AI project overview

Condensed summary based on project data

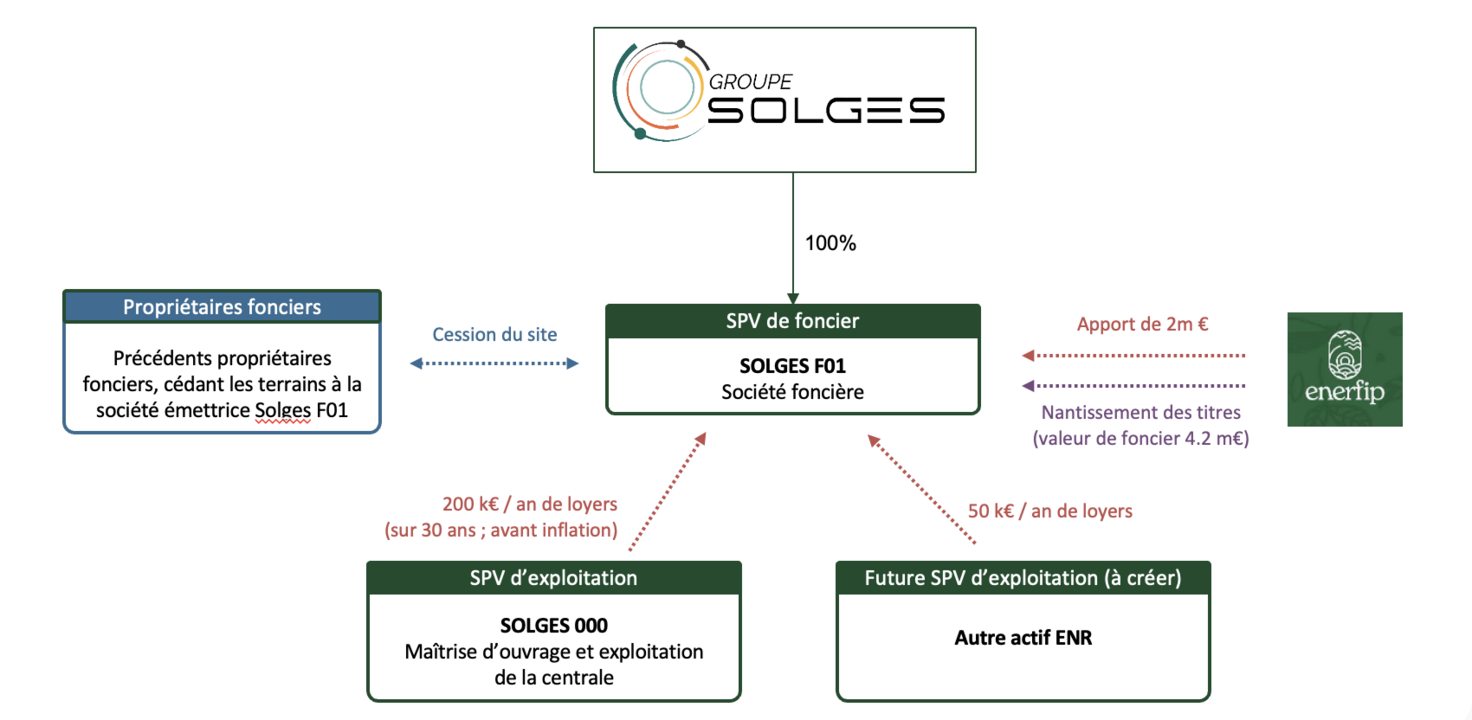

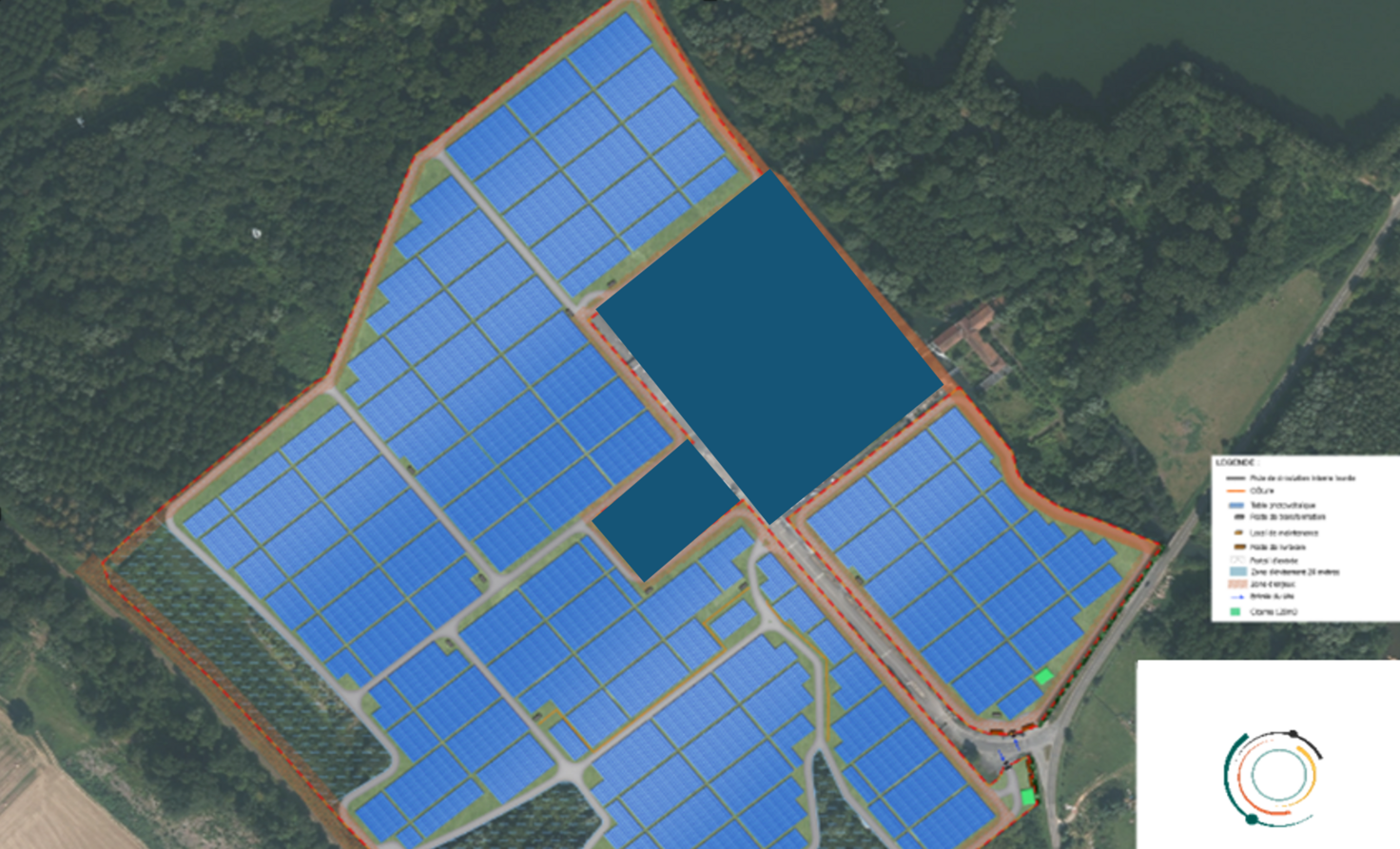

<p>## 0️⃣ Executive Summary Nova Friche is a **34.5 MWc ground-mounted solar PV project** on a **28.5-hectare industrial brownfield site in Oise, France**, with the current fundraising aimed at **acquiring the land through Solges F01**, not yet financing the full plant construction. The future land company is expected to receive **long-term lease income** from the operating/project SPV, while the underlying solar plant business model is still **partly unresolved on the revenue side**, with several options under consideration including CPPA, auction/FiT-style support, or merchant/market sales; the platform model nevertheless assumes **€85/MWh over 20 years** for the PV plant business plan. Investors in this issuance are offered **7.5% annual interest**, bullet repayment after **2 years**, with a possible **1-year extension at +1%**, and benefit from a **first-ranking pledge over 100% of the shares of Solges F01**, whose reported land value is **€4.2m** versus a raise of about **€2.0m**. The investment case is supported by an **advanced development stage**: land acquisition is in progress, environmental studies were completed in 2024, demolition permit obtained, construction permit obtained and reportedly cleared of appeal, and grid connection was requested/obtained depending on source wording. However, key risks remain around **land transaction completion, environmental remediation constraints, final grid/process execution, and especially refinancing/take-out risk**, because Enerfip investors are to be repaid through later project refinancing or asset sale rather than operating cash flow during the 2-year bond term. Overall, this looks like a **credible but development-stage land-finance transaction**, better protected than many unsecured development bonds thanks to tangible collateral and low implied LTV. Still, because important information is missing on the **final offtake contract, EPC package, detailed yield report, debt sizing, and liquidation mechanics**, the project is best classified as **viable but requiring further due diligence**. --- ## 1️⃣ ⚠️ Key Risks – Strong Asset Backing but Development and Refinance Dependence This transaction finances the **purchase of land for a brownfield solar development**, not an already-operating plant. The sponsor is **Groupe Solges Energy**, and the issuer is **Solges F01**, a dedicated land SPV. Solges F01 is expected to own the site and lease it under a **30-year emphyteutic lease** to a project company for the development and operation of the PV plant. The underlying asset is a **34.5 MWc solar project** on a **28.5 ha** site, with an indicated land purchase price of **€1.8–2.0m** and a reported land value of **€4.2m**. ### Main risk categories - **Development / transaction risk:** land acquisition must close successfully; the platform notes the transaction was authorized by the Beauvais commercial court in the context of the seller’s liquidation. - **Construction and permitting risk:** though key permits are in place, the project is still pre-construction and must pass through demolition, site rehabilitation, final procurement and construction. - **Environmental risk:** the site is a historically polluted chemical brownfield with usage constraints and required rehabilitation conditions. - **Revenue risk:** the underlying PV revenue model is **not fully fixed**; several remuneration options were still being considered. - **Refinancing risk:** repayment of the 2-year notes depends on subsequent bank financing or project sale rather than near-term operating cash generation. ### Key mitigants - Experienced sponsor with a long PV track record; the analysis cites **1,500+ PV projects** and **300+ MWc** managed, plus experience in financing structuring. - Advanced development stage: environmental studies completed, demolition permit obtained, construction permit obtained, lease structure in place or intended to be transferred. - Strong collateral on paper: share pledge over issuer holding land valued at **€4.2m**. ### Critical missing data - No signed **PPA / tariff award / offtake contract** provided. - No detailed **independent energy yield assessment** or explicit P50/P90 table beyond P90. - No disclosed **EPC contractor**, module/inverter suppliers, or turnkey contract terms. - No detailed **senior debt term sheet**, refinancing commitment, or bank LOI. - No explicit **land appraisal report methodology** or forced-sale valuation. - No detailed **DSCR table**, only a single average DSCR reference for senior debt. **Data completeness:** moderate at best. Enough exists to understand the structure, but not enough to fully verify production, refinancing, and liquidation risk. --- ## 2️⃣ 💰 Cash Flow Stability – Land Lease Visible, Take-Out Depends on Refinancing At issuer level, Solges F01’s revenue is expected to come primarily from **land lease payments** from the solar SPV. The structure chart indicates **€200k/year of lease income over 30 years** from the main PV SPV, plus **€50k/year** from another future renewable asset/SPV, although the secondary income stream appears less mature and should not be relied upon heavily. At the underlying project level, the platform’s business plan assumes: - **34.5 MWc** - **P90 yield of 997 kWh/kWc** - **P90 generation of 34.4 GWh/year** - **€85/MWh power price over 20 years** - **CAPEX of €27.471m** - **Project IRR of 6.26% over 30 years** - **average senior DSCR of 1.25x** ### Debt service view For the Enerfip notes, the key issue is not project operating DSCR today, but whether the land SPV can **refinance or be taken out within 2 years**. | Scenario | Indicative view | |---|---| | **Optimistic** | Permit and grid milestones convert smoothly, project reaches ready-to-build / financing stage, bank debt or asset sale repays notes on time. | | **Base case** | Project remains financeable, but timing risk leads to tight repayment at maturity; extension option may be needed. | | **Pessimistic** | Delay in construction readiness, unresolved offtake, or brownfield remediation complexity impairs refinancing and delays repayment. | ### Cash flow assessment - **Issuer cash flow during note tenor:** weak for repayment by operations alone. €200k annual land rent does not cover full repayment of a ~€2m bullet note plus coupon at maturity. - **Repayment mechanism:** mostly **capital event/refinancing dependent**, not amortizing from stable current cash flow. - **Conclusion:** this is **not a classic cash-flow lending case**; it is closer to **bridge/development financing secured by land and project de-risking progress**. **Default-risk rating:** **Moderate to High** for the note if judged solely on self-liquidating cash flow, moderated by collateral and project maturity. Due to missing refinancing commitments, the risk cannot be fully verified. --- ## 3️⃣ 🏦 Collateral Strength – Good Asset Coverage, but Forced-Sale Value Unclear Collateral consists of a **first-ranking pledge over 100% of the shares of Solges F01**, the SPV that will own the land. The platform analysis explicitly notes the pledged asset value as **€4.2m** against a raise of **€2.0m**, implying a headline **LTV of about 48%**. ### Security package - **First-ranking share pledge** over Solges F01. - Dedicated use of proceeds for land acquisition; release of funds is tied to acquisition formalities and security documentation. - The KIID/terms also reference security documentation and legal formalities before funds are released. ### Strengths and caveats Strength: - Tangible asset backing is materially better than unsecured development loans. - Low headline LTV offers a buffer. Caveats: - The **€4.2m value** may reflect strategic/project-enhanced value, not necessarily **forced-sale liquidation value**. - Brownfield land can be harder to liquidate due to **pollution, use restrictions, remediation obligations, and specialized buyer pool**. - Investors have a **share pledge**, not necessarily a direct first mortgage over land receivables or a full cash collateral package, based on documents reviewed. ### Estimated LGD Assuming ~€2.0m principal: - **Base-case LGD:** **20–35%**, if land value proves reasonably realizable and enforcement is orderly. - **Stressed LGD:** **35–55%**, if brownfield stigma, legal process, or delayed resale depresses realizable value. Because no formal valuation report or liquidation appraisal is provided, **collateral recovery cannot be fully verified**. --- ## 4️⃣ ⚙️ Technical Risk – Project Advanced, but EPC Data Missing The project benefits from a relatively advanced development profile. The platform analysis indicates: - environmental studies completed in 2024, - demolition permit obtained, - construction permit obtained on 8 March 2024 and reportedly cleared, - grid connection process underway / obtained depending on document wording, - estimated commissioning by **end-2027**, - a 12-month construction schedule from site prep through commissioning. ### Missing technical detail No documentation found on: - EPC contractor identity, - contract type (turnkey EPC vs multi-lot), - panel/inverter suppliers, - warranties / performance guarantees, - performance bonds, - delay liquidated damages, - construction all-risk insurance details, - O&M contract terms. That is a meaningful gap. For a 34.5 MWc project on a brownfield requiring demolition and environmental constraints management, contractor quality and risk allocation matter a lot. **Construction risk rating:** **Moderate**. It would be lower if EPC, grid, and remediation packages were fully documented. --- ## 5️⃣ 🌤️ Production Forecast – Reasonable P90, but No Full Yield Study Provided The platform analysis provides a **P90 yield of 997 kWh/kWc** and **P90 production of 34.4 GWh/year** for the 34.5 MWc plant. That is broadly plausible for northern France and is consistent with a conservative production case. However, several important pieces are missing: - no **P50** production estimate, - no independent **Energy Yield Assessment**, - no resource consultant name, - no assumptions for degradation, availability, curtailment, soiling, or clipping, - no sensitivity tables linking production downside to DSCR. ### Production risk factors - Potential underperformance from site layout constraints and brownfield limitations. - Possible curtailment or grid-related outages. - Long-term weather variability. - Construction on a constrained industrial site may also reduce layout optimization. **Production risk rating:** **Moderate**. The disclosed P90 helps, but without an independent yield report, **resource risk cannot be fully verified**. --- ## 6️⃣ 🤝 Offtaker & Counterparty Risk – Major Uncertainty on Final Power Sales This is one of the weakest-documented areas. The analysis states that remuneration is **still under consideration**, with options including: - **internal CPPA**, - **auction / EDF-type support (AO cat. 3)**, - **free market / merchant sales**. At the same time, the financial model assumes **€85/MWh over 20 years**. That assumption may be reasonable for modeling, but it is **not the same thing as a contracted revenue stream**. ### My view vs. platform I agree with the platform that the project is advanced. I am **more cautious** than the platform on revenue certainty, because: - no signed PPA or tariff award is shown, - no offtaker credit information is disclosed, - no contract tenor/termination details are available. **Offtaker/default risk rating:** **Moderate to High**, because the final buyer and contract structure are not yet fixed. Due to missing offtake documentation, this risk cannot be fully verified. --- ## 7️⃣ 🏛️ Market & Regulatory Environment – France Supportive, but Revenue Route Still Open France remains a generally supportive market for renewable energy, with established permitting, grid, and auction frameworks. That is a positive backdrop. The project also appears to have moved through a substantial portion of the local authorization process. Still, the project faces: - potential changes in support mechanisms or auction outcomes, - merchant price volatility if no fixed-price offtake is secured, - brownfield-specific permitting and environmental compliance obligations, - grid timing risk despite advanced status. **Market/regulatory risk rating:** **Moderate**. Country risk is low-to-moderate, but project-specific commercialization risk remains meaningful. --- ## 8️⃣ 🌱 ESG Impact – Strong Brownfield Redevelopment Story, Some Remediation Sensitivity The ESG case is compelling. The project reuses an **already industrialized and polluted site** rather than greenfield agricultural land, which is generally positive from a land-use perspective. The site historically hosted chemical activities, and rehabilitation must meet environmental requirements set by the sellers/regulators. Environmental positives: - clean power generation from a contaminated former industrial site, - productive reuse of degraded land, - estimated production of **34.4 GWh/year**, enough to support significant local decarbonization. Environmental concerns: - sensitive zones on/around the site are mentioned, - remediation and construction constraints may increase cost/complexity. No explicit EU Taxonomy alignment statement, no quantified CO₂ savings, and no full environmental/social report were provided in the materials reviewed. **ESG assessment is positive overall, but not fully documented.** --- ## 9️⃣ 📊 Risk-Adjusted Return – Attractive Coupon, but This Is a Bridge-to-Refinancing Story The investor return of **7.5% fixed annual interest** for a **2-year senior bond**, with **+1% if extended**, is attractive relative to plain-vanilla operating solar debt. That premium makes sense because this is **development/land bridge financing**, not construction-complete project debt. ### Strengths - Tangible asset-backed structure. - Advanced project development. - Experienced renewable-energy sponsor. - Headline collateral coverage appears strong. ### Weaknesses - Repayment depends on refinancing or sale, not operating amortization. - Final offtake model is unresolved. - EPC and technical package are undisclosed. - Brownfield remediation/legal complexity may affect exit timing. **Overall attractiveness:** **Viable but requires due diligence.** I broadly agree with the platform’s positive-but-not-investment-grade posture reflected in its **B+ project rating**, though I would emphasize more strongly that unresolved offtake and refinancing visibility are the core gating factors. --- ## 🔟 🔍 Overall Risk Rating – Moderate (PD ~10–15%, LGD ~25–45%) ### Estimated credit view - **Probability of Default (PD):** **10–15%** - **Loss Given Default (LGD):** **25–45%** These are judgment-based estimates from the disclosed structure, not model outputs. PD is elevated because the note is effectively dependent on a future financing event. LGD is moderated by the pledged land-holding SPV and headline low LTV, but uncertain because forced-sale value is unproven. ### Key mitigating factors - 1st-ranking pledge over Solges F01 shares. - Land value reported at **€4.2m** vs ~€2m raise. - Advanced development stage and permits largely in hand. - Experienced sponsor with renewable-energy track record. ### Critical missing data - Signed PPA / tariff award / route-to-market contract - Independent yield report with P50/P90 and sensitivities - EPC contract and contractor details - Detailed senior financing / refinancing term sheet - Formal land valuation and liquidation assumptions - Full environmental remediation budget and liabilities allocation ### Final comment **Project appears credible and better protected than many development-stage renewable financings due to tangible land collateral and low implied leverage. However, because repayment depends heavily on successful project de-risking and refinancing, and because key offtake/technical documents are missing, the investment should be viewed as a moderately risky bridge financing rather than stable operating-asset debt.**</p>