Selecting the right crowdfunding platform from hundreds of options across Europe is genuinely complex. You face competing claims about returns, varied regulatory standings, and real differences in risk exposure depending on whether you are backing real estate debt, startup equity, or renewable energy projects. This investment platform comparison guide cuts through that noise. It focuses specifically on European crowdfunding, covering the regulatory framework you must understand, the key differences between lending and equity models, and the practical steps to evaluate platforms rigorously before committing a single euro.

Key takeaways

| Point | Details |

|---|---|

| ECSPR licence is your baseline filter | Verify any platform holds a valid ECSP licence with its competent authority before reviewing deals or returns. |

| Investment model shapes your risk profile | Lending-based and equity-based crowdfunding differ fundamentally in cash flow timing, collateral, and loss exposure. |

| Fees erode net returns significantly | Compare full fee schedules, not just advertised yields, especially on smaller investment amounts. |

| Vintage year data reveals true performance | Assess loan cohort data by origination year, not marketing averages, to understand real default and recovery rates. |

| Diversification requires active platform choices | The EUR 5 million project cap under ECSPR means spreading capital across platforms and asset classes matters greatly. |

The regulatory baseline every investor must check

Before comparing fees or projected yields, you need a firm grasp of the legal framework governing European crowdfunding platforms. The European Crowdfunding Service Providers Regulation (ECSPR) is the standard industry term for what many platforms now call their EU crowdfunding licence. It replaced a fragmented patchwork of national rules with unified EU crowdfunding rules, allowing licensed platforms to passport their services cross-border under a single authorisation.

This matters enormously for you as an investor. A platform licensed under ECSPR can legally operate across EU member states, which broadens your access to deals in countries like Estonia, the Netherlands, or Spain without those platforms needing separate national licences. However, local language and market familiarity still affect the investor experience, even where passporting applies. Cross-border legal structures and recovery mechanisms can vary meaningfully.

The ECSPR also mandates specific investor protections that you should actively look for:

-

Key Investment Information Sheet (KIIS): Every project must provide a standardised 6-page disclosure document before you invest, summarising risks, returns, and legal terms.

-

Appropriateness assessments: Platforms are required to assess whether investments suit your financial situation and knowledge.

-

Cooling-off periods: Non-sophisticated investors receive a reflection period before commitments are locked in.

-

Investment limits: Caps apply for non-sophisticated investors to limit overexposure.

Verifying licence status is not simply a matter of trusting a platform’s website badge. You should confirm active licence status directly with the issuing competent authority in the relevant member state. ESMA maintains publicly accessible registers for this purpose.

Pro Tip: Cross-reference a platform’s claimed licence on your national financial regulator’s website or ESMA’s register, not just the platform’s own “About” page. Platforms have been known to overstate their compliance status before full authorisation is granted.

One caution worth stressing: an ECSPR licence confirms regulatory authorisation, not investment quality. Compliance items like KIIS and suitability form a baseline filter only. Actual platform risk depends on deal-level economics and collateral structures, which the next section covers in depth.

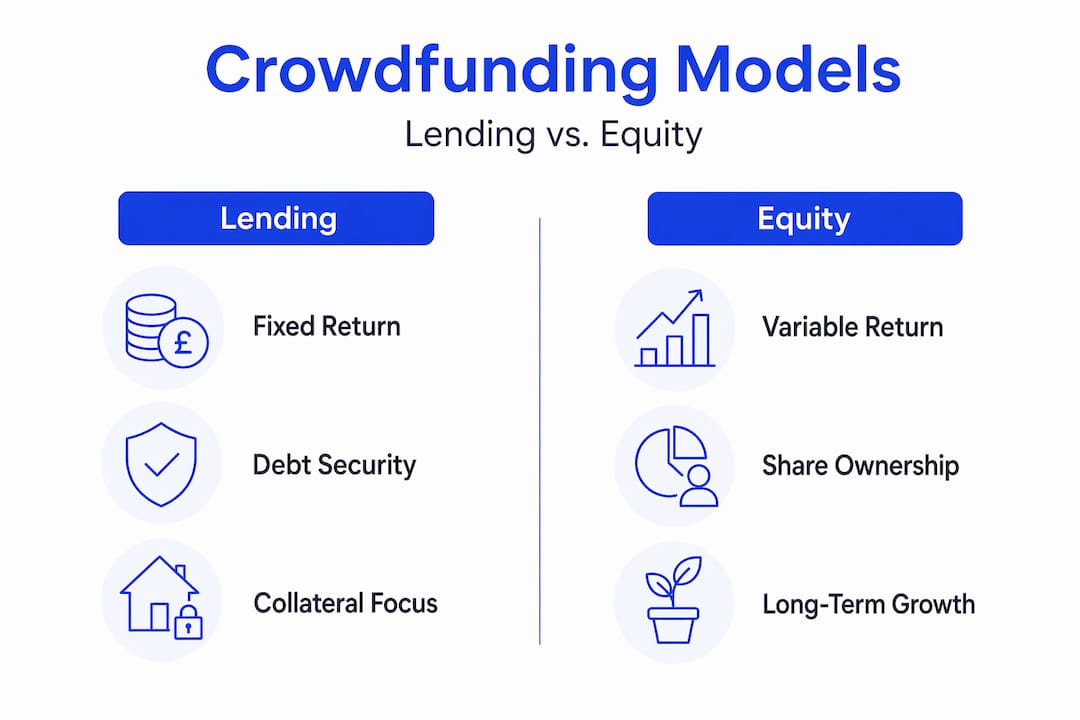

Lending versus equity: comparing crowdfunding models

Understanding investment models is central to any serious investment platform comparison, because the model determines your risk exposure, cash flow timing, and what happens if things go wrong.

The table below outlines the core distinctions:

| Feature | Lending-based (debt) | Investment-based (equity) |

|---|---|---|

| Investor return | Fixed interest payments | Dividends or capital gains on exit |

| Cash flow timing | Regular (monthly or quarterly) | Uncertain, often long-term |

| Collateral | Often secured (e.g. mortgage) | Generally unsecured |

| Default risk | Borrower default with recovery process | Total loss if company fails |

| Common asset classes | Real estate loans, SME debt, green energy bonds | Startups, growth companies, property equity |

| Liquidity | Secondary market possible under ECSPR | Illiquid until exit event |

For real estate debt platforms, collateral legal priority is where your risk analysis must focus. A first-rank mortgage is the most protective position for investors. Subordinated or mezzanine loans sit behind senior debt in any recovery, meaning losses in a default scenario are substantially higher. Many platforms market loans simply as “secured” without clarifying their position in the priority stack. That omission matters.

For startup equity, the risk profile shifts entirely. You are backing an illiquid stake with no guaranteed return. The upside can be compelling, particularly for early-stage projects, but the timeline to exit is typically measured in years rather than months. Platforms operating in this space should publish portfolio company updates regularly to allow ongoing monitoring.

Vintage year loan performance data is one of the most underused evaluation tools available to debt platform investors. Rather than accepting an advertised average yield, you look at cohorts of loans originated in specific years and track what percentage defaulted, how much was recovered, and over what timeframe. This gives you a realistic sense of underwriting discipline across different economic conditions, including stress periods like 2020 or 2022.

Practitioners building evaluation matrices separate regulatory compliance, economic deal structure, and operational features into distinct assessment layers. Applying this three-layer framework to any platform, regardless of asset class, produces a far more honest comparison than relying on headline metrics alone.

Fees, tools, and transparency

Fee structures across European crowdfunding platforms vary considerably, and the impact on net returns is often underestimated, particularly for investors starting with smaller amounts. Here is what to examine closely:

-

Platform fees: Charged either to borrowers, investors, or both. Some platforms advertise zero investor fees while embedding their margin in the interest rate spread.

-

Transaction fees: Applied on individual investments, often as a percentage of capital deployed.

-

Withdrawal and currency fees: Relevant if the platform operates in a currency other than your base currency.

-

Inactivity fees: Applied when accounts remain dormant, a detail often buried in terms and conditions.

The existence of a secondary market or bulletin board is a significant operational differentiator. Under ECSPR, platforms may offer secondary trading facilities, though these are not mandatory. Platforms that do provide one give you a meaningful exit route before loan maturity, which is particularly valuable for real estate debt investments with 12 to 36-month durations.

Transparency and compliance implementation vary widely across licensed platforms. A licensed platform is not necessarily a transparent one. Look for platforms that publish loan performance statistics publicly, disclose default rates and recovery timelines, and make KIIS documents accessible before registration is required.

Pro Tip: Download KIIS documents for five or six projects across a platform before investing. If the risk disclosures read as boilerplate and fail to specify collateral details, repayment ranks, or borrower financials, treat that as a red flag regardless of the advertised yield.

Dashboard quality and portfolio management tools also belong in your comparison. The best platforms allow you to filter investments by asset class, monitor cash flow projections, and track individual loan statuses. Some now incorporate AI-assisted project summaries, which can meaningfully reduce the time needed to assess individual deals.

A practical step-by-step comparison approach

Applying a structured process turns platform comparison from a vague exercise into a repeatable, reliable method. Here is a clear sequence you can follow:

-

Verify licence status. Confirm the platform holds a valid ECSP licence via your national regulator or ESMA’s register, not the platform’s website alone.

-

Review the KIIS for three or more live projects. The KIIS standardised document reveals the project risk profile, legal structure, and projected returns in a consistent format.

-

Assess collateral type and legal priority. For debt platforms, identify whether loans are first-rank secured, subordinated, or unsecured. Collateral priority and legal recovery paths determine actual risk beyond marketing labels.

-

Request or locate vintage year performance data. Ask for loan cohort statistics broken down by origination year. Absence of this data is informative in itself.

-

Build a full fee schedule. Calculate the net return after all fees on a realistic investment size, not just the gross yield headline.

-

Assess secondary market and exit options. Check whether the platform offers a resale facility and what the typical liquidity looks like in practice.

-

Consider the EUR 5 million project cap. The ECSPR financing cap limits project size, which shapes the risk profile of deals. Smaller projects may carry higher concentration risk.

-

Compile findings in a comparison table. Organise your research across platforms using a consistent structure.

| Comparison criterion | What to look for |

|---|---|

| ECSP licence verified | Confirmed with issuing authority, not website |

| Collateral and legal priority | First-rank mortgage preferred for debt |

| Vintage year default rate | Available and consistently below 5% in stable years |

| Net return after fees | Calculated on your target investment size |

| Secondary market available | Yes, with realistic liquidity |

| Reporting and transparency | Public data, not gated behind registration |

You can also explore regulated crowdfunding platforms in depth for a fuller overview of how the EU framework shapes platform comparisons in 2026.

Common pitfalls and how to avoid them ⚠️

Even experienced investors stumble when comparing crowdfunding platforms. These are the mistakes that surface most often and that cost the most when they materialise.

-

Accepting advertised yields at face value. A 12% gross yield on a subordinated loan with weak collateral can produce a net loss after default and fees. Always contextualise yield against risk rank and fee structure.

-

Ignoring loan priority. Not all “secured” loans offer the same protection. A second-charge loan is fundamentally different from a first-rank mortgage in a recovery scenario.

-

Skipping licence verification. Some platforms operate under grandfathering provisions or in the process of authorisation. Investing before full ECSP licence confirmation exposes you to unregulated risk.

-

Underestimating illiquidity. Secondary markets exist on some platforms but are not guaranteed. Committing capital you may need within 12 months to a 36-month real estate loan is a common structural mistake.

-

Ignoring the appropriateness assessment. ECSPR requires platforms to assess suitability. Rushing through this process or providing inaccurate information removes an important layer of protection the regulation is designed to provide.

Due diligence is not a one-time event before you invest. It is an ongoing practice: monitoring loan statuses, reading borrower updates, and reviewing platform-level statistics quarterly. The platforms that publish this data consistently are, in most cases, also the ones managing their loan books most carefully.

For a practical due diligence framework, PeerFounder’s due diligence checklists offer structured guidance specifically calibrated for European crowdfunding investors assessing authorised platforms.

My perspective on choosing platforms wisely

I have observed the European crowdfunding market evolve substantially over the past several years, and one consistent pattern stands out: investors who focus on regulatory status without diving into deal economics repeatedly end up disappointed.

An ECSPR licence tells you a platform has cleared the baseline. It does not tell you whether the loans are well underwritten, whether the collateral is actually enforceable, or whether the vintage year data holds up under scrutiny. I have seen platforms with impeccable compliance presentations and genuinely poor underwriting discipline. The two are not the same.

My honest recommendation is to spend 80% of your evaluation time on deal-level economics and only 20% on regulatory boxes. Read KIIS documents critically. Ask platforms directly for their 2020 and 2022 vintage cohort performance data. Those were stress years, and how a platform navigated them tells you more about credit quality than any marketing material ever will.

Diversification across platforms and asset classes is not just good portfolio theory. It is the only credible response to the fact that even well-regulated platforms carry idiosyncratic risk. Spreading exposure across real estate debt, renewable energy projects, and startup equity on separate ECSPR-licensed platforms gives you a genuine risk buffer. You can find structured guidance on how to analyse investment platforms to complement this framework.

— Jevgenijs

Explore smarter with Crowdinform

Ready to put this comparison framework into practice? Crowdinform is built precisely for European investors researching crowdfunding platforms across real estate, startups, and renewable energy. Aggregating data from over 500 platforms across Europe, Crowdinform provides investor reviews, project-level data, and an AI copilot that generates project assessments and helps you explore opportunities quickly and confidently.

Whether you are just beginning your crowdfunding journey or refining a portfolio across multiple asset classes, Crowdinform gives you the comparison tools and intelligence to invest with clarity. From platform rankings to AI-assisted deal reviews, everything you need to compare investment services across Europe is in one place. Start exploring at Crowdinform and see why thousands of European investors use it as their research home base.

FAQ

What is ECSPR and why does it matter for crowdfunding investors?

ECSPR is the EU-wide regulation governing crowdfunding service providers, replacing fragmented national rules. It introduces uniform licensing, mandatory KIIS disclosures, and investor protections that apply across member states.

How do I verify a crowdfunding platform’s licence?

Check the issuing national competent authority’s register or ESMA’s public database directly. Never rely solely on a platform’s own website claims, as authorisation status can change.

What is a KIIS and how should I use it?

A Key Investment Information Sheet is a standardised 6-page document required under ECSPR for every crowdfunding project. Read it to understand collateral details, legal structure, projected returns, and specific risk warnings before you invest.

How does collateral priority affect my risk in debt crowdfunding?

First-rank mortgages offer the strongest recovery position if a borrower defaults. Subordinated or second-charge loans sit behind senior debt and carry materially higher loss exposure in a default scenario.

What is vintage year data and why should I request it?

Vintage year data tracks loan cohorts by origination year, showing default rates and recovery outcomes over time. It reveals a platform’s true underwriting quality far more accurately than advertised average yields.