If you’re serious about diversifying your portfolio beyond stocks and bonds, understanding what is debt crowdfunding could open a genuinely exciting avenue. Unlike donation or reward models most people picture when they hear “crowdfunding,” debt crowdfunding is a lending-based investment structure where you earn returns through interest repayments. It has quietly carved out a 31% share of all crowdfunding offerings between 2016 and 2024, making it one of the most active corners of the alternative investment market. This guide unpacks how it works, what the regulations mean for you, and how to invest with confidence.

| Point | Details |

|---|---|

| Debt crowdfunding is lending-based | Investors provide loans to businesses or individuals and earn fixed interest returns over a set term. |

| Regulation shapes your protection | Platforms must register with regulators; investment caps and disclosure rules protect retail investors. |

| Risk diversification is critical | Spreading capital across multiple loans and platforms reduces exposure to any single default. |

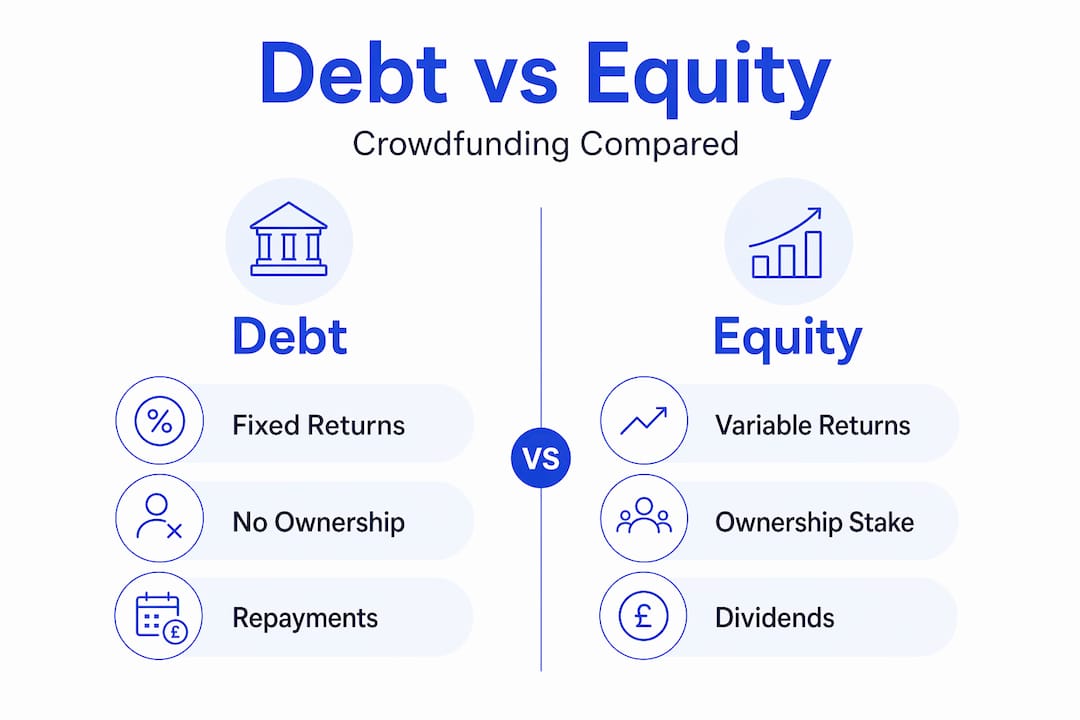

| Debt differs from equity crowdfunding | Debt investors receive repayments with interest; equity investors receive ownership stakes with uncertain returns. |

| Platform selection matters enormously | The compliance health of your chosen platform directly affects the security of every investment you hold there. |

What is debt crowdfunding and how does it work?

At its core, debt crowdfunding is peer-to-peer lending conducted through an online platform. You lend money to a business or individual borrower, and in return, they repay you the principal plus interest over an agreed period. It is sometimes called P2P lending, marketplace lending, or loan-based crowdfunding. The terminology varies, but the mechanics are the same.

Three key players make the model work:

-

Issuers (borrowers): Businesses or individuals seeking capital they cannot, or choose not to, access through traditional banks.

-

Investors (lenders): Individuals like you who fund those loans in exchange for interest income.

-

Intermediaries (funding portals): Regulated online platforms that vet borrowers, host listings, process transactions, and handle compliance.

The process is relatively straightforward. A borrower applies through a platform, which conducts credit assessments and sets loan terms including interest rate, duration, and repayment schedule. The offering is then listed for investors to fund, often in small increments so multiple investors share the loan. Once the target is reached, funds are disbursed to the borrower, who begins making repayments on a monthly or quarterly basis.

Typical offerings run for a median duration of around four months for the fundraising window, with loan terms extending further depending on the product. Maximum raises average around €1 million per offering. For investors, this translates to predictable, fixed-income-style cash flows, which is one reason debt crowdfunding appeals strongly to those seeking yield beyond savings accounts or government bonds.

The regulatory framework you need to know

Regulation is not just bureaucratic background noise. It is the architecture that determines whether your money is protected or exposed. In the United States, Regulation Crowdfunding (Reg CF) is the primary framework governing debt crowdfunding offerings, and understanding its key provisions tells you a lot about what responsible platforms should look like globally.

Here are the core regulatory pillars under Reg CF:

-

Issuer raise cap: Businesses can raise a maximum of $5 million per 12-month period under Reg CF in the USA and €5 milion EURO in Europe, which limits platform exposure and protects market integrity.

-

Mandatory disclosures: Issuers must provide audited or reviewed financial statements, business plans, and intended use of funds, giving investors material information before committing capital.

-

Investment limits: Retail investors face caps based on income and net worth, applied through a self-certification process that limits individual overexposure.

-

Intermediary registration: All platforms must register with the SEC and FINRA as either a broker-dealer or a funding portal, and they operate under a ‘broker-dealer lite’ model with distinct but real compliance obligations in the USA and the EU. They must be registered under an ECSP licence.

-

Ongoing reporting: Issuers must file annual reports, keeping investors informed beyond the initial fundraising window.

“For investors, understanding intermediary legal duties is as important as evaluating individual offerings.” Understanding who is gatekeeping your investment is not optional due diligence. It is the first line of defence.

Funding portals serve as critical gatekeepers between issuers and investors, legally obligated to verify disclosures, prevent fraud, and maintain regulatory standing. Critically, portal non-compliance can invalidate all offerings hosted on that platform, meaning a platform’s regulatory health is your financial concern, not just theirs.

In Europe, frameworks like the EU Crowdfunding Regulation (ECSPR) impose similar principles: platform authorisation, investor disclosures, and cross-border access controls. International variations matter too. Some models, such as Kiva’s Indian loan portfolio, introduce mandatory three-year holding periods and currency fluctuation risks that are uncommon in standard domestic debt crowdfunding.

Pro Tip: Before committing to any platform, verify its regulatory registration status directly on the relevant authority’s website. In Europe, check the national regulator’s authorised firms register. This takes five minutes and removes a category of risk entirely.

Debt crowdfunding vs other investment types

Knowing where debt crowdfunding sits relative to other options helps you allocate intelligently. Here is a direct comparison:

| Investment type | Returns | Risk level | Liquidity | Investor role |

|---|---|---|---|---|

| Debt crowdfunding | Fixed interest (typically 5–12% p.a.) | Medium | Low to medium | Lender |

| Equity crowdfunding | Variable (capital gains, dividends) | High | Very low | Part-owner |

| Traditional bank savings | Low (0.5–3% p.a.) | Very low | High | Depositor |

| Listed bonds | Fixed coupon (2–8% p.a.) | Low to medium | High | Bondholder |

| Stock market equities | Variable | High | High | Shareholder |

The most useful contrast is between debt and equity crowdfunding. With equity crowdfunding, you take an ownership stake in a business and your returns depend entirely on the company’s growth or sale. With debt crowdfunding, repayment is contractually obligated regardless of company performance, as long as the borrower does not default. That makes debt crowdfunding behave more like a bond than a share.

Compared with traditional bank loans, debt crowdfunding offers borrowers faster access to capital and investors a significantly higher yield than a savings account. The trade-off is liquidity. Secondary markets exist on some platforms, but they are not universally available, and selling your loan position before maturity is not always straightforward. Understanding crowdfunding ROI in detail helps you frame realistic return expectations before you commit.

Assessing risks and rewards

Debt crowdfunding can generate competitive yields, but the risks are real and specific. Knowing them is what separates thoughtful investors from those who get caught out.

The primary risks to manage include:

-

Default risk: The borrower fails to repay. Platform credit assessments reduce this probability, but they cannot eliminate it. Always review the platform’s historical default rates.

-

Platform risk: If the platform itself fails or loses regulatory standing, recovering your investment becomes legally complicated and slow.

-

Liquidity risk: Most debt crowdfunding investments are illiquid for their full term. Do not invest money you may need at short notice.

-

Regulatory risk: Changes in regulation can affect platform operations, investor caps, or market access, particularly in cross-border scenarios.

-

Currency risk: Investments denominated in foreign currencies carry exchange rate exposure that can erode real returns.

Diversification through debt crowdfunding requires careful risk appraisal given variant loan terms and platform reliability. The practical implication: spread capital across multiple borrowers, multiple sectors, and ideally multiple platforms. A single loan default on a diversified portfolio of 30 loans has a far smaller impact than the same default on a portfolio of three.

Credit assessment quality varies considerably between platforms. Look for platforms that publish their underwriting criteria, provide borrower financial summaries, and disclose loan-level performance data. Strict investment limits and compliance obligations constrain growth but genuinely protect retail investors from overexposure.

Pro Tip: Treat each platform as a separate risk exposure, not just each loan. If one platform goes offline, all loans hosted there become uncertain. Cap your total allocation to any single platform at 30–40% of your debt crowdfunding budget.

How to start investing in debt crowdfunding

Getting started requires methodical preparation rather than enthusiasm alone. Here is a practical sequence:

-

Research and shortlist platforms. Look for platforms with regulatory authorisation, published track records, transparent fee structures, and accessible investor reports. Crowdinform aggregates reviews and performance data for over 500 European platforms, which removes considerable legwork from your initial research.

-

Evaluate individual loan listings. Key data points to review: borrower credit grade, loan-to-value ratio (for secured loans), loan term, interest rate, repayment structure (bullet vs amortising), and any collateral backing.

-

Understand fee structures. Platforms typically charge investors a service fee ranging from 0.5% to 2% annually, or take a spread between the borrower rate and investor rate. Read the fee schedule carefully before committing.

-

Set your allocation limits. Decide what percentage of your total portfolio belongs in debt crowdfunding. Many advisers suggest capping alternative investments at 10–20% for retail investors. Within that, diversify across loan types and platforms.

-

Monitor and manage actively. Log into your platform dashboard regularly, review repayment statuses, and act on any early warning signals such as borrower payment delays or platform regulatory notices.

-

Plan your exits. Before investing, check whether the platform offers a secondary market. Even if you intend to hold to maturity, knowing your exit options is good risk management.

Learning to analyse investment projects at the listing level is a transferable skill that improves every investment decision you make across asset classes, not just debt crowdfunding.

My honest take on debt crowdfunding

I’ve spent considerable time studying how European retail investors approach debt crowdfunding, and one pattern stands out consistently. Most people who underperform do not make bad individual loan choices. They choose platforms carelessly and over-concentrate in one or two of them.

The platform is the infrastructure of your investment. When a platform has weak compliance, poor transparency, or shaky financials, every loan hosted there carries extra systemic risk that the individual loan metrics simply cannot reflect. I’ve seen investors with sensible diversification across 40 loans lose access to capital for two years because the platform entered administration. That is not a loan risk story. That is a platform selection failure.

My recommendation is to treat platform due diligence as the non-negotiable first step, not an afterthought. Read the platform’s annual reports. Check its regulatory filings. Look at its handling of previous defaults. Does it communicate clearly with investors when things go wrong? That last point tells you more than any marketing headline ever will.

The regulatory direction of travel in Europe is genuinely encouraging. The ECSPR framework is building more consistent standards across borders, and platforms that take compliance seriously are gaining investor trust and assets accordingly. Debt crowdfunding is not a shortcut to outperformance. But for investors willing to do the homework, it offers a genuinely differentiated yield source that complements both equities and bonds in a well-structured portfolio.

— Jevgenijs

Explore debt crowdfunding with Crowdinform

Ready to put this knowledge to work? Crowdinform is Europe’s most comprehensive aggregator for crowdfunding platforms, covering over 500 platforms with verified reviews, live project data, and an AI copilot that analyses individual investment opportunities for you.

Whether you are evaluating your first debt crowdfunding platform or optimising an existing alternative investment portfolio, Crowdinform gives you the data layer that individual platforms cannot. Compare gross annual yields, platform track records, default histories, and regulatory status all in one place. Discover crowdfunding investment opportunities across debt, real estate, and startup categories, and use the built-in AI tools to assess project quality before you commit a single euro. Smarter investing starts with better information.

FAQ

What is debt crowdfunding in simple terms?

Debt crowdfunding is when multiple investors collectively lend money to a borrower through an online platform, earning interest on their loans over a fixed term. It is often called peer-to-peer or P2P lending.

How does debt crowdfunding differ from equity crowdfunding?

In debt crowdfunding, investors receive scheduled repayments with interest and have no ownership stake. In equity crowdfunding, investors receive shares in the business and returns depend on company performance.

What returns can I expect from investing in debt crowdfunding?

Returns typically range from 5% to 12% per annum depending on the platform, loan type, and borrower risk profile, though higher rates generally indicate higher default risk.

Are debt crowdfunding platforms regulated?

Yes. Reputable platforms must register with relevant financial authorities. In the US, this means SEC and FINRA registration. In Europe, platforms must be authorised under national or EU-level frameworks such as the ECSPR.

What is the biggest risk in debt crowdfunding?

Default risk (borrower non-repayment) and platform risk (platform failure or regulatory issues) are the two most significant exposures. Diversifying across multiple loans and platforms is the most effective way to manage both.

Recommended

- What is crowdinvesting? A modern guide for European investors - Article | Crowdinform Investment Guides Startups

- How to invest in business loans via crowdfunding in Europe - Article | Crowdinform Investment Guides Crowdlending, How to invest in loans?, Invest in loans

- Crowdfunding ROI explained: Maximising returns in Europe - Article | Crowdinform Investment Guides Crowdfunding

- Step-by-step real estate investing in Europe: a clear guide - Article | Crowdinform Investment Guides Real estate crowdfunding