Management fees, platform fees, and exit fees can erode returns. Always model net returns, not gross figures.

|

Factor |

Traditional direct ownership |

Fractional ownership |

|---|---|---|

|

Capital required |

High (€100k+) |

Low (€500+) |

|

Diversification |

Limited |

High |

|

Liquidity |

Variable |

Variable to low |

|

Management burden |

High |

Low |

|

Governance control |

Full |

Minimal |

|

Regulatory clarity |

Established |

Evolving |

Pro Tip: Before committing capital, request the platform’s legal opinion on the investment structure and confirm how investor rights are protected in the event of platform insolvency. This is a basic due diligence step that many first-time investors skip.

The balance here is genuinely nuanced. Fractional ownership is not a shortcut to risk-free returns. It is a structural innovation that redistributes access and opportunity, with its own specific risk profile that you must understand before investing.

How to get started with fractional ownership in Europe

With the benefits and risks clearly in view, here is a practical roadmap for European investors who want to begin exploring fractional ownership opportunities. The process is more straightforward than many expect, but it rewards careful preparation.

-

Decide on your asset class: Real estate offers the most mature fractional infrastructure in Europe, with established SPV structures and a growing number of regulated platforms. Private equity slices offer higher potential returns with higher risk. Tokenised assets offer the most liquidity potential but the most regulatory complexity. Choose based on your risk appetite and investment horizon.

-

Understand the regulatory environment: EU-wide regulatory coverage varies depending on whether tokens are treated as crypto-assets under MiCA or as financial instruments under the Prospectus Regulation. For SPV-based real estate, the European Crowdfunding Service Provider (ECSP) Regulation provides a harmonised framework across member states. Knowing which rules apply to your chosen platform protects you from unpleasant surprises.

-

Research platforms thoroughly: Look for platforms with a track record, transparent governance, clear exit mechanisms, and regulatory authorisation. Check whether they are licensed under the ECSP Regulation or hold relevant national licences. Read independent reviews and compare platforms before committing.

-

Read all terms carefully: Pay particular attention to resale mechanisms, fee structures, investor rights in the event of default, and the timeline for exits. The fine print is where the real structure of your investment lives.

-

Start small and diversify: Your first fractional investment should be a learning experience as much as a financial one. Invest a modest sum across two or three different offers to understand how the process works in practice before scaling up.

-

Monitor and review regularly: Fractional ownership is passive, but it is not set-and-forget. Review platform communications, financial reports, and market conditions at least quarterly.

European investment platforms vary enormously in quality, focus, and regulatory standing. Taking time to compare them carefully before investing is one of the most valuable things you can do as a new fractional investor.

Pro Tip: Diversifying across asset classes (for example, one real estate offer, one startup equity offer, and one tokenised asset) gives you a natural hedge against sector-specific downturns while you learn how each model performs in practice.

The European fractional ownership market is expanding at pace, with new platforms, new asset classes, and improving regulatory clarity creating a genuinely exciting environment for informed investors. 🎂

Fractional ownership: Our view on what matters most

Stepping back, here is our candid view on what fractional ownership means for the smart European investor, and where we think the conventional narrative misses the point.

Most coverage of fractional ownership focuses on technology. Blockchain, tokenisation, and digital platforms are presented as the story. We think that framing is misleading. The real innovation is not technological. It is structural and social. Fractional ownership matters because it redistributes access to wealth-generating assets that were previously gatekept by capital requirements, geography, and professional networks.

That said, democratisation without proper governance is simply a new way to lose money. The investors who will benefit most from fractional ownership are not those who chase the lowest minimum investment or the flashiest platform interface. They are the investors who ask hard questions: What are my actual legal rights as a fractional owner? What happens if the platform fails? How is the exit mechanism structured, and who controls it?

We have observed a troubling pattern in the European market: investors assume that because an asset is fractionalised, it is also liquid. This is not always true. Liquidity depends on the specific design of the investment structure, the existence and depth of a secondary market, and the willingness of other investors to buy your stake. None of these are guaranteed.

Our honest recommendation is this: treat fractional ownership as a genuine asset class that requires the same rigour you would apply to any other investment. Study the governance structure. Understand your rights. Model your returns net of all fees. And never invest in a fractional offer you cannot afford to hold until the end of its stated term, because that may be exactly what you are required to do.

Fractional ownership is one of the most exciting structural shifts in European investing right now. But excitement is not a substitute for due diligence. The investors who approach it with both enthusiasm and discipline are the ones who will genuinely benefit. 🌱

Explore fractional ownership opportunities with Crowdinform

If you are ready to put these insights into practice, Crowdinform is the ideal starting point for your research. Think of us as the TripAdvisor of European crowdfunding and fractional investment platforms: we aggregate data, reviews, and performance information from over 500 platforms across Europe, so you can compare opportunities with confidence.

Our AI copilot helps you explore individual investment projects, review platform credentials, and assess opportunities based on your specific goals and risk profile. Whether you are drawn to fractional real estate, private equity slices, or tokenised assets, you can discover fractional investment options that are transparently curated and independently reviewed. European investors deserve access to the same quality of information that institutions have always enjoyed. That is exactly what Crowdinform provides.

Frequently asked questions

How does fractional ownership differ from timeshare?

Fractional ownership provides actual equity in the asset with rights to proportional returns and capital appreciation, while timeshares only offer usage rights for a set period with no ownership stake or financial upside.

Are fractional ownership tokens considered crypto-assets in the EU?

They may be classified as crypto-assets if they do not qualify as financial instruments, in which case MiCA applies. If they do qualify as financial instruments, EU regulatory coverage falls under securities law instead, including the Prospectus Regulation.

Can I sell my fractional ownership stake easily?

Liquidity varies considerably by platform and structure. Some platforms offer secondary markets for peer-to-peer resale, but liquidity benefits can depend on specific institutional design features, and selling is never guaranteed.

Is fractional ownership legal across all of Europe?

Fractional ownership is permitted across the EU, but the applicable regulations differ based on asset type and investment structure. Always confirm which national and EU rules apply to your specific platform and offer before investing, as regulatory coverage depends on the exact classification of the instrument involved.