Key Takeaways

Low entry barriers: Platforms like Indemo let you invest from only €10, making property accessible to all.

Diversification reduces risk: Spreading investments across countries and platforms helps protect your money from defaults and delays.

Returns and timelines: Average returns range from 7 to 12 percent, but you should expect to wait up to two years for cash-out.

Platform choice matters: Choosing regulated, debt-focused platforms can improve safety and reliability for both novices and intermediates.

What you need to get started in real estate crowdfunding

Once you understand the opportunity, the first step is making sure you’re actually ready to act. The good news is that the barriers are genuinely low compared to buying property directly.

Documents and funds

You will need three things before you can invest on any regulated European platform:

-

A valid government-issued ID (passport or national identity card). All platforms operating under the European Crowdfunding Service Provider (ECSP) regulation are required to verify your identity through a Know Your Customer (KYC) process.

-

A bank account in your name, ideally in euros. Most platforms accept accounts from any EU member state, and several also accept investors from Norway, Switzerland, and the UK.

-

A starting capital of at least €50 to €100, depending on the platform. This is genuinely the minimum, not a recommended amount.

Beyond documents and money, you need a basic understanding of what you are buying. In real estate crowdfunding, you are either lending money to a developer (debt-based investing) or buying a small equity stake in a property project (equity-based investing). Each carries different risk and return profiles, which we cover in detail later.

Choosing the right platform as a beginner or intermediate investor

Not all platforms are equal. Some specialise in Baltic markets, others focus on Western Europe or the Iberian Peninsula. Some are built for cautious investors who want steady monthly repayments; others cater to those chasing higher equity returns over longer timeframes. Checking top platforms, minimums, and features before committing is time well spent.

Find the best real estate crowdfunding platfrom here!

Pro Tip: Start with a debt-based platform like Profitus if you are new. Monthly repayments give you early feedback on how the process works, and the collateral backing reduces your downside risk considerably.

The right mindset

Patience is not optional here. Real estate crowdfunding is not a trading account where you can buy and sell in seconds. Your capital will be committed for months or years, and some projects will run late. Understanding diversification in property crowdlending from day one will save you a great deal of frustration later. Think of your portfolio as a collection of small, independent bets on European property markets, not a single high-stakes wager.

Step-by-step process for your first investment

With requirements prepared, you are ready to follow the concrete steps necessary to make your first investment. The process is more straightforward than most beginners expect.

Step 1: Sign up and complete KYC

Visit your chosen platform’s website and create an account using your email address. You will then be prompted to complete the KYC process, which typically involves uploading a photo of your ID and a selfie or a short video. Most platforms complete verification within 24 to 48 hours. Some, like EstateGuru, use automated systems that verify in minutes.

Step 2: Deposit funds

Once verified, navigate to the deposit section and transfer funds from your bank account. Most platforms accept SEPA bank transfers, which are free within the eurozone. Some also accept credit or debit card deposits for smaller amounts. Always start with an amount you are genuinely comfortable leaving untouched for 12 to 24 months.

Step 3: Browse and select projects

This is where the real research begins. Every listed project should show you:

-

The loan-to-value (LTV) ratio — the loan amount as a percentage of the property’s appraised value. Lower is safer.

-

The location and property type — residential, commercial, development, or rental.

-

The borrower’s track record — how many previous projects they have completed on the platform.

-

The expected return and term — annual interest rate and projected repayment timeline.

-

The risk rating — most platforms assign an A to D or similar grade based on borrower and project quality.

Read the project documentation carefully. A well-structured project will include a professional valuation report, planning permission details, and a clear exit strategy (sale or refinancing).

Step 4: Make your first investment

Once you have selected a project, enter your investment amount and confirm. Your funds move from your wallet to the project. You will receive a loan agreement or investment contract, which you should save for your records. Many platforms, including EstateGuru with its €50 minimum and auto-invest feature, allow you to set up automated investing rules so that repaid capital is reinvested automatically into new projects matching your criteria.

Step 5: Monitor your dashboard

Log in regularly (weekly is sufficient) to check repayment status, project updates, and any communications from the borrower or platform. Most platforms send email notifications for repayments and delays. Do not panic at the first sign of a delay; late payments are common and do not automatically mean a loss.

Pro Tip: Use platform diversification across at least two or three platforms from the start. If one platform experiences technical issues or regulatory changes, your entire portfolio is not affected.

Common mistakes and risk management

Completing an investment is straightforward, but avoiding critical errors and understanding risks are just as vital. Many beginners lose money not because the market failed them, but because they made avoidable mistakes.

The four main risks

-

Defaults: Borrowers fail to repay. Default rates run at 3–6% across the sector, with platforms recovering 60–80% of capital through collateral sales. This means you rarely lose everything, but you may wait months for recovery.

-

Delays: Projects run over schedule. Construction timelines slip, planning permissions take longer, or property sales stall. This is the most common issue you will encounter.

-

Platform bankruptcy: The platform itself could fail. This is rare but has happened. Your investments are typically held in a separate legal structure, but the recovery process can be slow and stressful.

-

Illiquidity: Unlike stocks, you cannot sell your investment on a whim. Secondary markets exist on some platforms but are thin and may not find buyers quickly.

Mitigation strategies

“Diversification is not just a strategy in real estate crowdfunding — it is the strategy. Spreading capital across countries, platforms, and project types is the single most effective way to protect your returns.”

Here is how to apply this in practice:

-

Keep LTV below 80% on every project you select. Projects with LTV above 80% offer less collateral protection if the borrower defaults.

-

Spread across at least 10 to 15 projects before concentrating on any single one. This smooths out the impact of individual delays or defaults.

-

Invest across at least two countries to reduce exposure to a single property market’s cycles.

-

Stick to ECSP-regulated platforms. The European Crowdfunding Service Provider regulation requires platforms to maintain investor protections, segregate funds, and publish standardised key investment information sheets (KIIS).

-

Avoid concentrating more than 20% of your portfolio in any single project, no matter how attractive it looks.

Pro Tip: For intermediate investors, reducing risk with diversification across debt and equity projects can improve your risk-adjusted return. Debt projects stabilise your income; equity projects boost your upside.

Debt-based investments are generally safer for intermediates building their first serious portfolio. They offer predictable repayments, collateral backing, and shorter terms. Equity investments can deliver higher returns but require patience and a higher tolerance for uncertainty.

What to expect: Returns, timelines, and exit strategies

Now that you know the risks, it is important to understand what realistic outcomes look like and how you will get your money back.

Average returns across leading platforms

The numbers are genuinely competitive compared to savings accounts or government bonds. EstateGuru delivers 10–12% annually, Indemo targets 20% or more through capital appreciation, and Raizers typically offers 8–12% on development loans in France, Spain, and Germany. These figures are gross returns before tax, so factor in your local tax obligations.

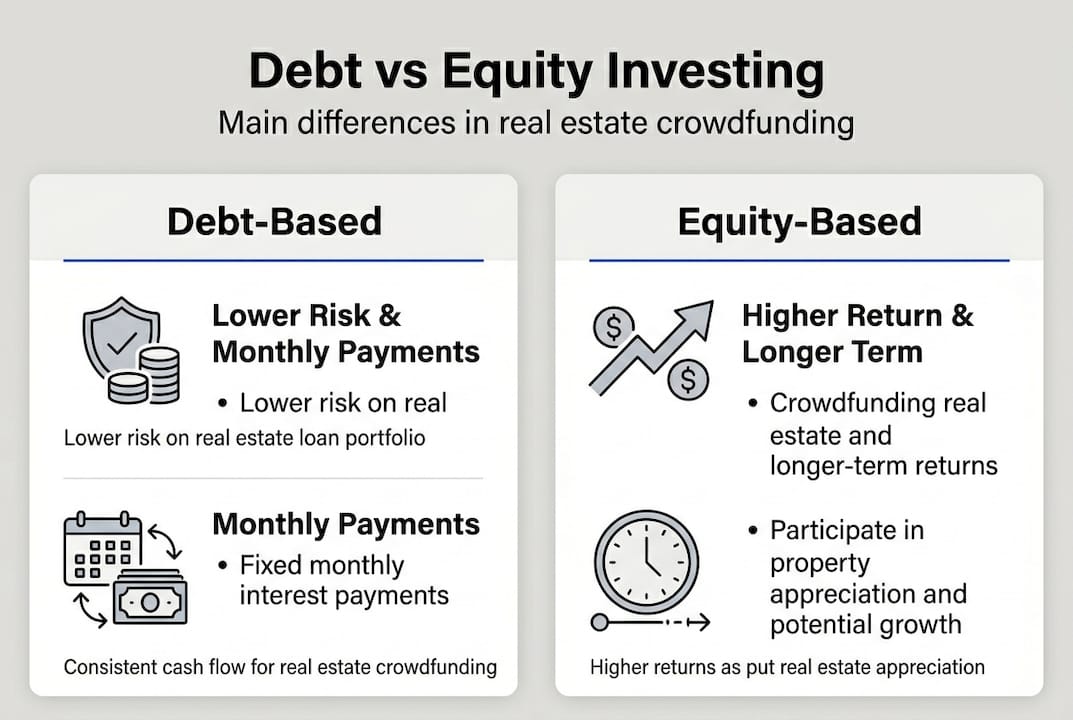

📊 Debt-based vs equity-based: a comparison

Feature: Typical return - Debt-based: 8–12% p.a., Equity-based: 10–20%+ p.a.

Feature: Risk level - Debt-based: Lower, Equity-based: Higher

Feature: Repayment frequency - Debt-based: Monthly or quarterly, Equity-based: On exit (sale/refinancing)

Feature: Typical term - Debt-based: 12–36 months, Equity-based: 18–48 months

Feature: Collateral - Debt-based: Yes (first or second charge), Equity-based: No (ownership stake)

Feature: Liquidity - Debt-based: Low, Equity-based: Very low

Feature: Best for - Debt-based: Beginners, income seekers; Equity-based: Intermediate, growth seekers

Timelines and liquidity

Most debt-based projects run for 12 to 36 months. Equity projects can extend to 48 or even 60 months. Plan your cash flow accordingly. Do not invest money you might need urgently. A practical approach is to stagger your investments so that some are maturing every few months, giving you a rolling stream of returned capital to reinvest or withdraw.

Delays are normal. A project with a 12-month term may run to 15 or 18 months. This is not necessarily a warning sign; it is simply the reality of construction and property sales. What matters is whether the platform communicates clearly and whether the collateral remains intact.

What happens at the end of a loan

When a loan matures successfully, your principal and final interest payment land in your platform wallet. You can withdraw to your bank account (usually within 1 to 3 business days) or reinvest immediately. If you have set up auto-invest, the platform will redeploy your capital automatically. If a project defaults, the platform initiates collateral recovery, which can take 6 to 18 months but typically returns 60–80% of your invested capital.

Why the best real estate investing strategy isn’t what most beginners think

With the technical steps and risks covered, let us step back for a seasoned perspective on what actually drives success in this space.

Most beginners arrive on a crowdfunding platform and immediately sort projects by highest advertised return. It feels logical. If you are here to make money, why not pick the option paying the most? The problem is that the highest-yielding projects are almost always the highest-risk ones. They carry higher LTV ratios, less experienced borrowers, or locations with thinner property markets. Chasing that 15% headline rate often means waiting longer, experiencing more delays, and in some cases absorbing partial losses.

The platforms and investors that have genuinely thrived over time are those that prioritised regulated environments and disciplined diversification over headline numbers. Zero capital losses have been recorded on Urbanitae, a regulated Spanish platform, demonstrating that careful project selection and strong collateral structures can protect capital even through difficult market conditions.

The uncomfortable truth is that a 9% return across a well-diversified, regulated portfolio will outperform a 14% return on a concentrated, high-risk selection in almost every realistic scenario. The former compounds steadily; the latter gets disrupted by a single bad project that locks up your capital for 18 months while you wait for recovery proceedings.

Patience and research genuinely pay off more than luck or timing. Spend time understanding diversification best practices before you commit significant capital. Read the KIIS documents. Check the platform’s track record on defaults and recoveries. Ask yourself whether the platform is ECSP-regulated and how long it has been operating. These factors matter far more than any individual project’s advertised yield.

The investors who build real wealth through property crowdfunding are not the ones who found the hottest deal. They are the ones who built a systematic, diversified portfolio across multiple platforms and markets, reinvested consistently, and stayed calm when individual projects ran late. 🌱

Start your step-by-step real estate investing journey today

You now have a clear, actionable framework for investing in European real estate through crowdfunding platforms. The knowledge is in place. The next step is putting it to work.

Crowdinform is Europe’s leading aggregator for crowdfunding platforms, bringing together reviews and data from over 500 platforms across the continent. Think of it as the TripAdvisor of European property crowdfunding. You can compare platforms side by side, read verified investor reviews, and use the built-in AI copilot to analyse specific projects and receive personalised recommendations. Whether you are selecting your first platform or building a multi-platform portfolio, Crowdinform gives you the intelligence to invest with confidence. Start exploring today and turn this guide into real results. 🎂

Frequently asked questions

What are the minimum investments for European real estate crowdfunding?

Typical minimums start at €100, making entry genuinely accessible for beginners with limited starting capital.

How safe is real estate crowdfunding compared to direct property?

Crowdlending offers diversification and passive income but carries risks such as defaults and delays. ECSP-regulated platforms add meaningful investor protections, including segregated funds and standardised disclosures.

How long is my money locked up in a typical investment?

Expect terms between 12 and 24 months for most debt-based projects. Illiquidity over 12–24 months is standard, though liquidity is generally higher than with direct property ownership.

What happens if a project defaults?

Default rates sit at 3–6%, with platforms typically recovering 60–80% of capital through collateral sales, though timing varies and recovery can take over a year.