Earning competitive returns from business loans is no longer the exclusive preserve of banks and institutional funds. European investors now have direct access to a growing marketplace of lending-based crowdfunding platforms, where you can fund real businesses, earn regular interest, and build a genuinely diversified income portfolio. Business-loan crowdfunding is largely governed by the ECSPR, the EU-wide framework that sets investor protection standards across member states, making this one of the most regulated and transparent alternative asset classes available to retail investors today.

Key Takeaways

Point: Diversification is vital

Details: Spread investments across many loans and platforms to reduce risk.

Point: Regulation adds safety

Details: ECSPR-regulated platforms must provide transparent disclosures and investor protections.

Point: Automation offers efficiency

Details: Auto-invest features help diversify and save time, but manual review enhances control.

Point: Returns are not guaranteed

Details: All business loan investments carry risk, including borrower default and payment delays.

Point: Consider alternative routes

Details: Venture debt and institutional products offer additional options for experienced investors.

Point: New tools to make investing easier

Details: Crowdinform.com AI tool makes investing in crowdfunding easier and more secure.

What you need to start investing in business loans

Before you transfer a single euro, it pays to understand the regulatory landscape and practical requirements that shape business loan investing in Europe. The good news is that the framework is clear, and getting started is more straightforward than many investors expect.

The first and most important rule: only invest through platforms that hold a valid ECSPR licence (or proper local licence). The European Crowdfunding Service Providers Regulation requires platforms to provide standardised disclosures, maintain investor protection measures, and operate under oversight from their national competent authority. You can find an overview of crowdfunding regulations and check platform licensing status before committing any capital.

Understanding how commercial lending works is also genuinely useful before you start. Business loans on crowdfunding platforms typically fall into three instrument types:

-

Loan-based (debt) crowdfunding: You lend money directly to a business and receive principal plus interest repayments over a fixed term. This is by far the most prevalent structure, and loan-based crowdfunding accounts for more than half of 2024 EU crowdfunding funding volumes.

-

Debt-based securities: Platforms issue notes or bonds backed by underlying business loans, often with more structured terms and covenants.

-

Equity-linked debt: Hybrid instruments where returns may include an equity kicker alongside interest, common in venture-stage business lending.

Before your first investment, you will need to complete the following:

-

✅ Identity verification (IDV): All ECSPR platforms require full KYC (Know Your Customer) checks, including passport or national ID and proof of address.

-

✅ Investor questionnaire: Platforms must assess your knowledge and experience; you may be classified as a sophisticated or non-sophisticated investor, which affects access to certain products.

-

✅ KIIS review: The Key Investor Information Sheet (KIIS, sometimes called KIID) is a standardised document summarising each project’s risks, returns, and terms. Reading it is not optional.

-

✅ EU/EEA residency: Most platforms require EU or EEA residency for retail investors, though some accept investors from additional jurisdictions.

-

✅ Minimum capital: Starting amounts vary widely by platform.

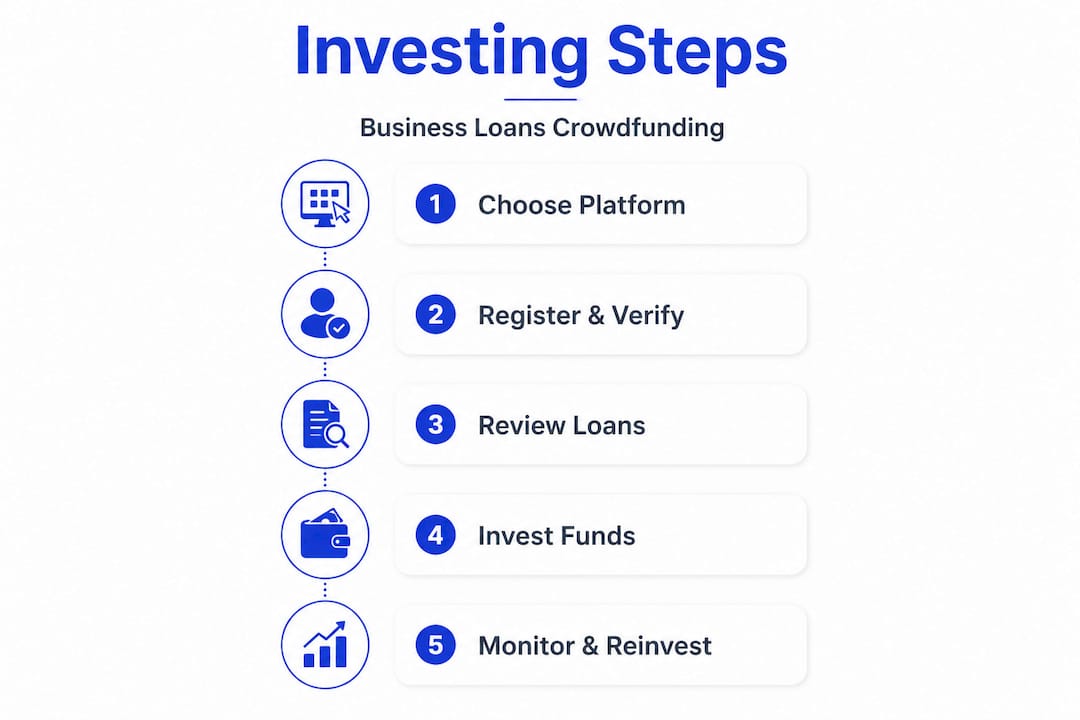

Step-by-step: How to invest in business loans via crowdfunding

With your prerequisites ready, here is exactly how to start investing step by step. 🚀

Step 1: Shortlist platforms. Look for platforms specialising in business loans rather than consumer credit or real estate, as the loan structures and risk profiles differ significantly. Crowdinform aggregates data on over 500 European platforms, making it straightforward to filter by asset class and regulatory status. Here is a list of European crowdfunding platforms.

Step 2: Complete onboarding and identity verification Register on your chosen platform and complete the full KYC process. This typically involves uploading identity documents and answering a suitability questionnaire. Most platforms complete verification within 24 to 48 hours.

Step 3: Review project listings and KIIS documents Before investing in any loan, read the KIIS carefully. Pay attention to the borrower’s credit assessment, loan-to-value ratio (where applicable), interest rate, loan term, and any security or collateral provided.

Step 4: Make your first investment Deposit funds via SEPA bank transfer and allocate to your chosen loans. Most platforms allow fractional investment, meaning you can spread €500 across 5 different loans at €100 each, which is a sensible starting approach.

Step 5: Monitor and reinvest repayments As borrowers repay principal and interest, funds return to your account. Reinvesting repayments promptly keeps your capital working and compounds your returns over time. Investors can invest in business-loan notes or fractional loan interests on marketplace platforms, with returns generated directly from borrower repayments.

Step 6: Use auto-invest for scale and efficiency Once you are comfortable with the platform’s loan selection, auto-invest tools can deploy capital automatically according to your pre-set criteria, such as minimum interest rate, maximum loan term, and borrower risk grade.

Pro Tip: Set your auto-invest criteria conservatively at first, focusing on shorter loan terms (6 to 24 months) and higher-grade borrowers. This gives you faster capital recycling and a clearer picture of actual default rates before you extend into longer or riskier loans.

When reviewing project-level risk modelling, pay close attention to how each platform assesses borrower creditworthiness. Some use proprietary scoring models, others rely on third-party originator assessments. Understanding the methodology behind the risk grade is far more valuable than simply chasing the highest advertised yield.

Managing risk and building a diversified business loan portfolio

Having invested, the next crucial step is protecting your capital and maximising long-term returns. Risk management in business loan investing is not complicated, but it does require discipline and regular attention. 🛡️

The single most effective risk control is diversification. Spreading your capital across many loans, multiple borrowers, and ideally several platforms reduces the impact of any single default. Portfolios diversified across many loans and originators, without excessive concentration, represent the core mitigation strategy against default clustering, where multiple loans in the same sector or geography fail simultaneously.

Core diversification strategies to implement:

🔹 Spread across at least 10 to 20 loans to reduce single-loan concentration risk below 10% of your portfolio per loan.

🔹 Diversify across sectors and geographies as business loan performance can be correlated within industries during economic downturns.

🔹 Limit platform concentration by using three or five platforms, reducing the risk that a single platform’s operational failure affects your entire portfolio.

🔹 Stagger loan maturities so that capital returns to you at regular intervals, maintaining liquidity without forcing you to sell on a secondary market.

“Even experienced crowdlending investors stress-test their assumptions about business debt service capiacity and platform solvency. ”

For portfolio risk management at scale, consider reviewing your portfolio composition at least quarterly. Check for unintended concentration that may have built up through auto-invest, particularly if one originator has been issuing a disproportionate share of available loans.

Pro Tip: Keep individual loan allocations to 1 to 2% of your total portfolio. If one borrower defaults, the impact on your overall return is manageable. Losing 1% of capital to a default is an acceptable cost of doing business; losing 20% because of a single large position is not.

Beyond P2P: Alternative ways to invest in business loans

If you want to broaden your exposure or invest larger sums, alternative routes may be of interest. Crowdfunding platforms are excellent for retail-scale investing, but they are not the only way to access business loan returns in Europe.

Institutional venture debt is one of the most compelling alternatives for investors with larger capital bases. Venture debt is a form of structured lending to growth-stage companies, typically alongside or following equity funding rounds. The European Investment Bank, for example, offers venture debt products targeting eligible innovative businesses across the EU. These instruments are structured very differently from retail crowdlending, with bespoke terms, covenants, and access routes that generally require institutional or high-net-worth investor status.

Direct lending funds provide another route. These are professionally managed vehicles that deploy capital into a diversified portfolio of business loans, offering investors exposure without the need to select individual loans. Minimum investments are typically €50,000 or higher, and liquidity is often limited to quarterly or annual redemption windows.

Bridge loans and structured credit are worth exploring for investors comfortable with shorter-duration, higher-yield instruments. Understanding the difference between bridge loans and traditional loans is useful here, as bridge lending often carries higher rates but shorter terms and specific exit triggers.

These alternatives suit specific investor profiles:

-

💼 Investors with €100,000+ who want institutional-grade diversification and professional management.

-

🌱 Impact-focused investors seeking exposure to innovative EU businesses through structured venture debt.

-

⚡ Experienced investors comfortable with illiquidity in exchange for higher gross annual yields.

-

🔄 Investors looking to complement a crowdfunding portfolio with longer-duration, lower-correlation assets.

What most guides miss about business loan investing

Most how-to guides focus on the mechanics: sign up, verify, invest, diversify. That advice is sound, but it leaves out the harder lessons that only emerge after you have actually managed a live portfolio through a full credit cycle.

The first thing to scrutinise is platform incentives. Platforms earn fees when loans are originated and funded. This creates a structural bias toward volume over quality. A platform with strong loan flow looks attractive, but if origination standards are slipping to maintain that flow, you are the one absorbing the credit risk. Always explore platfrom performance indicators, how much is overdue, what is the risk cost? If statistics are not provided or platfrom shows just one number, e.g. 0% defoults, it signals a lack of transparency and is a red flag.

Finally, do not underestimate the value of reviewing your portfolio composition regularly, not just your headline return figure. A portfolio showing 10% average yield may contain a hidden concentration in loans from one sector or originator. The return looks great until it does not. Focus on process: consistent diversification, disciplined reinvestment, and honest assessment of platform health. Platform branding and marketing materials are not a substitute for that rigour.

The investors who succeed over five-year-plus horizons in business loan crowdfunding are not the ones who found the highest-yielding platform. They are the ones who built disciplined, diversified portfolios and stayed alert to the structural risks that come with lending to businesses at scale.

Discover curated platforms to start your business loan investing journey

You have the framework, the risk management principles, and the step-by-step process. Now it is time to put it into practice with the right tools. 🎂

Crowdinform aggregates and reviews over 500 European crowdfunding platforms, giving you a TripAdvisor-style overview of platforms for investing in business loans, P2P lending, and alternative assets. Our AI copilot reviews individual investment projects, flags concentration risks, and helps you compare platforms by regulatory status, minimum investment, and asset class. Whether you are building your first business loan portfolio or expanding an existing one, Crowdinform gives you the data and insights to invest with confidence, not guesswork. Explore the platform today and let the AI tools do the heavy lifting on due diligence.

Frequently asked questions

What is the minimum amount needed to invest in business loans in the EU?

Minimum investments typically start from as little as €50-€100 on most crowdfunding platforms. For institutional routes such as EIB venture debt and direct lending funds, minimums are substantially higher, often €50,000 or more.

How are business loan platforms regulated in Europe?

Most platforms are regulated under the ECSPR framework, which requires standardised investor disclosures, suitability assessments, and supervision by national competent authorities across EU member states.

Can I withdraw early from a business loan platform?

Some platforms offer secondary market liquidity, allowing you to sell your loan positions before maturity. Others require you to hold until the loan term ends, so always check the exit options before investing.

Is it better to use auto-invest or pick loans manually?

Auto-invest is efficient for diversification at scale, but manual selection lets you review each project’s specific risk, terms, and borrower profile. A combined approach, using auto-invest with conservative criteria and manually reviewing larger allocations, tends to work well.

Are returns from business loans guaranteed?

Returns are not guaranteed. Even platforms with buyback policies can face stress if originators encounter liquidity problems. As investors earn returns only as loans are repaid, defaults and delays directly affect your actual yield. Always treat advertised rates as targets, not promises.