Crowdcube • Lireka

Aktien-Crowdfunding

Lireka

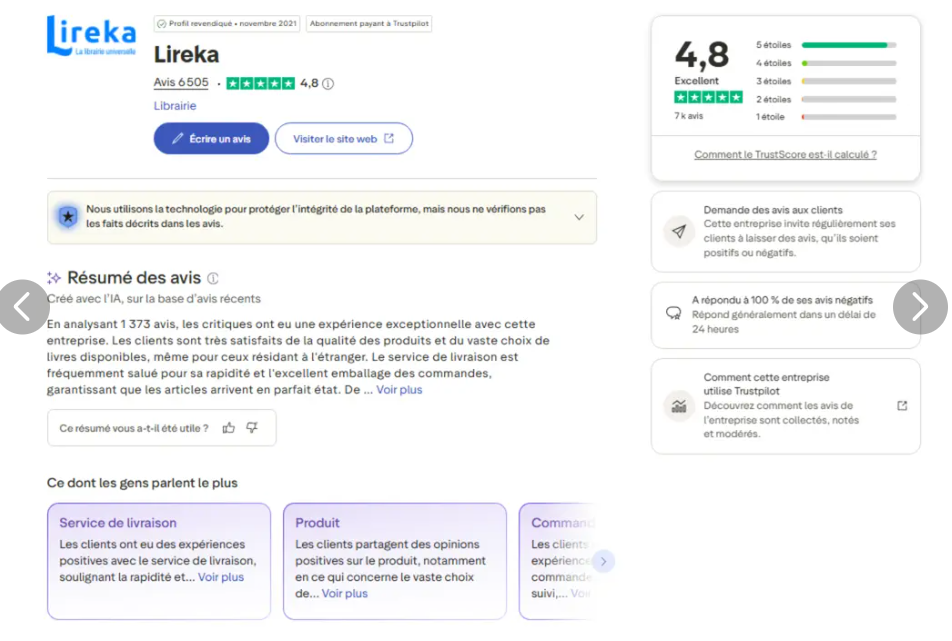

Lireka ist der erste Online-Buchhandel, der KOSTENLOSEN internationalen Versand anbietet, und macht Kultur zugänglich, indem er Bücher weltweit versendet. Das von zwei ehemaligen Amazon-Mitarbeitern gegründete Unternehmen bietet ein umfangreiches Sortiment von fast 2 Millionen Titeln zu attraktiven Preisen.

Key project data

Target amount

3,0 MEUR

Valuations

9,0 MEUR

Enddatum

2026-07-11

Would AI invest?

64/100

1

100

KI-generierte Übersicht

AI project overview

Condensed summary based on project data

<h1><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><em>Die erste internationale Buchhandlung mit kostenlosem weltweiten Versand – wir versenden französisch- und englischsprachige Bücher an Auswanderer und Frankophone weltweit.</em></span></span></h1> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Branche</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Internationale Online-Buchhandlung (E-Commerce / Buchexport) mit angeschlossener stationärer Buchhandlung „Librairie Arthaud“</span></span></p> </td> </tr> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Phase</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Vom Unternehmen als „Serie A“ bezeichnet</span></span></p> </td> </tr> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Hauptsitz</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Grenoble, Frankreich (Lireka SAS; hält 100 % an der Librairie Arthaud SAS)</span></span></p> </td> </tr> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Finanzierungsrunde</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Eigenkapitalrunde über insgesamt 3 Mio. € (2,4 Mio. € Neugeld) bei einer Bewertung von 9 Mio. € vor der Finanzierung; 2,55 € pro Aktie; Eigenkapital über einen Treuhänder von Crowdcube</span></span></p> </td> </tr> </tbody> </table> <h2><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">KI-Bewertung</span></span></h2> <table cellspacing="0" class="Table" style="background:white; border-collapse:collapse; margin-left:-1px; width:6.5in"> <tbody> <tr> <td style="background-color:#faece7; vertical-align:top; width:229px"> <p style="text-align:center"> </p> </td> <td style="background-color:#faece7; vertical-align:top; width:395px"> <p><span style="font-size:11px"><span style="font-family:Aptos,sans-serif"><strong><span style="color:black">Warum dieser Score</span></strong></span></span></p> </td> </tr> <tr> <td style="background-color:#faece7; vertical-align:top; width:229px"> <p style="text-align:center"> </p> </td> <td style="background-color:#faece7; vertical-align:top; width:395px"> <ul> <li><span style="font-size:11px"><span style="font-family:Aptos,sans-serif"><span style="color:black">Echte, durch mehrere Quellen bestätigte Marktentwicklung: ~14,4 Mio. € Konzernumsatz im Jahr 2025, Umsatz der Lireka-Website um ~+41 % auf 5,5 Mio. € gestiegen, 104.643 Kunden insgesamt, Trustpilot-Bewertung 4,8/5 (6.283 Bewertungen) und angegebene CAC von 8 € bei einem ROAS > 5.</span></span></span></li> </ul> </td> </tr> <tr> <td style="background-color:#faece7; vertical-align:top; width:229px"> <p style="text-align:center"><span style="font-size:12pt"><span style="font-family:Aptos,sans-serif"><strong><span style="font-size:28.0pt"><span style="color:black">53 / 100</span></span></strong></span></span></p> </td> <td style="background-color:#faece7; vertical-align:top; width:395px"> <ul> <li><span style="font-size:11px"><span style="font-family:Aptos,sans-serif"><span style="color:black">Erfahrene Gründer – Marc Bordier (11 Jahre bei Amazon als Leiter der Buchkategorie) und Emma Henry (Hachette, Amazon, Samsung) – in einem Bereich, den sie gut kennen.</span></span></span></li> </ul> </td> </tr> <tr> <td style="background-color:#faece7; vertical-align:top; width:229px"> <p style="text-align:center"><span style="font-size:12pt"><span style="font-family:Aptos,sans-serif"><strong><span style="color:black">Fazit: Vorsicht</span></strong></span></span></p> </td> <td style="background-color:#faece7; vertical-align:top; width:395px"> <ul> <li><span style="font-size:11px"><span style="font-family:Aptos,sans-serif"><span style="color:black">Allerdings schreibt das operative Unternehmen auf bilanzieller Ebene nach wie vor Verluste (Nettoergebnis von Lireka SAS −0,40 Mio. € im Jahr 2025), ist mit mehreren Millionen Euro verschuldet, und das Investitionsszenario hängt fast ausschließlich von Prognosen des Managements ab, die laut Angaben der Plattform selbst nicht garantiert sind.</span></span></span></li> </ul> </td> </tr> <tr> <td style="background-color:#faece7; vertical-align:top; width:229px"> <p style="text-align:center"> </p> </td> <td style="background-color:#faece7; vertical-align:top; width:395px"> <ul> <li><span style="font-size:11px"><span style="font-family:Aptos,sans-serif"><span style="color:black">Mehrere ungeklärte Informationslücken: Ein dritter, öffentlich genannter Mitbegründer fehlt in den Unterlagen, die Beteiligungszahlen lassen sich nicht eindeutig in Einklang bringen, die Berechtigung zu Steuererleichterungen wird uneinheitlich angegeben, und seit Januar 2025 ist ein Verfahren vor dem Arbeitsgericht (Prud’hommes) anhängig.</span></span></span></li> </ul> </td> </tr> </tbody> </table> <p> </p> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#e6f1fb; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:672px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">ℹ️ Dies ist keine Anlageberatung.</span></strong><span style="color:black"> </span><span style="color:#000000">Der Zweck dieser Übersicht besteht darin, potenziellen Investoren zu helfen, Crowdfunding-Projekte schnell in die engere Wahl zu nehmen, ohne eine endgültige Anlageentscheidung zu treffen. Vor einer Investition sollte das endgültig ausgewählte Projekt auf der Grundlage der vom Unternehmen auf der jeweiligen Crowdfunding-Plattform bereitgestellten Informationen eingehend geprüft werden. KI kann Fehler machen, daher müssen Sie die Daten noch einmal überprüfen.</span></span></span></p> </td> </tr> </tbody> </table> <h2><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Unternehmensbeschreibung</span></span></h2> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Lireka ist eine Online-Buchhandlung, die auf den Export von Büchern spezialisiert ist. Sie bietet kostenlosen weltweiten Versand, Preise in der jeweiligen Landeswährung sowie die Abwicklung von Zöllen und Abgaben für den Kunden und positioniert sich damit gegen die höheren Exportpreise von Amazon und die separat in Rechnung gestellten Zölle. Das Unternehmen gibt an, über einen Katalog von fast 2 Millionen Titeln zu verfügen, vorwiegend in französischer Sprache; ein englischer Katalog wurde im 2. Quartal 2026 eingeführt, und für 2027 sind Kataloge in Deutsch, Spanisch und Italienisch geplant.</span></span></p> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Das Unternehmen arbeitet mit der „Librairie Arthaud“ zusammen, einer 1801 gegründeten Buchhandlung in Grenoble, die im Oktober 2020 von der Gruppe übernommen wurde und physischen Lagerbestand (rund 80.000 Artikel), Beziehungen zu Verlagen sowie eine Marke für unabhängige Buchhandlungen bereitstellt. Lireka betreibt zudem einen B2B-Bereich (Lireka Pro), der an Alliances Françaises, Instituts Français, französische Schulen und Bibliotheken verkauft; nach Angaben des Unternehmens macht der B2B-Bereich derzeit etwa 10 % des Umsatzes aus, wobei das Management einen Anteil von 20–30 % anstrebt.</span></span></p> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Die Gründer sind Marc Bordier (Präsident/CEO, ca. 11 Jahre bei Amazon als Leiter der Buchkategorie) und Emma Henry (CEO/Geschäftsführerin, mit Erfahrung bei Hachette, Amazon und Samsung). Öffentliche Quellen nennen zudem einen dritten Mitbegründer, Robin Mallein (CTO, mit Sitz in Prag), der jedoch weder in der aktuellen Präsentation noch in der Zusammenfassung der wichtigsten Informationen aufgeführt ist.</span></span></p> <h2><span style="font-family:Times New Roman,serif"><span style="font-size:13.3333px">Mögliche Renditen</span></span></h2> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Unternehmensziel</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Ausbau der bereits bewährten Position als Spezialist für Buchexporte; langfristige Vision von >100 Mio. € Umsatz innerhalb von 8–10 Jahren und Etablierung als europäischer Marktführer im Buchexport (angaben des Unternehmens, gemäß der Präsentation).</span></span></p> </td> </tr> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Zielgrößen</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong>Vom Unternehmen bereitgestellt</strong> – Lireka hat sein eigenes Renditeziel, seinen Exit-Horizont (5–7 Jahre) und seine Exit-Multiplikatoren (EV/Umsatz 0,85x, EV/EBITDA 10x) festgelegt, sodass der informativen Risikohinweis der Plattform von ca. 10x hier nicht zutrifft.</span></span></p> </td> </tr> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Angegebener Exit</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Verkauf an einen strategischen Käufer (Buchvertriebe, spezialisierte E-Commerce-Unternehmen, europäische Medienkonzerne) oder PE-Wachstumsdeal; angestrebter Unternehmenswert beim Exit ~30 Mio. € bei einem prognostizierten Umsatz für 2030 von ~35 Mio. € und einem EBITDA von ~3 Mio. €.</span></span></p> </td> </tr> </tbody> </table> <h2><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Weg zum Ziel (Methodik des Unternehmens)</span></span></h2> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Das Unternehmen stützt sich auf ein eigenes Exit-Framework, anstatt sich auf branchenübliche Heuristiken zu verlassen. Es bewertet einen zukünftigen Exit mit einem Unternehmenswert von rund 30 Mio. €, indem es ein EV/Umsatz-Multiple von 0,85x auf den für 2030 prognostizierten Umsatz von etwa 35 Mio. € anwendet, abgeglichen mit einem EV/EBITDA-Multiple von 10x auf das für 2030 prognostizierte EBITDA von etwa 3 Mio. €. Das Erreichen dieses Umsatzes setzt voraus, dass das Unternehmen von 2026 bis 2030 ein jährliches Website-Wachstum von rund +41 % aufrechterhält und zusätzlich zum bewährten französischen Modell Kataloge in Englisch, Deutsch, Spanisch und Italienisch einführt. Bei einem Pre-Money-Wert von 9 Mio. € impliziert ein Exit-Unternehmenswert von ca. 30 Mio. € ein etwa 3,3-faches auf Unternehmensebene, bevor Verwässerungen, Gebühren oder die Liquidationsrangfolge berücksichtigt werden – was im Großen und Ganzen mit dem im Deck selbst angegebenen „3x“-Wert übereinstimmt.</span></span></p> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Angeführter vergleichbarer Exit</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Die Präsentation veranschaulicht die These anhand der Übernahme der Recommerce-Plattform „World of Books“ durch Livingbridge im Jahr 2021 (eine Private-Equity-Finanzierung eines Buch-E-Commerce-Unternehmens).</span></span></p> </td> </tr> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Meilensteine bis zum Exit</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Ausbau des englischen Katalogs (Ziel: 10 Mio. Titel), Markteinführung in Deutschland, Direktbelieferung neuer Standorte, Verdopplung der Lagerfläche auf ca. 2.000 m² und ein EBITDA von ca. 3 Mio. € bis 2030 (allesamt vom Unternehmen angegebene Prognosen).</span></span></p> </td> </tr> </tbody> </table> <h2><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Bewertung</span></span></h2> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Angebot</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">3 Mio. € Gesamtkapital, davon 2,4 Mio. € Frischkapital; in der Präsentation wird darauf hingewiesen, dass ca. 300.000 € für die Crowdcube-Crowd-Tranche reserviert sind.</span></span></p> </td> </tr> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Pre-Money</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">9.000.000 € (Präsentation) / 8.998.514 € (Börsennotierung). Aktienkurs 2,55 € (≈2,20 £).</span></span></p> </td> </tr> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Impliziter Post-Money-Wert</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Etwa 11,4 Mio. € auf Basis der 2,4 Mio. € Frischkapital (etwa 12 Mio. €, wenn die gesamten 3 Mio. € als bewertetes Eigenkapital behandelt werden). Der genaue Wert hängt vom endgültigen Einziehungsbetrag ab, der noch nicht bekannt gegeben wurde.</span></span></p> </td> </tr> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Methodik</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Nicht offengelegt. Das Unternehmen legt ein Rahmenwerk für das Exit-Multiple im Hinblick auf einen zukünftigen Verkauf vor, erläutert jedoch nicht, wie der Einstiegspreis von 9 Mio. € selbst ermittelt wurde.</span></span></p> </td> </tr> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:168px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Benchmark</span></strong></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:504px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Der Pre-Money-Wert von 9 Mio. € liegt unter dem 1-fachen des konsolidierten Umsatzes von ca. 14,4 Mio. € für 2025 und entspricht etwa dem 1-fachen des Einzelumsatzes von Lireka SAS für 2025 (ca. 9,0 Mio. €). Die unternehmenseigene Exit-Annahme geht von einem niedrigen EV/Umsatz-Multiplikator von 0,85x aus, was widerspiegelt, dass Buchhandel-Unternehmen in der Regel mit moderaten Umsatzmultiplikatoren gehandelt werden.</span></span></p> </td> </tr> </tbody> </table> <h2><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Instrument und Anlegerbedingungen</span></span></h2> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Was Sie besitzen</span></span></h3> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Sie würden Stammaktien erhalten – die standardmäßige, einzige Aktienklasse dieses Unternehmens (es gibt keine separaten „Vorzugsaktien“). Sie würden diese nicht direkt halten: Das rechtliche Eigentum liegt bei Crowdcube Nominees Limited, die die Aktien treuhänderisch in Ihrem Namen hält (dies wird als Nominee-Struktur bezeichnet). Sie sind der „wirtschaftliche Eigentümer“, was bedeutet, dass Sie den wirtschaftlichen Wert erhalten, während der Nominee das rechtliche Eigentumsrecht innehat und die gebündelten Crowd-Aktien in der Regel als einen einzigen Block abstimmt. Jede Stammaktie ist mit einer Stimme verbunden, doch da die Crowd-Anteile über den Nominee gebündelt sind und die Gründer eine große Mehrheit kontrollieren – Marc Bordier allein hält etwa 58 % (die Gründer zusammen laut öffentlichen Quellen rund 69 %) –, haben einzelne Crowdfunding-Investoren praktisch kaum Einfluss auf Unternehmensentscheidungen, einschließlich einer Entscheidung zum Verkauf des Unternehmens.</span></span></p> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Verwässerung und zukünftige Finanzierungsrunden</span></span></h3> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">„Verwässerung“ bedeutet, dass Ihr Eigentumsanteil schrumpft, wenn das Unternehmen bei einer späteren Kapitalbeschaffung neue Aktien ausgibt. Das Unternehmen hat erklärt, dass es voraussichtlich weiteres Kapital beschaffen wird (in den Risikofaktoren heißt es, dass dies notwendig sein wird, wobei es keine Erfolgsgarantie gibt), und es hat sich bereits 0,6 Mio. € an Wandelanleihen von bestehenden Aktionären für das Jahr 2025 gesichert. Crowdfunding-Investoren erhalten hier Vorkaufsrechte (das Recht, in einer zukünftigen Finanzierungsrunde genügend Anteile zu erwerben, um Ihren Anteil zu halten), doch die meisten Kleinanleger nehmen diese Rechte nicht wahr, sodass im Laufe der Zeit eine gewisse Verwässerung realistisch ist. Es gibt keinen preisbasierten Verwässerungsschutz – wenn eine zukünftige Finanzierungsrunde zu einem niedrigeren Preis als die aktuelle durchgeführt wird, ist Ihre Beteiligung nicht geschützt.</span></span></p> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Rechenbeispiel (standardmäßige Mechanismen der Cap-Tabelle, keine Beratung): Wenn Sie heute 1.000 € bei einer Post-Money-Bewertung von etwa 11,4 Mio. € investieren, besitzen Sie etwa 0,0088 % des Unternehmens (ca. 1.000 € ÷ 11,4 Mio. €). Wenn das Unternehmen anschließend 4 Mio. € bei einer Pre-Money-Bewertung von 20 Mio. € einwirbt (eine erfolgreiche Serie-A-Finanzierungsrunde mit höherer Bewertung), entspricht das neue Kapital etwa 17 % des vergrößerten Unternehmens, sodass sich Ihr Anteil auf etwa 0,0073 % verwässert. Ist die nächste Runde hingegen eine Down-Round bei einer Pre-Money-Bewertung von 6 Mio. € mit einer Kapitalbeschaffung von 4 Mio. €, entspricht das neue Kapital etwa 40 % des vergrößerten Unternehmens, Ihr Anteil wird auf etwa 0,0053 % verwässert, und der implizite Wert Ihrer 1.000 € sinkt aufgrund des niedrigeren Aktienkurses um etwa 30–40 %.</span></span></p> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Zu den Mitarbeiteraktienoptionen: Das Unternehmen verfügt über einen BSPCE-Optionspool (das französische Äquivalent zu Mitarbeiteraktienoptionen), und der noch nicht zugeteilte Teil ist bereits in der vollständig verwässerten Aktienanzahl von 3.528.829 berücksichtigt, die zur Preisgestaltung dieser Runde herangezogen wurde, sodass diese spezifische Verwässerung bereits eingepreist ist. Unabhängig davon werden die Wandelanleihen 2025 wahrscheinlich mit einem Abschlag von 20 % in Aktien umgewandelt, da diese Finanzierungsrunde offenbar den „Pre-Money“-Schwellenwert von 6,6 Mio. € überschreitet, der die Wandlung auslöst – wodurch etwa zeitgleich mit Ihrer Investition weitere Aktien hinzukommen. Ihr Bezugsrecht ist das wichtigste Instrument, mit dem Sie Ihren Anteil in zukünftigen Finanzierungsrunden verteidigen können, falls Sie sich entscheiden, weiter zu investieren.</span></span></p> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Exit- und Liquidationsmechanismen</span></span></h3> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Die „Liquidationspräferenz“ legt die Reihenfolge fest, in der die Beteiligten ausgezahlt werden, falls das Unternehmen verkauft oder liquidiert wird. Auch wenn es hier nur eine Aktienklasse gibt, schafft die Gesellschaftervereinbarung eine Auszahlungsrangfolge: Zunächst erhält jeder Gesellschafter den Betrag zurück, den er ursprünglich für seine Anteile gezahlt hat; zweitens fließt der verbleibende Betrag vorrangig an die „neuen Investoren“ (zu denen auch diejenigen gehören, die in dieser Runde investieren), bis diese den von ihnen gezahlten Aufschlag auf den Nennwert ihrer Anteile zurückerhalten haben; und falls der Betrag dafür nicht ausreicht, wird er anteilig unter den neuen Investoren aufgeteilt. Was danach noch übrig bleibt, wird unter allen Aktionären entsprechend ihrer Beteiligungsquote aufgeteilt. Einfach ausgedrückt gewährt dies den Investoren dieser Finanzierungsrunde eine Vorzugsbehandlung bei der Kapitalrückzahlung im Verhältnis von etwa 1:1 – also einen gewissen Schutz vor Verlusten, jedoch keinen Multiplikator.</span></span></p> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">„Drag-along“ ermöglicht es einer Mehrheit, alle anderen zu zwingen, zu denselben Bedingungen zu verkaufen. Hier können Inhaber von mindestens 50 % aller Anteile und mindestens 50 % der von Investoren gehaltenen Anteile alle anderen Anteilseigner zwingen, an einen Käufer zu verkaufen, der 100 % der Anteile erwirbt – allerdings nur, wenn der Preis eine Untergrenze erreicht, die dem Einstiegspreis der neuen Investoren zuzüglich einer jährlichen Verzinsung von 10 % entspricht. „Tag-along“ ist das spiegelbildliche Recht, das Sie schützt: Wenn ein Großaktionär so viele Anteile verkauft, dass ein Käufer eine Kontrolle von mehr als 50 % erhält, können Sie zu denselben Bedingungen am Verkauf teilnehmen; ein proportionales Tag-along-Recht gilt auch für kleinere Verkäufe. Sie können also in einen Verkauf hineingezogen werden, den Sie nicht gewählt haben, jedoch nicht unterhalb einer steigenden Preisuntergrenze, und Sie können mitverkaufen, wenn andere verkaufen.</span></span></p> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Liquidität: Es sind keine Dividenden zu erwarten, es gibt keinen garantierten Sekundärmarkt (Sie können Ihre wirtschaftliche Beteiligung nur an ein anderes Crowdcube-Mitglied übertragen, wobei das rechtliche Eigentumsrecht beim Nominee verbleibt), und es gelten Übertragungsbeschränkungen. Sie sollten diese Anlage langfristig als illiquide betrachten – realistisch gesehen 5–7 Jahre bis zu einem Exit auf Unternehmensebene, laut Präsentationsunterlagen – und Kapitalverluste sind möglich.</span></span></p> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Wesentliche Risiken, die speziell mit diesem Anlageinstrument verbunden sind</span></span></h3> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Die Anteile werden über einen Treuhänder gehalten, und die Gründer verfügen über eine große Mehrheit, sodass Crowdfunding-Investoren praktisch keinen Stimmrechts Einfluss haben – auch nicht darüber, ob und wann das Unternehmen verkauft wird.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Kein preisbasierter Verwässerungsschutz: Bei einer Down-Round sinken der prozentuale Anteil der Crowd und der implizite Wert der Investition ohne Puffer.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Die Liquidationsrangfolge sieht vor, dass zunächst die ursprüngliche Zeichnung jedes Anteilseigners und anschließend die Prämie der neuen Investoren zurückgezahlt wird – bei einem Verkauf zu einem niedrigen Wert bleibt nach Begleichung der Gläubiger (die Gruppe hat Schulden in Höhe von mehreren Millionen Euro) möglicherweise nur wenig übrig, das anteilig ausgeschüttet werden kann.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Ein Mitverkaufsrecht bei der 50 %/50 %-Schwelle bedeutet, dass Gründer und gleichgesinnte Investoren einen Verkauf ohne Zustimmung der Crowd erzwingen können (allerdings nur oberhalb einer Untergrenze von Einstiegspreis + 10 % pro Jahr).</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Die von bestehenden Aktionären gehaltenen Wandelanleihen mit Fälligkeit 2025 werden im Rahmen dieser Finanzierungsrunde wahrscheinlich mit einem Abschlag von 20 % gewandelt, und das Unternehmen rechnet mit einer weiteren Kapitalbeschaffung – beides führt zu einer Erhöhung der Aktienanzahl vor oder parallel zur Crowd.</span></span></li> </ul> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Nicht offengelegte Punkte</span></span></h3> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Die folgenden Punkte wurden in den geprüften Unterlagen nicht offengelegt. Wenn eine Bedingung nicht offengelegt wird, können Sie diese vor einer Investition nicht beurteilen:</span></span></p> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Die vollständige Cap-Tabelle vor der Finanzierungsrunde – nur Marc Bordiers Beteiligung von >25 % ist aufgeführt; frühere Angel-Investoren, der genaue Prozentsatz des Optionspools und der Streubesitz werden nicht separat ausgewiesen.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Ein festgelegtes Enddatum der Sperrfrist für Investoren bzw. eine Haltefrist (es bestehen Übertragungsbeschränkungen, jedoch wird kein explizites Enddatum angegeben).</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Die Methodik hinter der Einstiegsbewertung von 9 Mio. €.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Der endgültige Kapitalbeschaffungsbetrag und damit die genaue Post-Money-Bewertung sowie die endgültige Verwässerung (die Kapitalbeschaffung läuft noch).</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Die vollständige Satzung (auf die in der E-Mail zur Bedenkzeit verwiesen wird, die jedoch nicht bereitgestellt wurde) sowie die bezifferte Höhe der anhängigen Arbeitsrechtsklage.</span></span></li> </ul> <h2><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Aufschlüsselung der Punktzahl</span></span></h2> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:213px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Kategorie</span></strong></span></span></p> </td> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Punktzahl</span></strong></span></span></p> </td> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Gewichtung</span></strong></span></span></p> </td> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:312px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Urteil</span></strong></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:213px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Erfolgsbilanz des Teams und des Gründers</span></span></p> </td> <td style="background-color:#faeeda; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><span style="color:black">78</span></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">15 %</span></span></p> </td> <td style="background-color:#faeeda; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:312px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Mäßig bis stark</span></strong><span style="color:black"> – Fundierte Amazon-/Verlags-Erfahrung in genau diesem Bereich; ausgeglichen durch einen nicht genannten dritten Mitbegründer und spärliche öffentliche Informationen über das übrige Team.</span></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:213px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Traktion und Unit Economics</span></span></p> </td> <td style="background-color:#faeeda; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><span style="color:black">72</span></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">30 %</span></span></p> </td> <td style="background-color:#faeeda; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:312px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Mäßig</span></strong><span style="color:black"> — Echte Umsätze, ~+41 % Website-Wachstum, über 100.000 Kunden und ROAS > 5; die Rentabilität beschränkt sich jedoch auf ein geringes EBITDA, und das Geschäftsmodell stützt sich auf Prognosen.</span></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:213px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Marktgröße & Wachstum</span></span></p> </td> <td style="background-color:#faeeda; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><span style="color:black">60</span></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">15 %</span></span></p> </td> <td style="background-color:#faeeda; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:312px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Mäßig</span></strong><span style="color:black"> – Große angegebene Exportmärkte nach Sprache, doch die Zahlen stammen vom Unternehmen selbst und wurden in den Unterlagen nicht unabhängig überprüft.</span></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:213px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Wettbewerb & Wettbewerbsvorteil</span></span></p> </td> <td style="background-color:#faece7; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><span style="color:black">55</span></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">10 %</span></span></p> </td> <td style="background-color:#faece7; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:312px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Vorsicht</span></strong><span style="color:black"> – Ausgehandelte Logistik, standortbezogene Preisgestaltung und SEO sind plausible Vorteile, doch Amazon ist der direkte Wettbewerber, und die Kernplattform wurde von einer externen Agentur entwickelt.</span></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:213px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Geschäftsmodell & Skalierbarkeit</span></span></p> </td> <td style="background-color:#faeeda; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><span style="color:black">65</span></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">10 %</span></span></p> </td> <td style="background-color:#faeeda; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:312px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Mäßig</span></strong><span style="color:black"> – Ein wirklich wiederholbares, mehrsprachiges Konzept auf einer gemeinsamen Grundlage; außerhalb des französischen Marktes noch nicht erprobt, da die englische Version erst 2026 eingeführt wird.</span></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:213px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Finanzielle Solidität & Bilanz</span></span></p> </td> <td style="background-color:#faece7; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><span style="color:black">48</span></span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:73px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">20 %</span></span></p> </td> <td style="background-color:#faece7; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:312px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Vorsicht</span></strong><span style="color:black"> – Lireka SAS verzeichnete bis einschließlich 2025 jedes Jahr Nettoverluste (−0,40 Mio. €), ist mit mehreren Millionen Euro verschuldet und muss ausdrücklich weiteres Kapital beschaffen.</span></span></span></p> </td> </tr> </tbody> </table> <h2><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Detaillierte Bewertung</span></span></h2> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Team und Erfolgsbilanz des Gründers (78 / 100)</span></span></h3> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Stärken</span></strong></span></span></p> </td> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Schwächen</span></strong></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Marc Bordier war rund 11 Jahre lang bei Amazon als Leiter der Buchkategorie in Paris und London tätig – direkt relevante Erfahrung in der Kategorie und im operativen Geschäft.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Emma Henry bringt Erfahrungen bei Hachette (Verlagswesen), Amazon und Samsung sowie aus einem früheren US-Start-up (Matelab) mit.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Das Team hat das Unternehmen auf einen Umsatz von ca. 14 Mio. € und ein positives Konzern-EBITDA geführt, was die Umsetzungsstärke belegt.</span></span></li> </ul> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Ein dritter Mitbegründer, der in öffentlichen Quellen genannt wird (Robin Mallein, CTO), fehlt ohne Erklärung in der Präsentation und im SKI – eine offene Frage zur Teamzusammensetzung.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Die Angaben zur Beteiligungsstruktur stimmen nicht über alle Quellen hinweg überein (SKI: 57,93 % für Bordier; Präsentation: 61 % + 8 %; Website: insgesamt 69 %).</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Es gibt nur begrenzte unabhängige Belege für die Tiefe des insgesamt 14-köpfigen Teams über die beiden namentlich genannten Gründer hinaus.</span></span></li> </ul> </td> </tr> </tbody> </table> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Traktion & Unit Economics (72 / 100)</span></span></h3> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Stärken</span></strong></span></span></p> </td> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Schwächen</span></strong></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Der konsolidierte Umsatz stieg im Jahr 2025 auf ca. 14,4 Mio. €; der Umsatz der Lireka-Website stieg um ca. +41 % auf 5,5 Mio. €.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">104.643 Kunden insgesamt (vom Unternehmen angegebene durchschnittliche jährliche Wachstumsrate (CAGR) von +124 % für den Zeitraum 2021–2025); Trustpilot-Bewertung von 4,8/5 bei 6.283 Bewertungen.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Die vom Unternehmen angegebenen Akquisitionskosten von 8 € CAC bei einem ROAS > 5 deuten – sofern zutreffend – auf effizientes bezahlte Marketing hin.</span></span></li> </ul> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Die Rentabilität beschränkt sich auf ein geringes EBITDA (+11.000 € allein bei Lireka laut Präsentation; ca. 44.000 € konzernweit laut Pressemitteilung), nicht auf den Nettogewinn.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Die Kunden- und NPS-Kennzahlen (NPS 82) stammen aus Unternehmensangaben und wurden im Dossier nicht unabhängig geprüft.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Das Zukunftsszenario setzt auf ein anhaltendes Wachstum von +41 %, während das EBITDA 2027 voraussichtlich wieder in den negativen Bereich rutschen wird.</span></span></li> </ul> </td> </tr> </tbody> </table> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Marktgröße und Wachstum (60 / 100)</span></span></h3> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Stärken</span></strong></span></span></p> </td> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Schwächen</span></strong></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Das Unternehmen verweist auf beträchtliche Exportmärkte nach Sprachen (Englisch: 5,4 Mrd. €; Französisch und Deutsch: jeweils 0,7 Mrd. €), was die These einer mehrsprachigen Expansion stützt.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Eine klare Definition der großen Zielgruppe: ca. 300 Mio. Französischsprachige und ca. 2–2,5 Mio. im Ausland lebende Franzosen.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Als Grundlage für die Marktgrößenangaben werden mehrere externe Datenquellen genannt.</span></span></li> </ul> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Die Angaben zur Marktgröße stammen vom Unternehmen selbst und wurden in den Unterlagen nicht unabhängig überprüft.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Das französische Exportsegment, das das Unternehmen tatsächlich nachgewiesen hat, ist der kleinste der genannten Märkte (~0,7 Mrd. €).</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Begrenzte unabhängige Validierung der Wachstumsraten in den angestrebten Exportnischen.</span></span></li> </ul> </td> </tr> </tbody> </table> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Wettbewerb & Wettbewerbsvorteil (55 / 100)</span></span></h3> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Stärken</span></strong></span></span></p> </td> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Schwächen</span></strong></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Differenzierte Positionierung als Exportspezialist (kostenlose Lieferung, inklusive Zölle, lokalisierte Preisgestaltung) im Gegensatz zu Amazons höheren Exportpreisen und separat in Rechnung gestellten Zöllen.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Angegebene Vorteile: ausgehandelte Speditionspreise, standortbezogene Preisgestaltung, SEO-Präsenz sowie Arthauds Beziehungen zu Verlagen und physischer Lagerbestand.</span></span></li> </ul> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Amazon ist der direkte Wettbewerber mit weitaus größerer Reichweite und mehr Ressourcen.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Die Kernplattform wurde von einer externen Agentur (COex) über einen Zeitraum von etwa zwei Jahren entwickelt, was die Darstellung als „proprietäre Technologie / vollständiges geistiges Eigentum“ relativiert.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Aggregatoren listen ca. 18 Wettbewerber auf; die Nachhaltigkeit des Logistik- und Preisvorteils ist nicht unabhängig validiert.</span></span></li> </ul> </td> </tr> </tbody> </table> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Geschäftsmodell & Skalierbarkeit (65 / 100)</span></span></h3> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Stärken</span></strong></span></span></p> </td> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Schwächen</span></strong></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Ein wirklich skalierbares Modell: eine gemeinsame Grundlage für Logistik, Technologie, Katalog und Akquise, die sprachweise angewendet wird.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Ein zusätzlicher B2B-Kanal (Lireka Pro) mit einem glaubwürdigen institutionellen Kundenstamm (Alliances Françaises, Schulen, Bibliotheken).</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Im Vergleich zum lagerintensiven Einzelhandel „asset-light“, wobei die physische Buchhandlung den Bestand und die Marke bereitstellt.</span></span></li> </ul> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Die Mehrsprachigkeit ist noch nicht bewiesen – Englisch wurde erst im 2. Quartal 2026 eingeführt, und Deutsch, Spanisch und Italienisch sind noch in Planung.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Der kostenlose weltweite Versand hängt von anhaltend günstigen Transportkosten und hohen Warenkorbwerten ab.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Eine Skalierung erfordert eine Verdopplung der Lagerkapazitäten und weiteres Kapital, was mit zusätzlichen Umsetzungs- und Finanzierungsrisiken verbunden ist.</span></span></li> </ul> </td> </tr> </tbody> </table> <h3><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Finanzielle Solidität & Bilanz (48 / 100)</span></span></h3> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Stärken</span></strong></span></span></p> </td> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:336px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Schwächen</span></strong></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Das EBITDA des Konzerns wurde 2025 leicht positiv, und die Librairie Arthaud befindet sich bei bescheidenem Wachstum nahe der Gewinnschwelle.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Die Verluste der operativen Gesellschaft haben sich von Jahr zu Jahr verringert (von −1,17 Mio. € im Jahr 2022 auf −0,40 Mio. € im Jahr 2025).</span></span></li> </ul> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:336px"> <ul> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Lireka SAS verzeichnete bis einschließlich 2025 weiterhin jedes Jahr einen Nettoverlust (−0,40 Mio. €), sodass das Unternehmen noch nicht netto profitabel ist.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Die Gruppe hat Bankverbindlichkeiten in Höhe von mehreren Millionen Euro (BPI, Banque Populaire, BNP, CIC) mit Laufzeiten bis 2032.</span></span></li> <li><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Im SKI wird darauf hingewiesen, dass das Unternehmen weiteres Kapital beschaffen muss, wobei kein Erfolg garantiert ist – das Finanzierungsrisiko wird ausdrücklich erwähnt.</span></span></li> </ul> </td> </tr> </tbody> </table> <h2><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Warnsignale und Integritätsprüfungen</span></span></h2> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:200px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Prüfen</span></strong></span></span></p> </td> <td style="background-color:#f4f2ec; border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:472px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong><span style="color:black">Befund</span></strong></span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:200px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Anhängige Rechtsstreitigkeiten</span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:472px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong>Vorhanden</strong> – Seit Januar 2025 ist ein Verfahren vor dem Arbeitsgericht (Prud’hommes) anhängig. Die Höhe des Streitwerts ist in den Unterlagen nicht beziffert.</span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:200px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Konsistenz bei Team/Gründern</span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:472px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong>Unstimmigkeit</strong> – Ein dritter Mitbegründer, der in öffentlichen Quellen genannt wird (Robin Mallein, CTO), taucht weder in der Präsentation noch im SKI auf, und der Grund dafür wird nicht erläutert.</span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:200px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Abstimmung der Beteiligungsverhältnisse</span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:472px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong>Unstimmigkeit</strong> – Die Beteiligungsverhältnisse der Gründer werden in den verschiedenen Quellen unterschiedlich angegeben (SKI: 57,93 % für Bordier; Präsentation: 61 % + 8 %; Website: insgesamt 69 %). Wahrscheinlich liegen unterschiedliche Berechnungsgrundlagen vor, die in den Unterlagen jedoch nicht abgeglichen wurden.</span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:200px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Bewertungsmethodik</span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:472px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong>Fehlende entscheidende Daten</strong> – Die unabhängige Grundlage für die Einstiegsbewertung von 9 Mio. € wird nicht angegeben; es wird lediglich das Rahmenwerk für das zukünftige Exit-Multiple dargestellt.</span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:200px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Darstellung der Rentabilität</span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:472px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong>Vorsicht</strong> – Die Überschrift „rentables Geschäftsmodell“ stützt sich auf ein geringes EBITDA; die operative Gesellschaft (Lireka SAS) wies im Jahr 2025 weiterhin einen Nettoverlust von −0,40 Mio. € aus.</span></span></p> </td> </tr> <tr> <td style="border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:200px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Konsistenz der Steuervergünstigungen</span></span></p> </td> <td style="border-bottom:1px solid #cccccc; border-left:none; border-right:1px solid #cccccc; border-top:none; vertical-align:top; width:472px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><strong>Unstimmigkeit</strong> — In der britischen Zusammenfassung der wichtigsten Informationen heißt es „EIS: Nein“, während in der französischen Börsennotiz „IR-PME 18 %“ angegeben ist. Die Anspruchsberechtigung variiert je nach Investor und wird nicht in Einklang gebracht.</span></span></p> </td> </tr> </tbody> </table> <h2><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Anmerkungen zur Datenqualität</span></span></h2> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif">Die Finanzdaten und die Geschäftsentwicklung wurden anhand des Pitch-Decks, der „Summary of Key Information“ auf Crowdcube und öffentlicher Presseberichte gegenseitig abgeglichen und sind in sich konsistent – daher ist das Vertrauen in die dargestellten Fakten relativ hoch. Die Anlegerbedingungen sind in der „Summary of Key Information“ gut dokumentiert. Die wichtigsten Lücken betreffen die vollständige Kapitaltabelle, den Status des dritten Mitgründers, die Methodik zur Ermittlung der Einstiegsbewertung, die bezifferte Höhe des anhängigen Rechtsstreits und den endgültigen Kapitalbetrag (die Finanzierungsrunde läuft noch). Die Marktgröße sowie einige Kunden- und NPS-Zahlen stammen aus Unternehmensangaben und wurden nicht unabhängig überprüft, weshalb die Kategorien „Markt“ und „Wettbewerb“ vorsichtiger bewertet wurden.</span></span></p> <table cellspacing="0" class="Table" style="border-collapse:collapse; border:none; width:7.0in"> <tbody> <tr> <td style="background-color:#e6f1fb; border-bottom:1px solid #cccccc; border-left:1px solid #cccccc; border-right:1px solid #cccccc; border-top:1px solid #cccccc; vertical-align:top; width:672px"> <p><span style="font-size:10pt"><span style="font-family:"Times New Roman",serif"><span style="color:black">Dieses Memo wurde von einer KI auf der Grundlage öffentlich zugänglicher Informationen und von der Plattform offengelegter Unternehmensunterlagen erstellt. Investoren müssen ihre eigene Due-Diligence-Prüfung durchführen. Frühere Finanzierungsrunden oder operative Ergebnisse sind keine Garantie für zukünftige Ergebnisse. Crowdfunding-Investitionen sind illiquide, mit hohem Risiko verbunden und es besteht die Möglichkeit eines Kapitalverlusts.</span></span></span></p> </td> </tr> </tbody> </table> <p> </p>

See full overview

Ask question

Ask AI about this project

Beta

Beginnen Sie ein Gespräch

Senden Sie eine Nachricht, um mit dem KI-Assistenten zu chatten

Like this project?

Platform offering this project

Crowdcube GB

Risk Level

Hoch

Return Level

Hoch

Risk Return Level

Good

Mindestinvestition

GBP 10

Finanziert

GBP 1357,04M