Many investors leap into real estate crowdfunding expecting straightforward, passive returns, only to face unexpected platform failures, payout delays, or funds locked in illiquid projects for years. The reality is that delays affect 20 to 50% of projects, with notable regulatory gaps across Germany and France adding further complexity. Yet these risks are manageable. With the right analytical framework, you can separate genuinely strong opportunities from overhyped ones, protect your capital, and invest with real confidence. This guide gives you exactly that: clear prerequisites, a step-by-step evaluation process, and ongoing monitoring strategies. 🚀

Key Takeaways

| Point | Details |

|---|---|

| Gather correct information | Start your analysis by collecting the right documents, verifying platform licensing, and ensuring all data is current. |

| Follow a step-by-step review | Always assess projects using a clear checklist, comparing debt and equity structures for security. |

| Watch for common red flags | Delays, lack of collateral, and unclear regulation should make you reconsider an investment. |

| Monitor investments actively | Stay up to date with project developments and platform communications after investing. |

| Be wary of high returns | If yields appear too high with minimal explanation or collateral, approach with caution and conduct extra due diligence. |

What you need before analysing opportunities

Once you recognise the risks, the next step is gathering the right tools and information to conduct a meaningful analysis. Jumping straight into project listings without preparation is one of the most common ways investors end up making costly decisions.

Start by collecting these key documents and data points:

-

✅ Platform licensing and regulatory status (ECSP registration in the EU)

-

✅ Project information memorandum (the formal project prospectus)

-

✅ Collateral terms and security agreements

-

✅ Historical return data and default rates from the platform

-

✅ Developer track record and previous project completions

-

✅ Independent property valuation reports

-

✅ Exit strategy documentation and project timelines

Due diligence is essential precisely because regulatory gaps and project overvaluation remain persistent issues across European markets. Platforms operating without full ECSP (European Crowdfunding Service Providers) compliance expose investors to significantly higher risk, so checking licences before anything else is non-negotiable.

Essential tools and research resources

| Tool or resource | Purpose | Where to find it |

|---|---|---|

| National regulatory registries | Verify platform licensing | AMF (France), BaFin (Germany), FCA (UK) |

| Platform track record database | Compare historical returns and defaults | Crowdinform, platform own statistics |

| Independent valuation reports | Confirm property appraisals | Requested directly from platform |

| ECSP registration list | Confirm EU authorisation | ESMA official register |

| Property market data | Benchmark valuations | Market analysis for property investments |

Cross-checking across multiple official sources is vital. Marketing materials from platforms are inherently optimistic. Regulatory filings and independent audits tell a far more accurate story. Before you follow a step-by-step investing guide, make sure you have your research tools ready and your accounts set up on relevant registries.

Pro Tip: Create a simple spreadsheet to log each platform’s licensing status, track record, and any red flags you identify. This structured habit saves significant time and keeps your analysis objective rather than emotion-driven.

Step-by-step process to analyse a real estate crowdfunding project

With all documents and research tools ready, you can now systematically evaluate each project using this framework. Skipping steps here is where most retail investors go wrong.

1. Verify platform credentials first

Before assessing a single project, confirm the platform is licensed under ECSP regulation and check its standing in the relevant national registry. A platform that is not properly authorised is not worth your time, regardless of the projected yields on offer. Find a list of platforms here: List of European Real estate crowdfunding platforms.

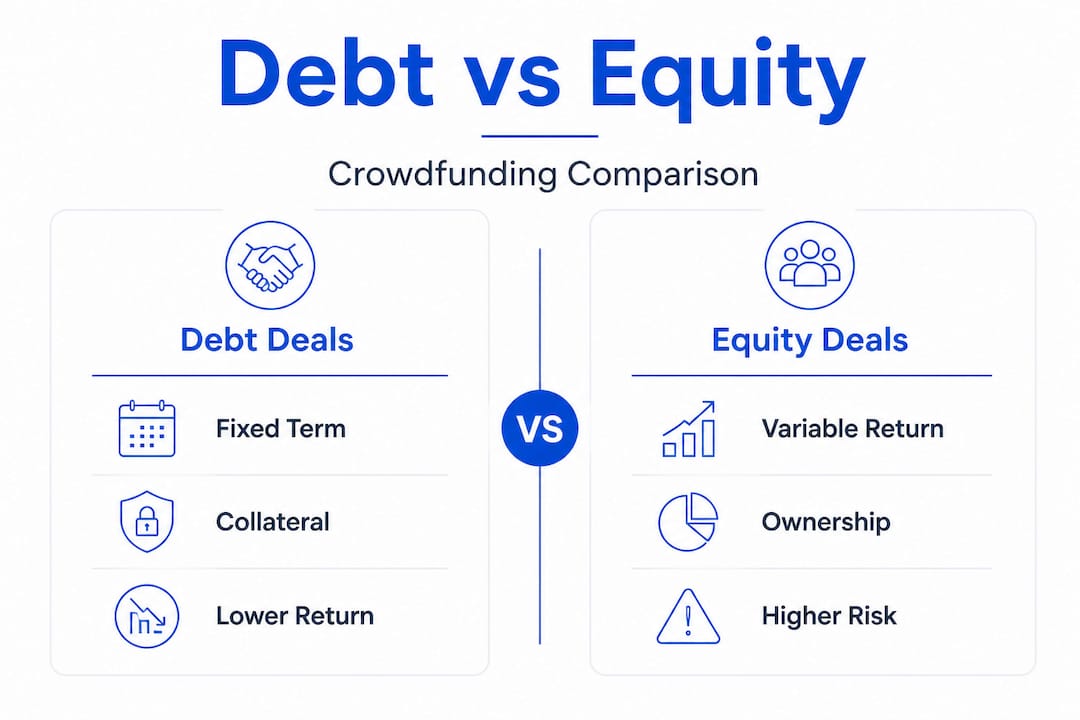

2. Identify the deal structure: debt vs equity

This is possibly the single most important distinction in real estate crowdfunding. Debt deals mean you are lending money and expecting repayment with interest. Equity deals mean you own a share of the asset and your return depends on its performance. These are fundamentally different risk profiles.

3. Review project duration and exit strategy

How long is your capital locked in? What triggers repayment? Projects without clear exit strategies or defined repayment events are a significant concern. Monitoring real estate trends helps you assess whether the proposed exit timeline is realistic given current market conditions.

4. Assess collateral and security

Is the loan secured against the property? What is the loan-to-value (LTV) ratio? A lower LTV (typically below 70%) indicates stronger collateral protection. Check whether the collateral is first-charge or subordinated, as this determines your priority if the developer defaults.

5. Evaluate the risk assessment

Look for independent risk scores, and check whether the platform performs its own credit assessments or simply lists all applicants. Platforms that are selective in their vetting typically show better historical performance.

6. Run a scenario analysis

What happens if the project is delayed by 12 months? What if the property sells for 15% below projected value? Running these scenarios prevents you from being blindsided. This kind of step-by-step analysis is precisely what separates informed investors from those chasing yield alone.

Debt vs equity: A quick comparison

| Factor | Debt crowdfunding | Equity crowdfunding |

|---|---|---|

| Security | Often secured by collateral | Typically unsecured |

| Return type | Fixed interest | Variable (profit share) |

| Liquidity | Defined repayment date | Tied to asset sale |

| Risk level | Generally lower | Generally higher |

| Upside potential | Capped at interest rate | Uncapped if asset appreciates |

| Typical yield range | 6 to 12% per annum | 8 to 20%+ per annum |

Debt investments often offer more security than equity, particularly when backed by first-charge collateral. This does not mean equity is always wrong, but the risk premium needs to genuinely justify the additional exposure.

💡 Prefer debt over equity for capital security, especially when you are newer to the asset class or operating in markets with weaker regulatory oversight.

Pro Tip: Always confirm whether collateral is a first-charge mortgage over the property or simply a subordinated loan. A subordinated lender is repaid last in the event of default, which is far less protective than many investors realise. You can also explore diversifying through fractional ownership as a complementary strategy for spreading exposure across multiple deal types.

Warning signs to watch for during evaluation:

-

🚩 Returns consistently above 15% with minimal risk disclosure

-

🚩 No independent audit of valuations or financials

-

🚩 Vague or non-existent exit timelines

-

🚩 Developer with no publicly verifiable track record

-

🚩 Collateral described in ambiguous terms without clear LTV ratios

Common mistakes and red flags to avoid

Even a robust analytical approach can be undermined by common missteps or overlooked warning signs. Recognising these patterns in advance significantly sharpens your investment discipline.

The most frequent mistakes investors make:

-

Failing to verify platform credentials before committing funds

-

Ignoring the significant regulatory differences between countries (France, Germany, and Poland operate under meaningfully different frameworks even within the EU)

-

Trusting polished marketing materials over raw performance data and independent audits

-

Underestimating liquidity challenges in alternative investments and overcommitting capital to illiquid projects

-

Diversifying across multiple projects on the same platform, which creates concentration risk at the platform level, not just project level

Red flags that demand immediate scrutiny:

-

🚩 Persistent payout delays with vague explanations

-

🚩 Absence of any tangible collateral or security structure

-

🚩 Platforms that are not ECSP-authorised or registered with a national regulator

-

🚩 Projects where the developer refuses to provide independent valuations

-

🚩 Extremely high projected returns without detailed risk disclosure documentation

Delays of 20 to 50% are common across Europe, with France recording approximately 30% of projects experiencing delays in 2024 alone. Platform failures frequently occur because operators prioritise growth and fundraising volume over careful project vetting. This dynamic surfaces as a critical structural risk for investors who do not look beyond the headline yield.

⚠️ Illiquidity and overvaluation are the two risks that tend to catch investors off guard most frequently. Neither is obvious from a platform’s homepage.

Learning to identify red flags early is an active skill that sharpens with each project you evaluate. Building a habit of patient, disciplined analysis is far more valuable than reacting to exciting opportunities under time pressure.

Pro Tip: Avoid investment FOMO (fear of missing out). Real estate crowdfunding projects do not disappear overnight. If a platform pressures you with countdown timers or scarce-slot messaging, treat that as a yellow flag, not an incentive. Quality deals do not need manufactured urgency.

How to verify and monitor your investments

Once you have invested, analysis does not stop. Effective verification and active monitoring keep your portfolio healthy and give you the information needed to act if circumstances change.

Your ongoing monitoring checklist:

-

📋 Review platform update reports at least monthly

-

📋 Track project milestones against the original timeline

-

📋 Monitor regulatory news in the project’s country

-

📋 Check for changes in platform ownership or management

-

📋 Re-examine collateral values if property markets shift significantly

-

📋 Engage with investor communities and discussion forums for early signals

Ongoing monitoring is crucial given the high rates of delay and platform failures across European real estate crowdfunding markets. A passive approach after investing is one of the fastest ways to be caught off guard by deteriorating situations.

Sample monitoring log for active projects

| Project name | Platform | Investment date | Expected completion | Last update date | Status | Action needed |

|---|---|---|---|---|---|---|

| Project Alpha | Platform A | Jan 2025 | Dec 2025 | Mar 2026 | 3-month delay | Contact platform |

| Project Beta | Platform B | Mar 2025 | Sep 2026 | Apr 2026 | On track | None |

| Project Gamma | Platform C | Jun 2025 | Jun 2026 | Feb 2026 | No updates | Escalate inquiry |

This kind of structured log gives you a clear picture of your entire portfolio at a glance. When a project misses a milestone or stops providing regular updates, that is an early signal worth acting on quickly.

If red flags surface post-investment, take these steps:

-

Contact the platform’s investor relations team in writing and request a formal update

-

Check if other investors on community forums or review aggregators are experiencing similar issues

-

Review your contractual rights, particularly around default procedures and collateral enforcement

-

Consider ongoing investment monitoring resources to benchmark your situation against broader market norms

-

Adjust future allocations to reduce exposure to the platform or country involved

Adopting institutional monitoring strategies at a retail investor level is entirely achievable with disciplined record-keeping and regular review cycles.

Our perspective: What most guides miss about real estate crowdfunding analysis

Most analytical guides in this space focus heavily on entry criteria: how to pick a project, what yields to target, which platforms look credible. That is genuinely useful, but it misses a critical dimension. The ongoing risks linked to regulatory maturity and cross-country governance gaps are consistently underestimated, particularly for investors active in markets like Germany and France.

Here is a hard-won lesson: analysis does not end when you click “invest.” The platforms that fail investors most severely are rarely the ones that appeared problematic at entry. They are the ones that looked perfectly reasonable but lacked the operational discipline to manage projects through market downturns or developer difficulties. Platform failures are often due to incentivising growth over careful project vetting, and that pattern is still very much alive across the European market in 2026.

The contrarian view worth holding is this: chasing high-yield equity deals without robust collateral is not ambitious investing, it is speculative behaviour dressed up in property market language. The investors who consistently perform well are those who prioritise capital protection, accept slightly lower yields in exchange for genuine security, and treat every new platform with healthy scepticism until it earns trust through demonstrated performance.

Technology genuinely helps here. AI-assisted tools for liquidity and payout risks analysis, aggregated platform reviews, and peer-sourced data are reshaping how retail investors access quality information. Leveraging these resources is no longer optional for anyone serious about this asset class. A patient, data-driven approach combined with peer intelligence is what separates consistently successful investors from those reacting to market noise. 🌱

Find the right platform for reliable real estate crowdfunding analysis

Ready to put your new skills into action? The quality of your analysis depends enormously on the quality of your data sources, and having everything in one place makes a measurable difference.

Start analysing with Crowdinform and access aggregated reviews of over 500 European crowdfunding platforms, AI-powered project evaluations, and a built-in copilot to help you explore live opportunities. Crowdinform works like a TripAdvisor for crowdfunding: you get transparent, community-driven ratings alongside intelligent data tools to compare deals, assess collateral structures, and monitor your active investments. Whether you are evaluating your first project or refining an established portfolio, having a single, trusted intelligence hub makes every step of the process sharper and faster. 🎂

Frequently asked questions

What risks are most common in European real estate crowdfunding?

The main risks are project delays, illiquidity, overvaluation, and regulatory gaps differing by country, with significant variation across France, Germany, and newer EU markets.

How can I check if a crowdfunding platform is properly regulated?

Verify that the platform holds a licence under the European Crowdfunding Service Providers regulation and confirm its listing in the ESMA registry or the relevant national regulator’s register.

Why might debt investments be considered safer than equity in real estate crowdfunding?

Debt investments typically carry defined repayment schedules and collateral protection, whereas equity returns are variable and depend entirely on the asset’s eventual sale, making debt generally more secure for capital-focused investors.

What is the average expected delay rate in France for real estate crowdfunding projects?

Around 30% of projects were delayed in France as of 2024, making it one of the European markets with the highest incidence of project timeline overruns.

Do I need to monitor real estate crowdfunding projects after investing?

Yes, continuous monitoring is essential because payout delays, platform management changes, and property market shifts can all affect your returns after your capital is committed.

Recommended

- Step-by-step real estate investing in Europe: a clear guide - Article | Crowdinform Investment Guides Real estate crowdfunding

- Crowdinform - Make money by investing in loans(P2P), real estate and startups with crowdfunding!

- Top advantages of startup investing for European investors - Article | Crowdinform Investment Guides Startups

- Fractional ownership: How investors diversify with ease - Article | Crowdinform Investment Guides fractional investment

- How market analysis shapes property investment success