Chasing the highest advertised return on a crowdfunding platform is one of the most common and costly mistakes European investors make. A headline rate of 14% sounds exciting, but once you factor in platform fees, default losses, tax treatment, and a five-year lock-up period, that figure can look very different indeed. Real crowdfunding ROI is a richer, more nuanced story than any marketing brochure will tell you. This guide cuts through the noise, explaining exactly how returns are measured, what drives them up or down, and how experienced investors across Europe are building genuinely competitive, resilient portfolios today. 🚀

Key Takeaways

| Point | Details |

|---|---|

| Net ROI matters most | Smart investors consider returns after fees, defaults, and time, not just the highest headline rates. |

| Diversification smooths risk | Spreading investments across 10–30 deals or multiple asset types reduces the impact of losses. |

| Asset type shapes returns | Real estate, startups, and loans offer differing ROI and liquidity, requiring tailored strategies. |

| Patience required | Many crowdfunding investments need 3–7 years to fully realise projected returns. |

| Disciplined approach wins | Consistent, systematic investing and managing expectations is key to long-term wealth building. |

Understanding crowdfunding ROI: The basics

Before diving into how to maximise returns, it is essential to grasp how crowdfunding ROI is actually measured and why it differs from traditional assets.

In a standard savings account or bond, ROI is straightforward: your interest rate, minus inflation. Crowdfunding ROI is far more layered. It reflects the percentage return you actually receive after accounting for every cost, risk, and time factor involved in the deal. That means platform service fees, any arrangement or exit fees, expected loan defaults, and the opportunity cost of having your capital illiquid for years. Understanding crowdinvesting basics is the essential first step before committing capital to any platform.

Key elements that make crowdfunding ROI unique include:

-

Platform fees: Service charges, transaction fees, or annual management fees that directly reduce net returns, often ranging from 0% to 3% depending on asset class.

-

Default rates: In debt-based crowdfunding, some borrowers will fail to repay. A platform advertising 10% gross yield may deliver only 7% net after a 3% loss rate.

-

Illiquidity premium: Because you cannot easily sell your position before maturity, crowdfunding typically needs to reward you with higher returns than liquid assets. However, this illiquidity is also a genuine risk.

-

IRR vs. simple ROI: Internal Rate of Return (IRR) accounts for the timing of cash flows, making it a superior metric for longer-duration deals. Always ask platforms for net-of-fee IRR figures, not gross yields.

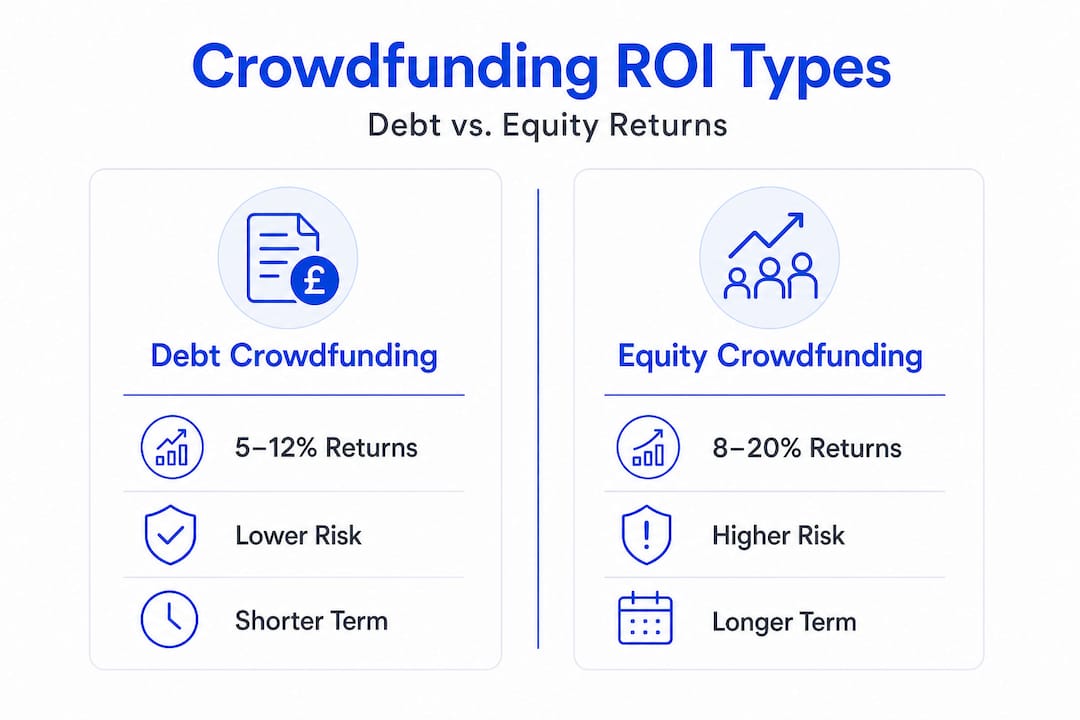

To put real numbers on this, real estate crowdfunding returns show debt deals target 5–12% annual returns, with equity deals targeting 12–18% IRR over 3–7 years, and diversified portfolios netting 8–12% after fees. These ranges are a useful benchmark, but they are starting points, not guarantees. The real estate investment process in Europe involves additional variables that shift these figures considerably for each individual investor.

What affects your actual returns? Beyond headline rates

With a foundational understanding of ROI, the next step is to see why real-world returns often differ from those in marketing brochures.

Several forces work against the headline rate every day your money is invested. Fees are the most obvious, but defaults and taxes are equally destructive to net returns if not managed proactively. One experienced investor achieved 12% net annual return over five years across EU platforms by absorbing 3–5% default rates through disciplined diversification. That result is achievable, but it took deliberate strategy, not luck.

Here is a practical comparison of how costs erode returns across different crowdfunding types:

| Asset class | Gross target yield | Typical fees | Estimated defaults | Net realistic return |

|---|---|---|---|---|

| Real estate debt | 7–12% | 0–2% | 0.5–2% | 5–9% |

| Real estate equity | 12–18% IRR | 0.5–3% | 1–3% | 8–14% IRR |

| Business loans (crowdlending) | 8–14% | 0.5–2% | 3–5% | 5–10% |

| Startup equity | 20–50%+ (target) | 2–5% | High failure rate | Highly variable |

| Renewable energy | 6–9% | 0.5–2% | Low | 5–8% |

Common pitfalls that erode returns further:

-

Focusing on gross ROI and ignoring platform risk or deal quality.

-

Investing heavily in a single deal or platform, amplifying concentration risk.

-

Neglecting the tax implications of interest income versus capital gains in your jurisdiction.

-

Reinvesting too slowly after deal maturity, leaving capital idle for months.

As experts advise, modelling defaults of 3–5% and diversifying across 10–30 deals while prioritising net-of-fees IRR over gross projections is the disciplined path, especially given illiquidity periods of 3–7 years that demand patience.

Pro Tip: When evaluating a platform, always request historical net returns, not just target rates. Legitimate platforms will publish loan book performance data showing actual default rates and realised net yields over time.

Diversification is genuinely your most powerful tool here. Spreading capital across investing in loans from multiple borrowers and sectors limits the damage any single default can do to your overall portfolio performance.

Comparing ROI across crowdfunding types: Real estate, startups, and beyond

Having isolated the drivers of true take-home returns, it is time to see how different European crowdfunding options really stack up.

Not all crowdfunding asset classes are created equal. Each carries its own risk profile, time horizon, and return potential, and the right mix depends entirely on your personal investment goals. Here is a direct comparison:

| Asset class | Expected net ROI | Risk level | Typical holding period | Liquidity |

|---|---|---|---|---|

| Real estate debt | 5–9% p.a. | Medium | 1–3 years | Low |

| Real estate equity | 8–14% IRR | Medium-High | 3–7 years | Very low |

| Business loans | 5–10% p.a. | Medium-High | 6 months–3 years | Low |

| Startup equity | Variable / high upside | Very High | 5–10 years | Very low |

| Renewable energy | 5–8% p.a. | Low-Medium | 5–15 years | Very low |

How to evaluate which asset class fits your strategy:

-

Define your time horizon first. If you need capital back within two years, startup equity or long-term renewable energy bonds are unsuitable. Real estate debt with shorter maturities fits better.

-

Assess your risk tolerance honestly. Startup investing can produce spectacular returns, but the majority of individual startups fail. Only allocate capital here that you can afford to lose entirely.

-

Calculate your target net yield. Work backwards from your income or wealth-building goal. If you need 7% net annual return, real estate debt or diversified crowdlending are the realistic paths.

-

Consider the regulatory environment. Europe’s ECSP (European Crowdfunding Service Provider) regulation now standardises protections across member states, making it easier to compare platforms directly.

-

Factor in reinvestment frequency. Shorter-term business loans return capital faster for reinvestment, compounding your returns more rapidly than a seven-year equity hold.

“The most successful crowdfunding investors in Europe are not those chasing the single highest yield. They are those who build structured, multi-asset portfolios that deliver consistent, risk-adjusted net returns year after year.”

Real estate crowdfunding portfolios targeting 8–12% net after fees remain the backbone of many European crowdfunding strategies, providing income whilst equity positions in startups and renewables offer longer-term growth potential.

A practical approach for most European investors is to allocate the majority of their crowdfunding capital (around 60–70%) to lower-risk debt instruments such as real estate loans and business credit, with the remainder spread across equity opportunities. Understanding the real estate investing guide for Europe alongside the startup investing benefits helps you strike this balance with confidence. 🌱

How to maximise your crowdfunding ROI (Expert strategies)

After understanding what is possible and how risk varies, let us move from theory to practice with the strategies real experts use to improve their crowdfunding outcomes.

Improving your crowdfunding ROI is less about finding miracle deals and more about implementing a systematic, disciplined process. The investors who consistently outperform are those who treat crowdfunding as a structured asset class, not a lottery.

Expert strategies that move the needle:

-

Spread across a minimum of 10–30 active deals. This is the most cited diversification rule for a reason. As expert analysis confirms, modelling 3–5% defaults and spreading across many deals smooths out the inevitable losses. With ten deals, one default hits you hard. With thirty, it barely registers in your annual return.

-

Always use net-of-fee IRR as your benchmark. A deal offering 13% gross with 2.5% in fees and a projected 2% default rate is only delivering roughly 8.5% net. Compare all deals on this single metric, and ignore headline marketing figures entirely.

-

Diversify across asset classes and geographies. Mixing Baltic crowdlending platforms with Spanish real estate debt and Dutch renewable energy bonds insulates you from localised economic downturns. Fractional diversification strategies make this accessible even with modest starting capital.

-

Reinvest returned capital promptly. Idle capital earns nothing. Build a reinvestment schedule so that when a deal matures, the funds move into the next position within days, not weeks. This discipline significantly boosts your effective annualised return through compounding.

-

Maintain a liquidity reserve outside crowdfunding. Because most deals have 3–7 year holding periods, you must never invest money you might need urgently. Keep three to six months of living expenses in liquid accounts, and only commit surplus capital to crowdfunding.

-

Review your portfolio quarterly, not daily. Crowdfunding is not a stock market. Checking prices every day serves no purpose and drives poor emotional decisions. Set a quarterly review cadence to assess overall performance, platform health, and allocation balance.

-

Prioritise platforms with secondary markets. Some European platforms now offer secondary markets where you can sell positions before maturity, providing a partial liquidity escape valve. This feature is worth a slightly lower headline rate in exchange for flexibility.

Pro Tip: When a deal looks suspiciously attractive (for example, a 16% secured real estate loan with no platform track record), that is your cue to investigate the platform’s loan book data, not to invest quickly. High advertised returns on new or unproven platforms often reflect higher actual risk, not better opportunity.

Why actual crowdfunding ROI is both simpler and harder than it looks

Here is what years of watching European crowdfunding markets have taught us at Crowdinform: the fundamentals of good ROI are genuinely simple. Diversify. Invest for the long term. Choose net returns over gross. Reinvest systematically. These principles are not complicated at all.

And yet, most investors struggle to apply them consistently, because crowdfunding triggers behavioural traps that sabotage rational strategy. The exciting new platform promising 15% feels more compelling than the disciplined portfolio delivering a steady 9% net. The failed deal creates panic that leads to poor exit decisions on perfectly healthy positions.

The real enemy of crowdfunding ROI is not defaults or fees. It is impatience and inconsistency. The investors we see consistently outperforming across EU platforms are those who commit to a strategy and then, frankly, get out of their own way. They understand from reading about crowdinvesting principles that illiquidity is not a bug but a feature. The illiquidity premium exists precisely because most investors are unwilling to wait. Those who are willing to wait are quietly collecting returns that liquid assets simply cannot match.

There is also a widespread misconception that maximising ROI means hunting for the single best-performing deal or platform in any given month. In practice, the opposite is true. Concentration in winners is hindsight investing. True outperformance comes from systematic risk control across a broad, balanced portfolio, not from placing bold bets. The European market has enough quality platforms and deal flow to build genuinely diversified portfolios without ever needing to reach for outlier risk. The discipline to build steadily and hold firmly is both the simplest and the hardest skill in crowdfunding. 🎂

Getting started: Grow your returns with Crowdinform

Armed with the right mindset and approach, putting this knowledge into action is easier with the right tools.

Crowdinform is Europe’s dedicated aggregator for crowdfunding platforms, bringing together data and independent reviews from over 500 platforms across the continent. Whether you are evaluating a real estate debt deal in Portugal or a renewable energy project in Germany, our AI copilot tool helps you assess each opportunity with data-driven project reviews and built-in exploration features. You no longer need to spend hours manually comparing platforms or guessing which deals meet your net-return threshold.

Explore current opportunities across real estate, startups, business loans, and renewable energy, all rated, reviewed, and contextualised for European investors. From diversification guidance to deal quality scoring, Crowdinform gives you the infrastructure to apply everything in this guide immediately and confidently. Join a growing community of European impact investors making smarter, better-informed crowdfunding decisions every day. 🚀🌱

Frequently asked questions

How is crowdfunding ROI actually calculated?

Crowdfunding ROI measures your annual net gain after fees, defaults, and associated costs, divided by your original capital invested. For longer deals, net-of-fee IRR is the superior metric as it accounts for the timing of each cash flow.

What is a good ROI for real estate crowdfunding in Europe?

A well-diversified real estate crowdfunding portfolio can realistically net 8–12% annually after fees, though equity-based deals may project 12–18% IRR across a 3–7 year holding period.

How do defaults impact crowdlending ROI?

Defaults typically reduce annual crowdlending returns by 3–5%, which is why spreading capital across many loans is essential. One disciplined investor achieved 12% net over five years by absorbing default losses through wide diversification.

How long should I expect my money to be tied up?

Most real estate and equity crowdfunding deals require 3–7 year holding periods before full returns are realised, so only commit capital you will not need during that window.

Is it possible to lose money with crowdfunding investments?

Yes, absolutely. Defaults, platform insolvency, and poor diversification can all result in partial or total loss of capital. Crowdfunding is not a guaranteed-return product, and all investments carry risk.